Background

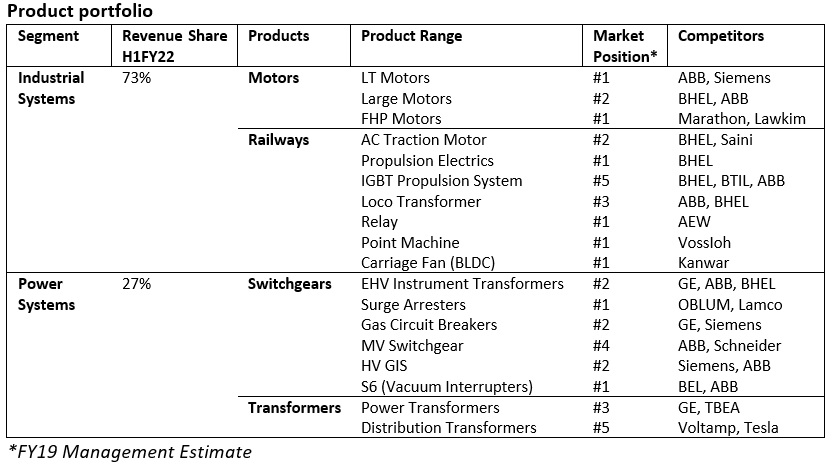

CG Power & Industrial Solutions Ltd (CG Power) is a leading capital goods & engineering company with a diverse portfolio of products across electric motors, railways, transformers, switchgears, drives & automation segments. The company’s products mainly find application in industrial, railway and power sectors.

The company was positioned among top 1-5 players in majority of its product segments. However, it was loosing market share due to lack of management focus, fraudulent activities by its erstwhile promoter’s (Avantha group) and subsequent fund crunch.

CG Power’s lenders-initiated steps under RBI’s Prudential Framework for Resolution of Stressed Assets, leading to Tube Investments of India Limited (TI), a listed company and part of the Murugappa Group acquiring a controlling stake (~53%) in November 2020. TI has infused about Rs.7 bn of equity, besides also subscribing to certain warrants.

Post takeover by TI, a new board has been constituted under the leadership of Mr S. Vellayan (Chairman) and Mr Natrajan Srinivasan (MD), settlement of old lenders has been done, recasting of previous years’ financials has been carried out and liquidation/divestment process of certain overseas subsidiaries has been initiated. Performance is back on track with PBT of Rs.215 crore achieved in H1FY22 as against management’s initial indicative target of about Rs.500 crore of PBT in next 4-5 years.

Business Overview

Historically, about 65-70% of revenue was contributed from domestic markets and rest was from international operations. However, majority of overseas subsidiaries have been liquidated or in the process of liquidation. Now with just 2 operating overseas subsidiaries; about 90% of revenue is from domestic operations.

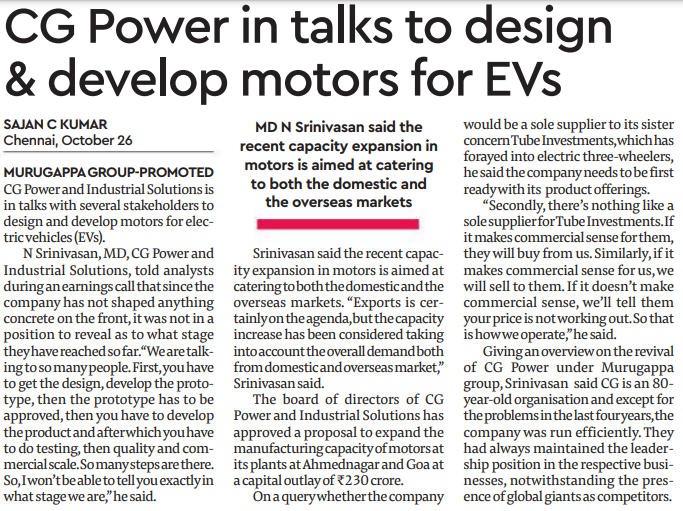

CG Power re-launched its Fast-Moving Electrical Goods (FMEG) range of products in 2019 such as domestic & agricultural Pumps, and industrial & domestic Exhaust Fans, but the contribution is insignificant. Now, the company has serious plan for the segment and preparing to extend FMEG product range, including ceiling fans.

