This is my first new post and I wish I had done this a couple of weeks ago since the stock price has almost doubled since then. That said, I still think it has enough left on the table for a new entrant.

CLSE is a old basmati rice player with a modern rice mill and focussed exclusively on basmati rice. They have consistently grown their topline and bottomline over the last 4 years (Sales - 185cr to 510 cr from FY 2010 to FY 2015. PAT - 7 cr to 20 Cr over the same period). Q1 FY 2016 was a bumper quarter with a PAT of 10.8 Cr and margins jumping to 7.8% (as compared to 3.9% for the whole of FY 2014-15 and 2.2% in Q1 of FY 2015) which is the reason why the markets got so excited.

CLSE has some good differentiated products i.e. basmatic rice for diabtic people, pesticide free basmati rice and I believe they will do well going forward. For the first time, they have started on a branding and marketing exercise in India and that should augur well for them.

More importantly, I think 2015-16 will be one of the toughest years for the basmati rice industry as most are carrying overpriced inventory due to the steep fall in paddy prices this season. So this year should truly separate the wheat from the chaff in the basmati rice industry (REI reported huge losses in Q1) !!! and CLSE having done so well in Q1 is a good sign.

I estimate that the rest of the year will follow the Q1 pattern and we should end up with an eps of 35+ for the current year.

Positives

Good, dedicated management

Technically sound and one of their promoters is considered an expert in basmati rice.

consistent historical growth and focused on the bottomline and margins.

Negatives

Not sure if the current year profits is on account of an one-off export order won.

They certainly don’t have the pricing power or the brand strengths of KRBL. They have started off on the journey now though.

the steep run leaves tremendous risks for a new entrant

management not very communicative – not even a basic ppt on the website.

Disclosure - Hold a good position in CLSE and have been holding this for about 4 months now.

Thanks for starting this thread… I have been observing this stock from the last 1 month and it made me curious by hitting upper circuits since the last 10 days. However, I still do not understand why it has been so cheap(PE of just 5) from so many years. I have tried to know more about their products but to no avail as no presentation is available anywhere.

But going purely by the numbers, it does seen cheap even after this heady run up. I want to know whether it is prudent to invest in such illiquid stocks as it is more prone to speculators actions.

Have been following CLSE and LT foods from same sector from a while now. Big valuation gap when one compare KRBL with LT foods and CLSE. CLSE is the smallest listed player in this segment.

While LT foods is second largest after KRBL. LT foods possess strong brand names like Daawat. Brand endorsers like Amitabh Bacchan and Sanjeev Kapoor

They are into other value added products too like organic foods and snacks items.

A lot of information available on LT foods on public domain.

have been tracking this for almost 6qtrs now but could not add position as very limited info on it was avaiable…didnt got what capacity they have to proceas basmati, couldnot find their brand Maharani in any modern trade, very small in size compared to krbl, lt food and other known players…thought such small company with unknown capacity wont get even half of what krbl was trading tht time…so was checkin qttly numbers and had see its rise from 40 to 80 than 120 b4 this qtr results…and spree of UCs followed after Q1

will be helpful if we get info on capacities and future growth plans if any to quantify on upside growth to its topline

was thinking to start the thread but was tied up with current qtr earnings…and then the runup after q1 made me think its too late…thanks @saeyons for starting the thread

Hi

One observation is that

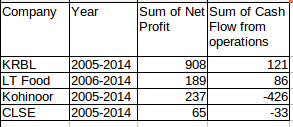

Cumulative PAT for past 10 years is 64.62 crs

Cumulative CFO for past 10 years is -33.32 crs.

Which means company is unable to convert the profits into cash.

data is from screener, FY 15 data is not available yet in screener.

I think KRBL and CLSE operate on slightly diff tracks.

KRBL largely buys paddy, processes, warehouses and then sells it. CLSE buys a combination of paddy + semi-processed basmati rice and then sells it. For example, most of what they bought this year was the latter type. KRBL also does the latter, but I think the qty is limited to less than 10% or so. But for this reason, KRBL’s profits are far more predictable than CLSE’s.

I don’t know the capacity they have, but what they told me is that they are operating at less than 50% capacity. Probably bcos when they buy the semi-processed basmati rice, they don’t need as much processing capacity, but perhaps just warehousing space.

What I would really like to find out is how really differentiated their products are - rice for diabetes and pesticide free rice. If their claims are true, then they should be able to increase or atleast sustain their margins.

The other reason why we don’t know about their products is that till last year, almost all of their produce was exported. It is only in the last few months that they have started selling in India. They told me that within the next one year, they would be selling pan-India but they kicked-off this process in and around the Delhi area. Anybody in Delhi area can confirm this?

