Dear @bhaskarjain

Thank you for the kind reply. Right. As you do most of the time you have hit the nail on the head.

I too found it funny when they had these young guys up on the podium and it was a strange sight ![]() . They were a small if I remember right a below 1000 crore fund till about 12 months ago with less than 20000 portfolio’s. Suddenly they got additional 800 crores but 60000 new portfolios so basically a lot of small investors. I could see the change all the while. I think that they have been trying something to see how they should present themselves as a company, or something to do marketing of their company, but they are making some presentation bloopers. It is for me not taking away from their investing style, they are trying a marketing style, so that is fine. Let them try some marketing. But most of it is silly to say the least. Their AGM’s were and are good enough. They should cut out the rest of this stuff they have gotten into.

. They were a small if I remember right a below 1000 crore fund till about 12 months ago with less than 20000 portfolio’s. Suddenly they got additional 800 crores but 60000 new portfolios so basically a lot of small investors. I could see the change all the while. I think that they have been trying something to see how they should present themselves as a company, or something to do marketing of their company, but they are making some presentation bloopers. It is for me not taking away from their investing style, they are trying a marketing style, so that is fine. Let them try some marketing. But most of it is silly to say the least. Their AGM’s were and are good enough. They should cut out the rest of this stuff they have gotten into.

For that matter even Quantum has started sending out funny emails trying to market themselves and they do not reflect what I think of them. So I wonder why suddenly these both want to get into marketing themselves, what they have stayed away from all these years.

Right again, and quite frankly this is something else I had discussed over email with one of our VP members. There is a huge keyman risk and I am basically watching the positions they take and their strategy. For me their are two keyman risks, one is the fund manager leaving and the second is the fund manager dramatically changing his strategy. If either was to happen I would exit the fund. Also, point to note, another keyman is the gentleman who handles the debt and from what I could understand also the currency side.

On Noida toll bridge I think they learnt a valuable lesson. Trust me I really don’t understand why they have Mahindra Holidays. I really don’t see the logic and don’t like the company in the portfolio, but I had to make peace with it if I like the other 24. I do hope they relook their logic on Mahindra Holidays.