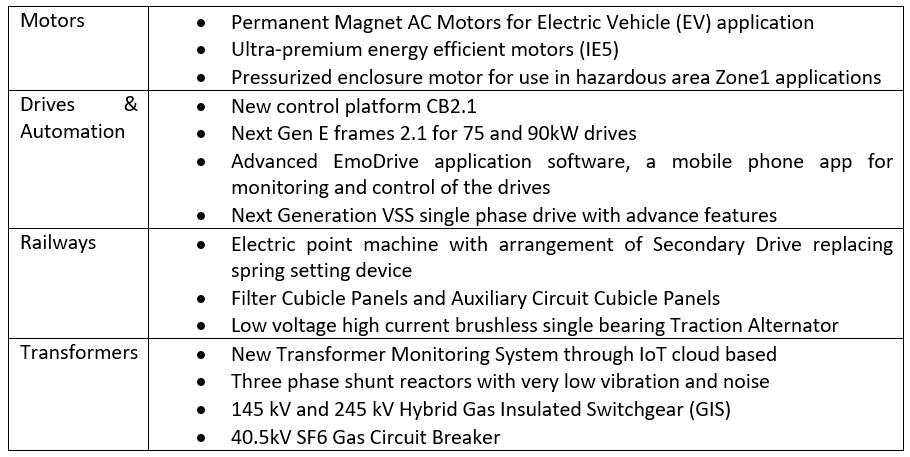

There is renewed focus on R&D and a number of new products have been developed, EV Motor being most significant one. Details of few such products are as following

Management

Tube Investments of India Limited (TI), a listed company and part of the Murugappa Group now holds ~53% stake in the company, besides certain warrants. Murugappa Group, Headquartered in Chennai, is an Indian conglomerate founded in 1900 and having presence in several segments including engineering, abrasives, auto components, bicycles, sugar, farm inputs, fertilizers, NBFC, Insurance and financial services. Mr. M A M Arunachalam is Chairman and Mr S Vellayan is MD of Tube Investments.

Mr S Vellayan is appointed as Chairman and Mr Natrajan Srinivasan as MD of CG Power.

Growth Triggers

• CG Power has eight decades of lineage with leadership position in many product categories. Strength of its product portfolio is evident from the fact that it was able to sell its products despite significant internal challenges and acute funding crunch during the last few years. Now, with a new promoter group and management team having clear focus on gaining lost ground, expanding product portfolio and range; business performance should improve significantly.

• Focus on R&D, industrial automation, EV motors, FMEG products, application & geographical expansion, improving capacity utilisation are management identified areas to drive revenue and profitability growth. Also, selling of identified non-core assets and FCF generation should help the company in becoming debt free in 2-3 years.

• Industry tailwind are conducive. After a subdued scenario during past many years; capital goods sector is seeing initial signs of recovery. Government impetus on manufacturing through PLI schemes, modernisation initiatives in railways & power sector, private capex driven by improving capacity utilisation and export opportunities, provide visibility for long-term uptrend in the sector.

• New management team has a proven track record. Mr Vellayan has been associated with Murugappa group since 2010 is credited for improved performance of Cholamandalam Investment and Finance as well as Tube Investments. Mr. Natarajan Srinivasan has also been associated with Murugappa group for last 15 years.

• For TI and CG Power’s future business strategy, the group is inspired by a very successful American company, Danaher Corporation; which has a successful track record of acquiring many entities and generating above average returns for shareholders. The management plans to replicate the same under TI as well as CG Power and use these companies as a platform for growth through acquisitions. Besides, there is stated intent of improving revenue growth & profitability, focus on cash flows, improving return on capital employed and pare debt.