Seasonal business could show negative cash flow for the following reason

Highly seasonal businesses will have negative cash flow from operations during the low season. Working capital items such as inventory and debtors will chew up cash flow during this seasonal build up.

Negative cash flow may be because they have to buy paddy at time of harvest for the full year.

All the companies in the rice business including KRBL, LT Food, Kohinoor will have similar or even worst numbers.

Godrej’s Nature Basket has started selling Maharani Parboiled Basmati Rice for Diabetics in Pune. I have tried it and not only it tastes very nice, it really doesn’t shoot the blood sugar up.

The diabetic market is huge in India and up till now it usually depended on (Organic) Brown Rice. But the truth is - brown rice needs to be soaked overnight to make it somewhat soft, takes a lot of time to cook and even then it is quite rough to eat. Bottom line - it is not as delicious and convenient as polished rice. I know many diabetics and pre-diabetics who have stopped eating brown rice for above reasons.

Maharani Parboiled Basmati Rice appears to be a winner in taste, softness and sugar control.The pricing too is little cheaper than Organic Brown Rice. My hunch is it is going to be very popular in India - even among non-diabetic health conscious people.

Cos not able to generate profits into cash for long are generally not good investments (exceptions are always there). Hence if all cos in this industry are having same issues, better to view complete industry with this fact in mind while investing. There are many industries which don’t earn even cost of capital due to bad economics eg: Airlines. We need to check if this industry is in similar situation.

There are some companies which look very interesting on P/L basis but just dig a little deep first question there was no meaningful cash flow generated by the company

Second if you browse the EXIM details in the shipping bill of this company you will find the exports are made on third party basis which means actually as an export house you are allowed to purchase shipping bill and the actual exporters endorse your name in the shipping bill so that you can claim star trading status this is why yoy the revenue shows increase and opm is increasing whereas virtually there is no cash flow

Third watch the raw material purchase detail and tarded purchase detail under the expense you will understand the clear picture

I cannot comment on the valuvation but this company cannot be compared with LT FOODS forget even think to compare with KRBL

Sum of Cash flow and net profit for rich processors

Now we can make deductions from the data.

@indirachitra I could not understand what you are trying to say? Do you mean to say that company is not exporting any rice but is some how managing the bills to get star trading status?

Mr Gaurav I never meant they are not exporting if you see the shipping bill

the actual manufacturer name will be different but the export will be done

in CLSE name that is called third party exports. Secondly the cash flow

comparison made by you looks at one angle of cash generation that is good

but in KRBL and LT foods please see the corresponding increase in the gross

block from 2005 2014 and also look at the other assets secondly the claim

about diabetic rice was retraced many times and nothing is clearly

mentioned in the annual report.

Mr Gaurav I am just trying to excise caution in this particular case hope a

little more digging will reveal the real problem in this case

Regards

1…Chamanlal’s Maharani Rice Export Data :-Showing Increasing Trend YoY

2…Chamanlal Increase its production (Not Capacity) by 35 v% in fy 15

3.Only Concern with CLSE is decrease in Realisation ie…per unit export price showing declining trend but it is compensated with increase in volume

4this is part of commodity business

(Dis:- Holding at much lower level)

Very True…

But tht’s the reason behind such healthy BS of CLSE

1…CLSE is doing Asset Light Business

2…ie…Procuring Rice from domestic market without setting up Rice mills and selling in International market at premium

3…CLSE clearly states they will spend on Marketing now own-words to improve brand Value of Maharani Rice …Agree it can not be Compare with KRBL or LT foods

4…CLSE operating cashflow Fy 15 is 20 cr against -21 cr

5…Only play in CLSE is Low Valuation, Increase in Export,Opening in Iran Market,& Healthy BS

6…Dont expect returns like KRBL its altogether in different League

(Invested at much Lower Level)

I appreciate the logical way though which you saw the traded goods being significant and checked the shipping bill details. The indicator for the same gimmick are the small font,without coma used for the line item " purchase of stock in trade" as compared to the cost of material consumed and the ratio of inventory to receivables. For this company it is close to 1.5 for LT Foods it is about 4.3 and for KRBL it is around 6. The other interpretation could be it could be trading, but since the shipping bill says a different story, even if it is to a small degree, it shown deceiving traits.

The current season paddy prices are even lower than last year with basmati paddy quoting at around 1600/quintal. This is generally bad news for the sector as they carry inventory and most companies do not have much pricing power.

CLSE doesn’t carry much inventory, has just forayed into branding and has very low debt at this point. So this situation does create a good opportunity for them to stock up on low cost inventory for their branded products.

They are doing well this year and will probably make an eps of Rs40+ for 2015-16 and closer to Rs.50 for the next year. All in all, exciting times to be a shareholder on this counter.