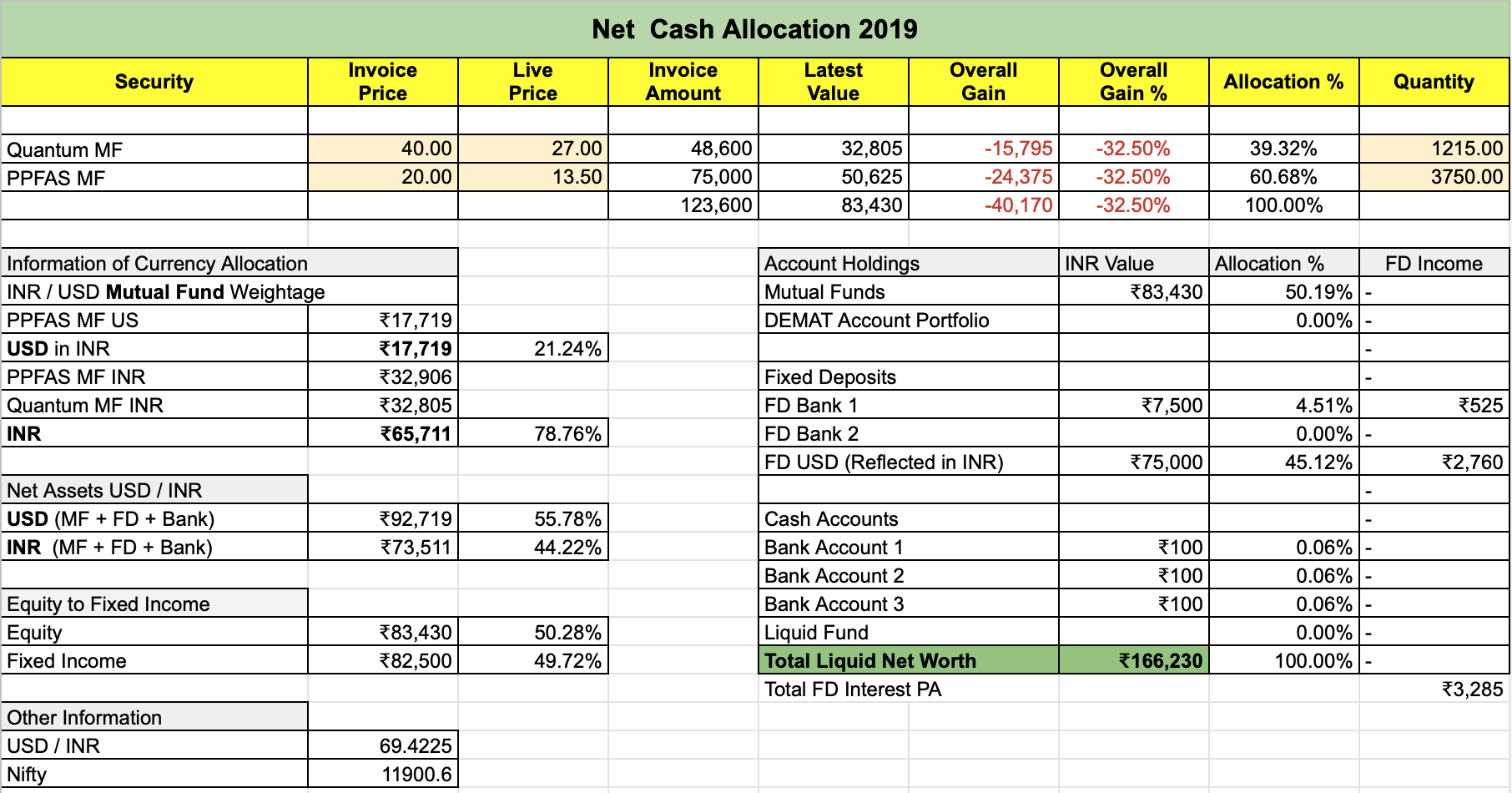

For that matter, my other MF Quantum bought Yes Bank ![]() at the wrong time. I know they will have their own biases and in a MF if 1-2 stocks are not suiting my thinking, or they end up making a bad decision, I will have to live with it.

at the wrong time. I know they will have their own biases and in a MF if 1-2 stocks are not suiting my thinking, or they end up making a bad decision, I will have to live with it.