• While the management was targeting Rs.5000 crore of turnover and Rs.500 crore of PBT in next 5 years, they seem to be much ahead on the target. During H1FY22, CG Power reported revenue of Rs.2504 crore and PBT (before exceptional items) of Rs.215 crore. With the legacy issues already fixed; enhanced product portfolio, operational efficiencies and industry tailwinds should help in achieving better earnings going forward.

Key Risks

• The Company had received notice of demand under Income Tax Act for Rs.606.30 crores for FY17. While the Hon’ble Bombay High Court has granted interim stay until admission of appeal before the High Court, it remains a major contingent liability.

• There are ongoing investigations by SFIO, ED and CBI pertaining to acts of erstwhile promoter & previous management and the company is also a party in this investigation. The Company believes that the Company or the present Board of Directors and Key Managerial Personnel appointed after the change of Management on 26 November, 2020, cannot be made liable for any violations in respect of certain past. However, risk of any unforeseen development remains.

• One lender has invoked the corporate guarantee amounting to Rs.41.56 crore due to bankruptcy proceedings initiated of Belgium Entities. The Company has not made provision towards this invocation on the assumption that the estimated recoverable value of assets of Belgium entities shall be sufficient to meet this liability.

• Successful expansion of product portfolio and favourable industry environment are key to expected superior growth prospects. Any disappointment on the same can have significant impact on the performance.

• Once CG Power becomes debt free, management has stated plans of driving growth through acquisitions. Acquisitions carry certain amount of risk pertaining to business as well as integration. Nevertheless, competent management with a track record provides comfort.

• Steep increase in commodity prices led by lag in pricing action has impacted the margins by about 2-3% during H1FY222. Large transformer orders have price variation clause, however smaller distribution products or industrial products do not have such clauses. Thus, the company is exposed to the risk of any sudden or steep increase in input prices.

• While probability for most of above-mentioned risks significantly impacting the business is low, however they cannot be completely ruled out.

