An outstanding Q2 given the conditions. CLSE’s focus on speciality products has resulted in a significant expansion of margins. This year 2015-16, they will end up with an eps of around Rs.45.

I think next year will witness an increase in their topline as well. I think volumes have already started picking up, but given the lower basmati prices, this really doesn’t reflect in their topline. Additionally, they are setting a target of Rs.100 crore in the Indian markets alone and plan to reach there next year.

I own a good position and intend owning for the next several years if they can sustain their growth momentum.

2015-16 will be a great year for the company with eps crossing Rs.45 (as compared to Rs.20 for FY15). and that too without too much debt.

They have recently started selling in the Indian markets and hope to cross 125 Cr (around 20% of total sales) in the next year or two. Internationally their marketing is taking them to newer geographies.

The price is stuck at 313 for the last 2 weeks on BSE due to circuit filters. The company has taken steps and they feel that clse should move out of t-to-t by december end. They also plan on having listed on NSE before the next fiscal year starts. My guess is that we should see 500 (adjusted for split that will be announced tomorrow) by mar 2016.

But the company has been in talks with nse to get listed and with bse as well to move out of the T group. Only time will tell if these efforts bear fruit. But if doesn’t, then you are right.

In some sense, I also think this is a good opportunity to accumulate at depressed prices. At an eps of 8, the stock is available at single digit p/e’s and given the consolidation in the sector, we might well see krbl attracting fmcg type valuations in the next 2-3 years. That would automatically pull clse along with it to say a 15 p/e multiple.

With a moderate 15% CAGR growth (which is much lower than their last 10 year average) over the next 2-3 years and an expansion of p/e’s, we could see a 100-200% return in stock prices.

I think they will cross 600 Cr sales with a PAT of 60+ … which translates to an eps of 12. Given their differentiated products, their margins have been close to that of KRBL … but then, I do expect KRBL to pull ahead this year bcos of the low paddy purchase price the last season which should come into the market these days.

But still, trading at just 5-6 p/e and growing at good rates, clse deserves a rerating. Once their NSE listing tes finalized, I think we should witness a triple digit price for clse.

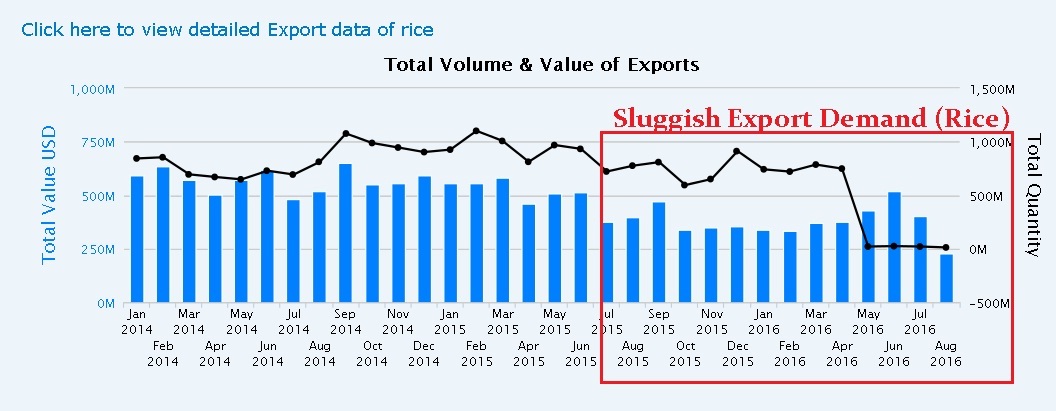

With Q4 sales down by 10% YoY and FY 16 sales down by 5% YoY from 508 cr to 485 cr. What is your view of members. Is it only due to falling prices of basmati rice in Q4. If that is the only reason I am ok. Apart form sales all other parameters looks great on balance sheet.

Net Profit increased by 91% YoY

Tax Rate 34% flat YoY

EBIT increased by 69.5% YoY

OPM% improved to 12.3% in FY16 from 7% in FY 15

NPM% improved to 7.6% in FY16 from 3.8% in FY 15

Short term borrowing down by 77% from 33cr to 7.4 cr

Inventory days 36 in FY16 compared to 50 in FY15

Receivable days 24 in FY16 compared to 34 in FY15

Cash increased to 50 cr from 12 cr

All this marks to all round improvement in operating efficiency and balance sheet. Views invited.

Also, the acreage for the current season is likely to be down by 30%… so prices of the paddy that comes out in december would be substantially higher than last year.

CLSE should do upwards of 600 cr this year. Also, about 75 cr of which would be domestic sales alone. If prices move up, they might do even much better than 600 cr. Let’s see.

But I think it’s a good buy and the muted q4 results have provided shares with reasonable liquidity and attractive price for new entrants. Ofcourse, prices cannot move beyond 78 till Oct 01 due to BSE restrictions… so, the timing is upto individual buyers. But liquidity would probably evaporate after Q1 results.

The June Qtr. results and a Twitter thread (screenshot below) drew my attention towards this company.

The good discussion on the forum so far tells that CLSE is more of a rice trader rather than a manufacturer, and their intent is to serve the market (primarily exports and is slowly moving towards domestic) with premium quality basmati under its Maharani Brand.