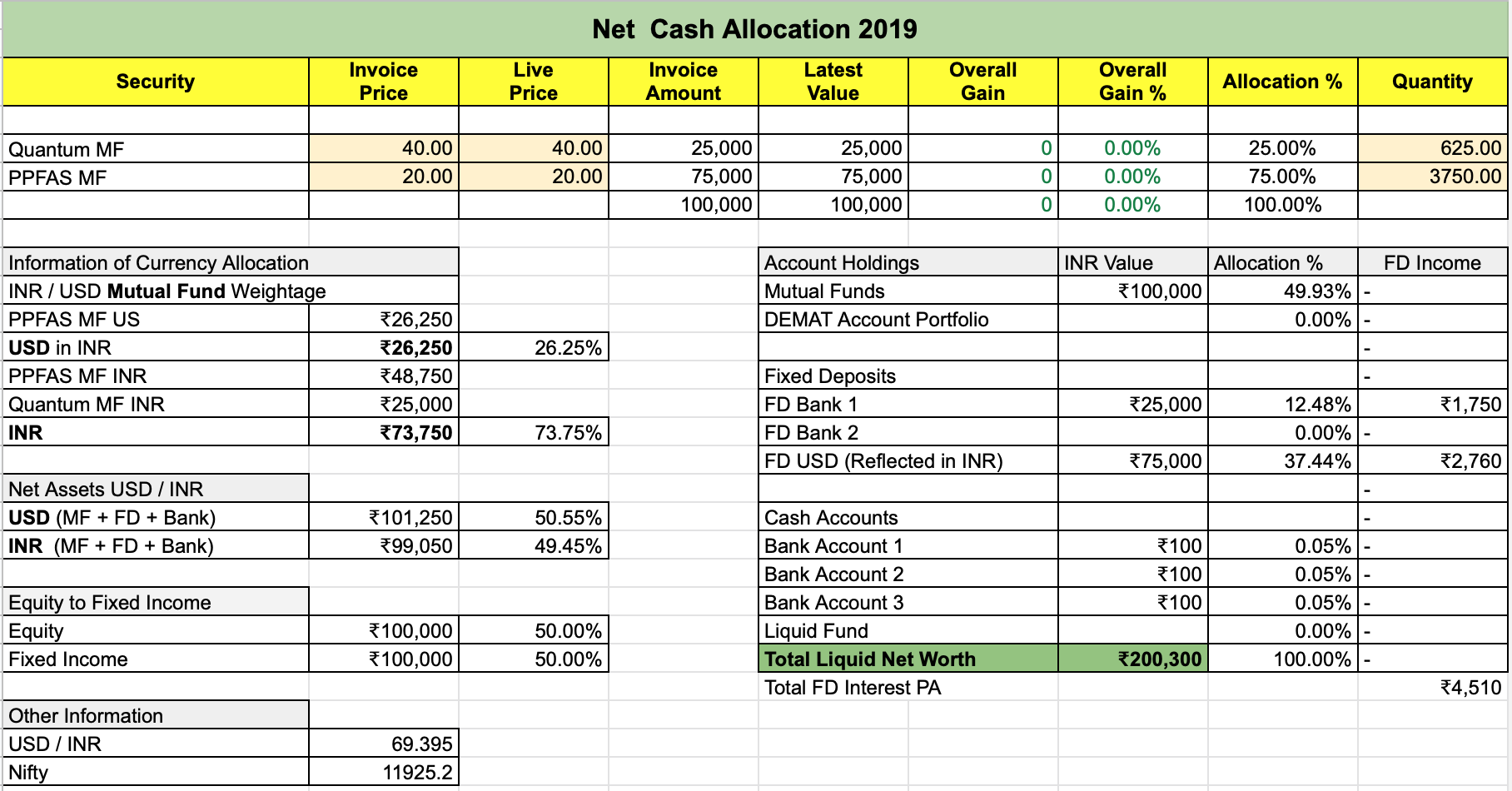

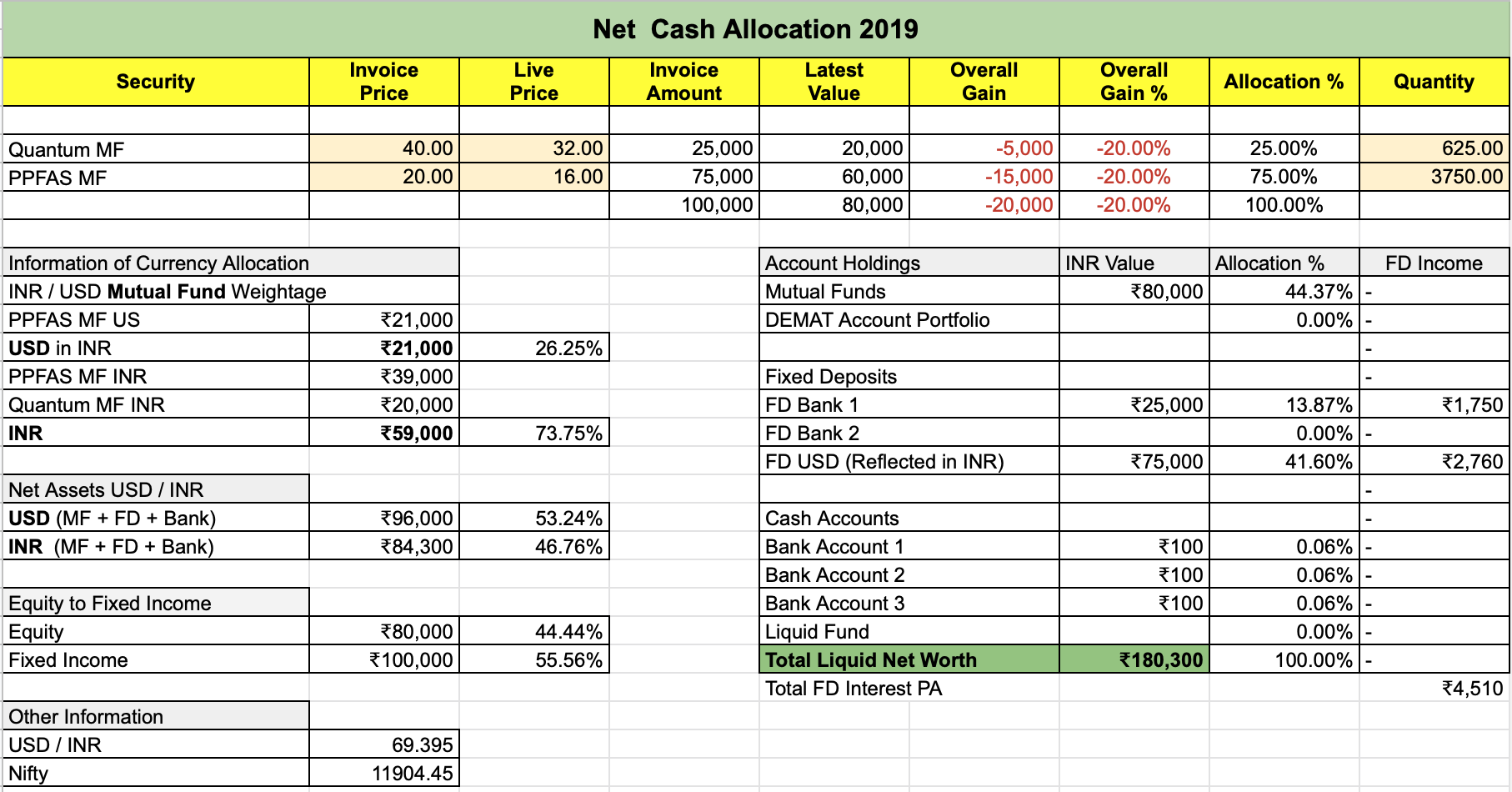

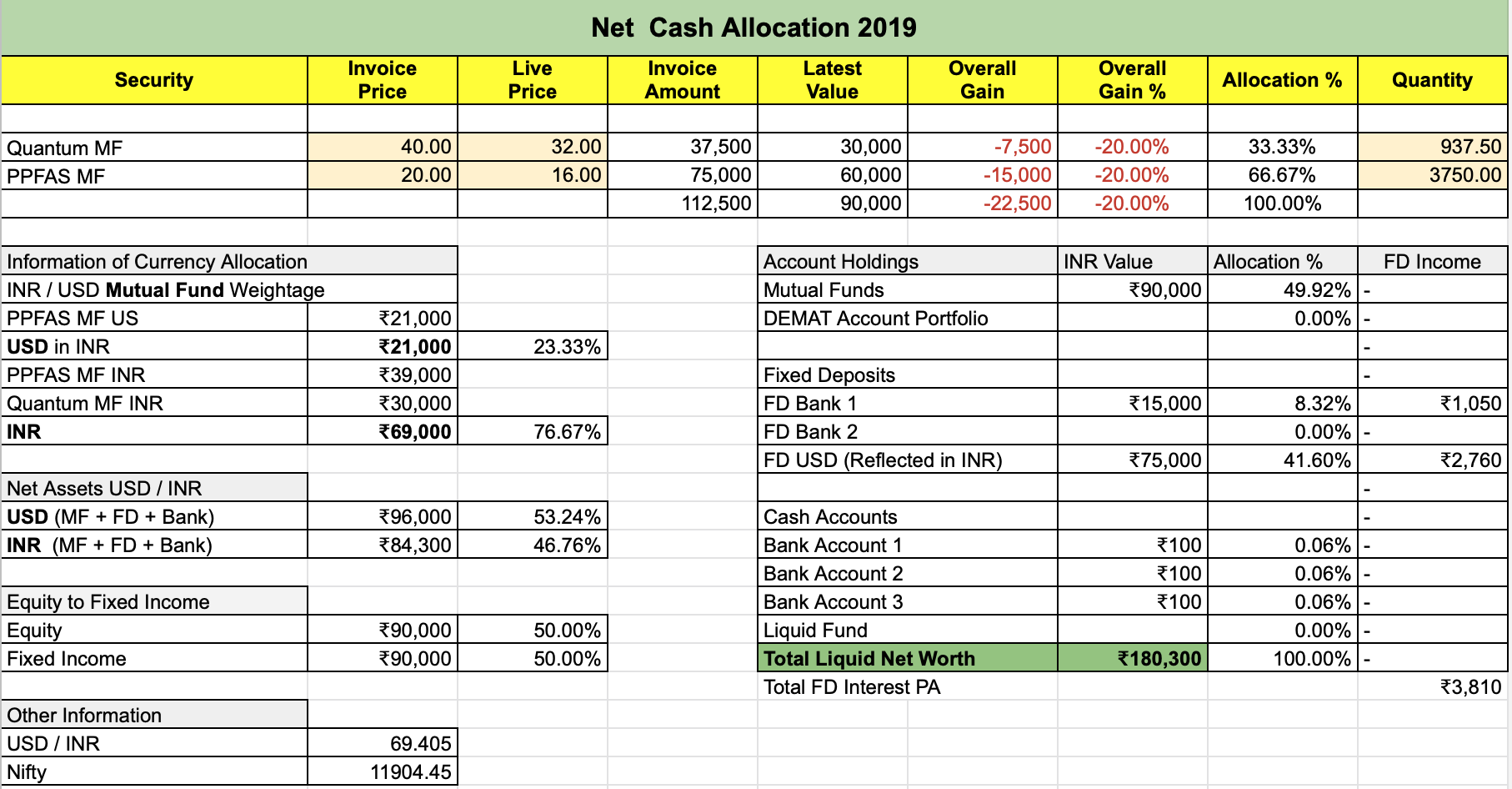

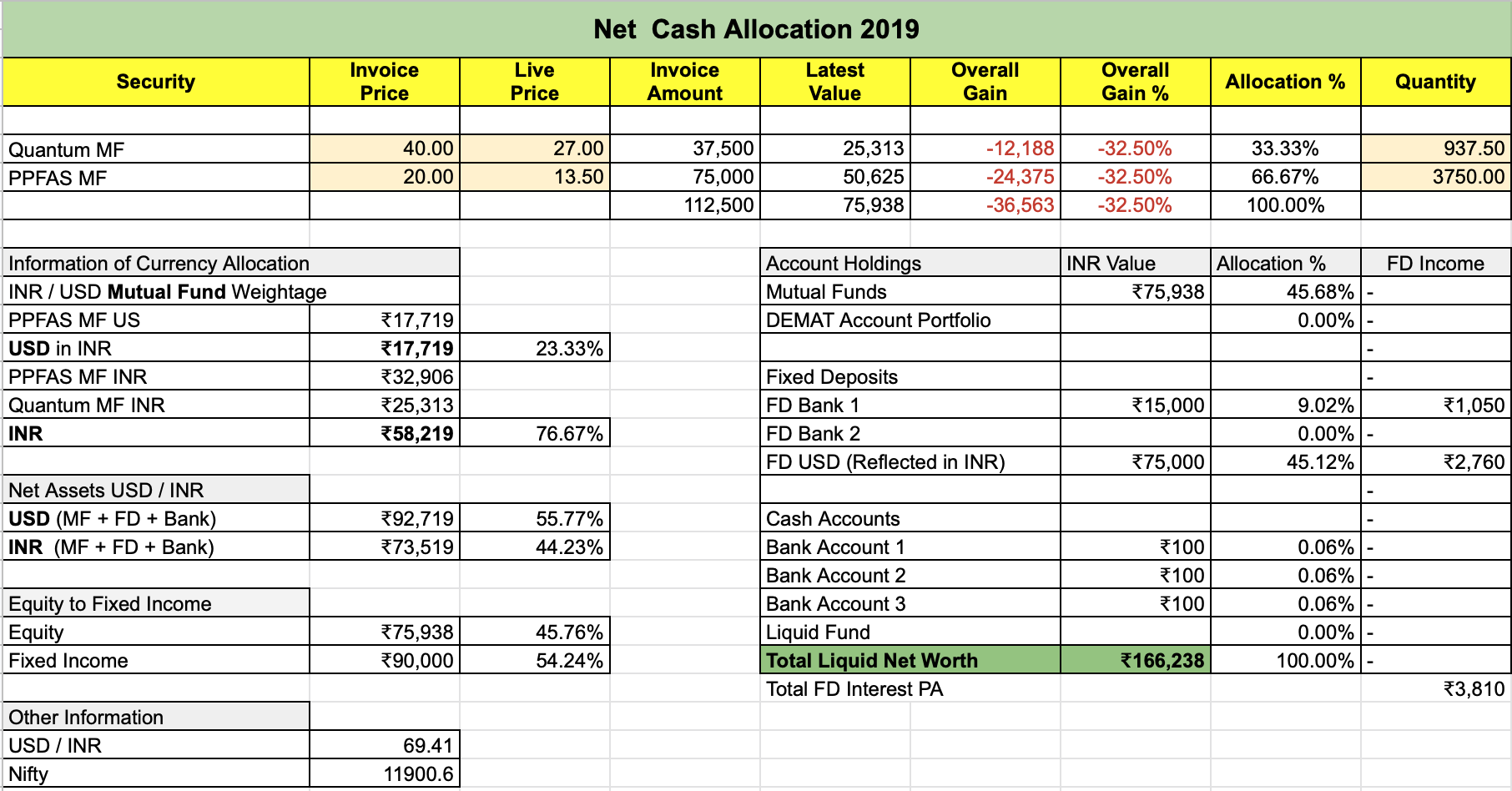

We have just seen so many famed funds taking a hit with DHFL and ILFS. Both Quantum and PPFAS were not into any of these. Their learning and experience buildup plus skin in the game shows here. They have no incentive to play with other people’s money because it is their money also. I like to think that is a better way to bet for me.

PS: PPFAS also bought Google much earlier and recently Charlie Munger said that they made an error or commission and they should have bought Google a long time ago and you are correct, they bought Amazon before Berkshire.