Financials

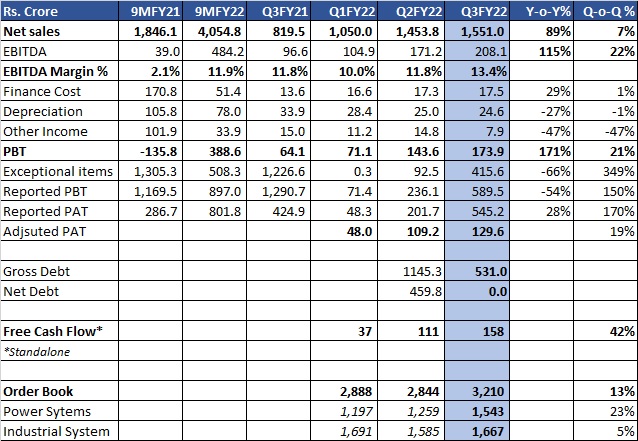

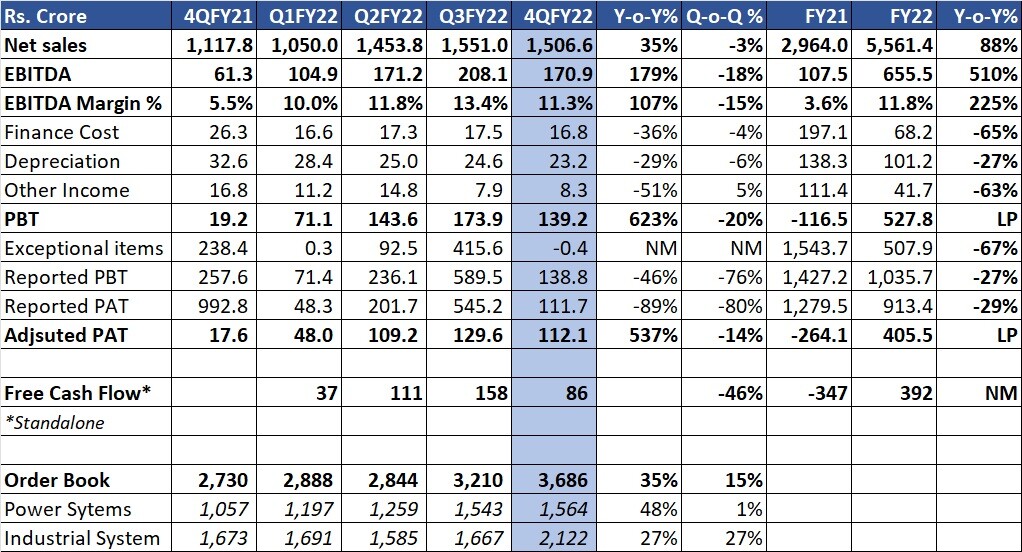

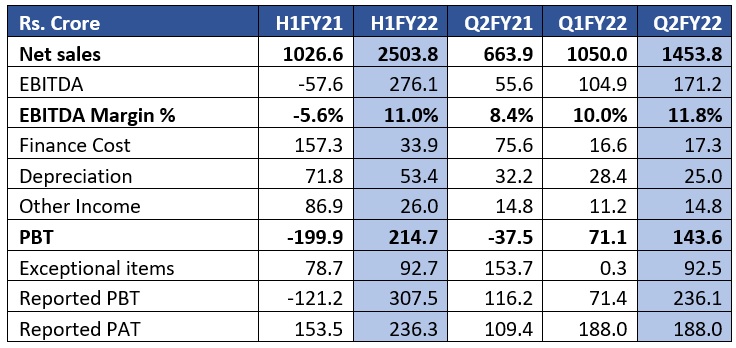

• I have not shown historical financials as the company was in a different trajectory during last few years. Also, YoY performance is not comparable due to severe fund crunch impacting operations during H1FY21.

• As visible above, CG Power has reported impressive performance during the first 2 quarters of FY22.

• Exceptional items majorly pertain to cessation of liabilities due to settlement/restructuring of past borrowings, provision for past corporate guarantees and other provision reversals etc.

• Apart from good P&L performance, cash flow generation was also strong with OCF of Rs.177 crore and FCF of Rs.140 crore in H1FY22. Debt level came down by about Rs.3 bn in H1FY22 and net debt stands at about Rs.7 bn now.

Valuation

Stock has multiplied from a low witnessed in the phase when the company had bankruptcy risk and post management change also; as no one had expected such fast and significant turnaround. At the CMP of Rs.178, market cap is Rs.240 bn and diluted market cap (on conversion of warrants) is around Rs.272 bn. At the annualised PBT of Rs.430 crore (H1FY22 x 2), stock is trading at about 63x. I have used PBT due to significant amount of one-offs and income tax is majorly deferred tax during H1FY22. One of the leading broking firms estimates PAT of more than Rs.7 bn in FY24, which gives forward PE of 39x.

Capital goods majors such as ABB, Honeywell, Siemens, Thermax are trading between 40-65x FY24 estimated earnings. While these multiples optically look high, there could be earning surprises as witnessed during previous capital goods up-cycle during 2003-2008 (led by high revenue growth and margin expansion).

While the turnaround as well as near term performance appear to be already discounted; compounding of earnings which can happen over a period under the capable new leadership is probably not discounted. An investor should look forward for only this now.

Philip Fisher writes “In evaluating a common stock, the management is 90%, the industry is 9% and all other factors are 1%”. Only time will tell if CG Power is a perfect 100% combo of this.

Disc: Invested. I am not SEBI registered Advisor/Analyst. The information provided above is for education purpose only.