CLSE informed the exchange about the credit rating it has received from Crisil. (You can read the intimation letter from here) Crisil has reaffirmed its rating.

You can also read the rating rationale published as on 17-Oct-2016 using the below links.

Some Key points from the rating rationale are:

(Comments against each point in brackets are my views)

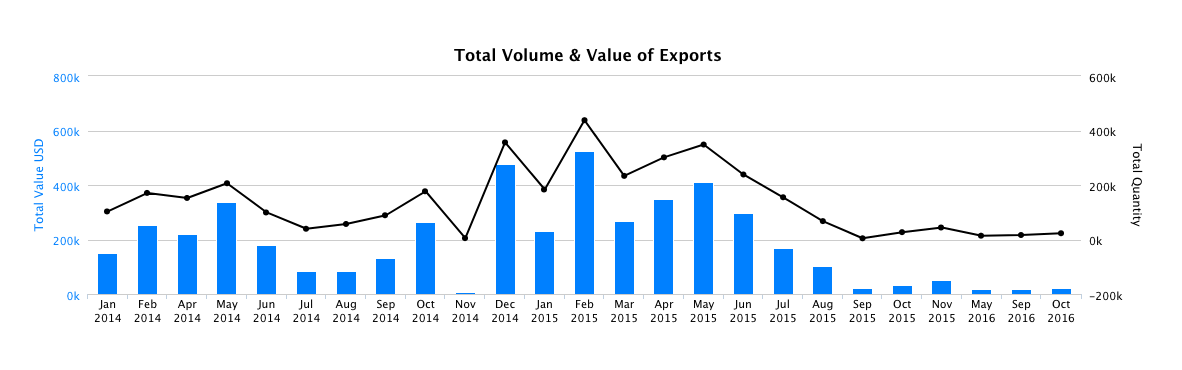

Significant volumetric growth of about 33% in sales in fiscal 2016 over the previous fiscal, despite a challenging market scenario in the basmati rice processing industry, indicating CLSE’s strong market position. (As mentioned previously, co. has shown growth in volume but had low exports in value terms due to lower realization.)

Robust liquidity, marked by prudent working capital management, and absence of repayment obligations and capital expenditure plans.

Low bank limit utilization at an average of 30% in the 12 months through July 2016.

Low gearing and strong interest coverage ratio.

Low brand penetration. (CLSE needs to continue its focus on Maharani’s Brand building and as pointed out by @ARTR CLSE can get better results with such efforts.)

Geographically diversified revenue profile. (A diversified client base is always welcomed by investors as it helps spread the risk.)

I don’t have any information regarding any future capex.

However, CRISIL’s rating rationale does mention about- "absence of repayment obligations and capital expenditure plans."

Additionally, CLSE focuses more on rice trading rather than manufacturing.

Ekansh mital of katalyst wealth has suggested chamanlal sethia as his pick of 2017 in recent interview given to outlook magazine. Also the price activity from rs.60 to rs.100 in past two months suggest something cooking beneath .

Discl: invested

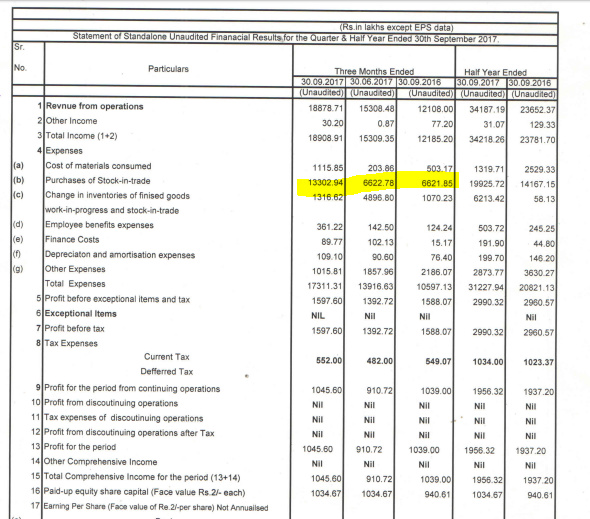

The company has shown stellar performance over the last fiscal. Going through the financials of FY16 as well as 9M FY17 it is evident that the company had been facing tremendous pressure over lower realizations. Infact according to an ICRA Industry Report, the Basmati export realizations have declined from Rs. 77,988/MT to Rs. 56,149/MT, which is around a 25% drop. Yet the company has managed to keep the revenue more or less stable. In FY16 the revenues declined by 5% but considering the 25% drop in realizations the performance was stellar, as the promoters must’ve added a good number of customers to maintain the revenue levels. Also, even in such difficult times the promoters have managed to keep the OPM and NPM stable, infact the company recorded an almost 100% growth in NPM(FY16) which is a testament to their ability to cut costs without hampering the overall operations of the company. This only goes to show the quality and resourcefulness of the core team who are at work in Chaman Lal Setia Exports.

Rice prices right now are at an all time low, however it appears that the cycled has bottomed out and a revival is around the corner. With rice production declining and production picking up one can expect a price rise, which in turn should lead to higher realizations. Iran, which used to be one of the major importers of Indian Basmati rice has also indicated that the import ban which was levied 2 years ago in 2015, might be lifted soon. The stock is well poised to be a multibagger.

Good Topline growth reported by CLSE inspite of the challenges thrown by demonetisation and GST and when most of the other competitors are reported muted growth. Although bottom line is still in pressure.

Actually, they get more than 80 percent revenue from export, so, GST n demonetization does not have much impact on them. Since last 1.5 years , basmati rice price was in downward cycle due to demand supply scenario until March. As per export data, Q1 18 export of basmati rice did a YoY growth of 33 percent vs q1 17 primarily driven by price increase . This was reflected in 30 percent plus growth in KRBL and now in chamanlal numbers . However, the latest shock has been european ban which will ve approx 8 percent impact on exports . Now, specific to chamanlal , though 40 percent revenue growth looks great, two questions :

Could there be any potential risk or downside of inventory numbers or will we have good bottom line growth in coming quarters

2.any idea what is chamanlal exposure to EU.KRBL has disclosed they have negligible exposure to EU.

Disc : invested in chamanlal

@suru27@Deepen_Thakkar

Can anyone clarify the following for me

In the annual report 2016 , on page 31,it is given that all 6 independent directors are not paid any remuneration.same thing is written in 2015 annual report.How do directors not get paid? sent them a mail,but no reply.

8% worth 1700 cr of total 22000 cr is exported to EU from India. Chaman Lal may have same kind of exposure. We will come to know in last quarter of FY 18 depending upon impact on realisations

Can anyone clarify the following for me

In the annual report 2016 , on page 31,it is given that all 6 independent directors are not paid any remuneration.same thing is written in 2015 annual report.How do directors not get paid? sent them a mail,but no reply.