So the gist of what I could see was, having burnt their fingers a bit with some bad decisions and having taken some good decisions they are in a reasonably sweet spot of a couple of decades of experience and with a couple of more decades to play out. I will watch like a hawk.

Dear @yudiagg

You could check it here https://www.valueresearchonline.com/funds/newsnapshot.asp?schemecode=19701

Dear @777

I am a novice and unable to predict the end of good days of an entire economy which is a world superpower ![]() .

.

Dear @gautham1

I am not sure but I think they started buying Lupin around 800 odd maybe I am wrong. I must admit I am not trying to double guess the manager but I agree the logic they gave out on the PE of Nestle USA was not making sense. Nestle USA is a low growth high dividend stock and not so comparable to Nestle India. They may have their logic on valuation, but that logic made no sense since growth of Nestle USA is so different. If they had a pure valuation logic and not an apple to apple comparison, it would have made more sense to me.

On their performance, sure it is quite similar to most others, but like I said, there is a currency risk also being taken out to a reasonable degree so I am happy with that.

Long and short, there are going to be risks in the stock market. We just choose what we can live with and what makes sense.

Dear @sarthakkumar19_

Like I have said before; I am not looking at returns. I am looking at risk. Whatever the returns I am ok, I am fine and I am content. I am more focused on saving consistently to grow my corpus than being dependent on the stock market. I am not looking for a fund that beats benchmarks, if that is what is the focus of my fund manager I would be scared because they would take higher risks and doing short term punts with higher churn to try and beat the market. I do not want to think about returns. I want funds that think about risk mitigation and risk management. Currently both Quantum and PPFAS fit the bill.

Great questions all. Thank you for them.

I was just repeating what I have been reading that US has outperformed the entire world in the past 10 years, and that may not be same in the next 10 years. I am sure, US is superpower now and will remain after 10 years as well.

I was just repeating what I have been reading that US has outperformed the entire world in the past 10 years, and that may not be same in the next 10 years. I am sure, US is superpower now and will remain after 10 years as well.