In order to get more insights, I did a deep dive into the company’s Annual reports and collated some quantitative data. Hopefully it will help resolve few of the concerns raised by fellow members.

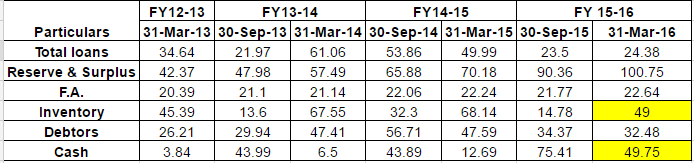

The view of Co.'s half yearly balance sheet is pleasing to see. Debt has been reduced by the firm and reserves have touched the 100 crore mark. Also, the inventory and cash data as per the half yearly balance sheet shows the company is able to convert inventory into cash (would like to highlight the 2016 inventory and cash numbers). In a way it is good as company usually has more cash in September which is the low season.

@vinamrachaware brilliant piece of information. Such quality data/charts are really helpful for the VP community to confirm the story behind this stock idea. Please help share the latest such data (as posted by you earlier, till 2015) or share the link for the benefit of all.

Lastly, It came as a pleasant surprise to me, the news of a Proposal to issue Bonus Shares(See link below).

Hi @vinamrachaware,

thanks for the Zauba data, even I agree that they aren’t selling under the maharani brand. Is it possible to find their unbranded exports through Zauba? Because the numbers seem to suggest that the profits have broadly held up (albeit minor declines). Additionally, I have heard from a credit analyst at Crisil that this company works on tender / order basis in export market which essentially means they export only if they have orders and the ordering parties have good credit rating. So I am assuming that most of their business is B2B and that they don’t really rely too much on their brand for exports.

A bonus issue of 10:1 announced on 29th august , this is clear signal for nse listing where one of the mandatory provision is capital of 10crs . Nse listing can open doors for institutional investors so a pe rerating is on the cards .Also a new website unveiled , if in future management does show intent for branding and selling products in local markets via dmart or online portals , this can be a sector to be judged at par with fmcg but all this will take time ,but a sure rerating can happen in near term because of nse listing . My views can be biased as I am already invested and in mood to accumulate more

I went through the AR16, sharing my notes from the same:

1.Sale of 482.45 cr (PY 508.02 cr). Although there was a decline in value of sales but in quantitative terms there was an increase of 27% approx. This is because there was a fall in the average price realization in the case of the sales.

2. PBT of 57.12 cr has registered an increase of 93% (PY 29.54 cr) which is mainly due to timely procurement of raw materials at very reasonable rates and through product innovative ideas of the management.

3. The company has developed a novel process for reducing energy and water requirements in paddy parboiling process. As a result the water consumption and energy expenditure in mechanical parboiling of paddy is greatly reduced.

4.The Company has also developed the novel process of recycling of most of hot water used for soaking of paddy during parboiling of rice, thereby generating little waste water and still having a high quality product.

5. Managerial remuneration of WTDs- Mr. Ankit Setia & Mr. Sankesh Setia have increased by 192.56%

6. The Increase in remuneration is on the back of:

a. Mr. Ankit Setia’s tremendous performance in the Company. He is the main engine for exports marketing and developing new market, after his joining in the company the exports which were to the tune of 100 crores have gone up to 400 crores approx.

b. Mr. Sankesh Setia has participated in various international food exhibition & has developed new foreign markets and added 82 international customers.

7. Promoter holding has increased by 0.49% to 74.86% (PY 74.37%).

8. Reduction in Indebtedness to the tune of 25.61 cr

9. The Promotion of flagship brand Maharani is on the Top agenda of the company and plans to go for aggressive advertising in print and electronic media.

10. Company has explored new export market and the management continues to maintain its efforts for the same.

11. Actual productions (in Qtls): 310958 (PY 313252)

12. Directors have extended a loan of 17 cr @12%, an interest of 1.73 cr was paid to directors.

(All the above points are taken from the AR16 and can be found under different sections like MD&A, director’s report, notes etc)

Sharing my thoughts on few of the above points:

It is pleasing to see that firm has achieved a 27% volume growth, and will be interesting to see how well the company is able to sustain such growth. The efforts put in by the duo Ankit & Sankesh (WTDs) looks to be the driver for the same.

Another thing that caught my attention and requires further digging is the 93% rise in PBT (Which as per the co. is mainly due to timely procurement). Was this beneficial procurement a result of efficient managerial efforts or was there any bit of luck involved? in case the latter is true, this shouldn’t be a point of celebration…because what has gone in our favor this year might not do the same in next year. Also, what is the firm’s procurement process and how strong it is against such moves?

Few developments and achievements of the firm in process improvement are good news and exhibit management’s focus towards efficiency…reduction in debt level is another good point.

From the look of this AR16, management seems to be focused on achieving higher growth by tapping new exports and building the brand name “Maharani”.

The volume growth is possible because CLSE also buys semi-processed rice and the numbers I have mentioned in my AR notes above are only it’s in house production numbers. The lower exports you are seeing are in value terms (not quantitative), which is low due to lower realization this year.

Hope this answers your query.

I agree with Yogansh’s observations. Chaman Lal is in fact at an inflection point. With the focus on Maharani brand and marketing, CLSE can push for much higher growth in top and bottom line in coming years