This company came into my view when it fell from Rs.20 to Rs.13 or so in a very short timespan without any reason and stayed there for a good 4 months last year where strange things happened on daily price movement and volumes. It looked to be price manipulation to have a lot of volume of shares change hands at fixed prices.

I dug in more into the fundamentals of the company and found that they were getting into e-Waste disposal business and this post is solely about this new business and a possible new opportunity and what it could do to revenues and profits. This business has already started on 7th February, 2017 and we should have more clarity on how it adds to the revenues after this quarter results and management commentary.

For 1 MT of e-Waste costing around Rs.20k, it looks like around Rs.1.2 lakhs worth materials can be recovered by my back of the envelope calculations, going by the quantities per MT recoverable as mentioned in their results presentation last quarter. The company is aiming for a 92000 MT capacity of which 36000 MT is installed. The unknowns are of course the margins and capacity utilisation.

The company seems to have paid back the debt going by the interest costs on QoQ basis. This in itself should increase PAT considerably going forward but once the e-Waste revenues kick in, this stock could undergo a re-rating.

I will keep updating this thread with more information as I find them. Please do the same and let me know if you see any red flags in the company in terms of corporate governance, equity dilution, promoter holding and so on.

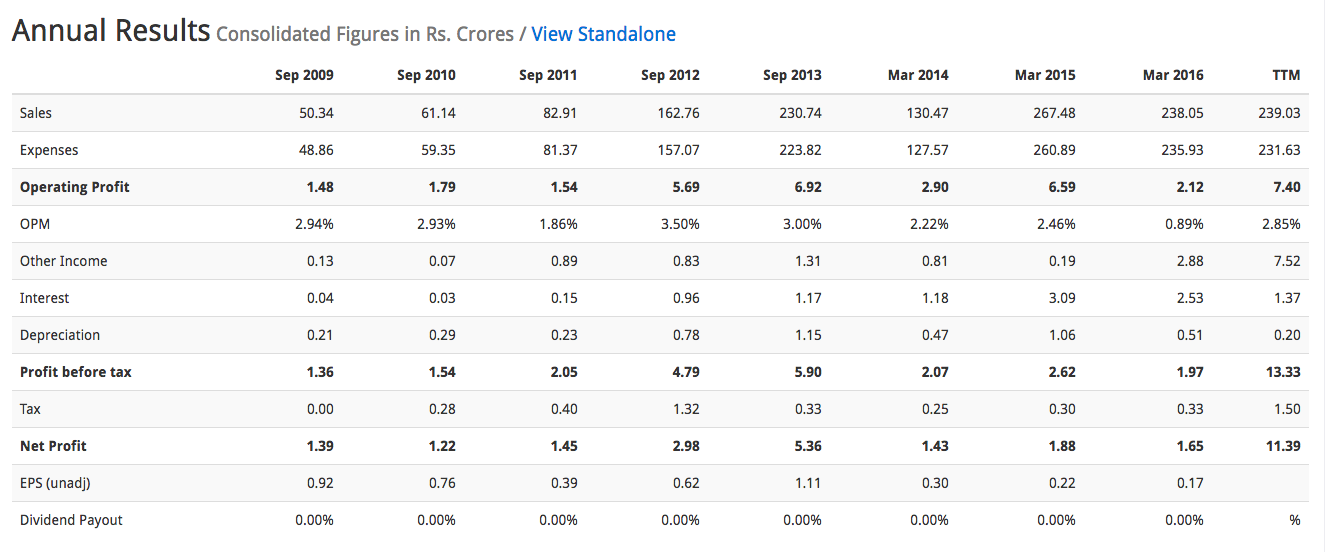

Though the company is reporting regular profits, it is not paying out tax

Company has a low return on equity of 1.71% for last 3 years.

Alsothere is a recent news http://www.equitybulls.com/admin/news2006/news_det.asp?id=204635 increasing authorized capital using11900000 Equity Shares on preferential basis to Strategic Investor Kuber Global Fund, a company incorporated in

the Republic of Mauritius and 5300000 Warrants convertible into Equity

Shares on preferential basis to Promoters at such price as may be

arrived at, as per the SEBI Regulations. Why to Mauritius firm? Any tax related issues??

Thanks for your inputs. I have checked screener for Cerebra and this is what I think.

Book value should get updated with the new plant value under Fixed Assets which I believe will happen in FY17 balance sheet.

The company has not been paying dividend because it has reinvested in building capacity.

Promoter holding should go up with the recently announced Warrants to about 7.5% (I think). It is still quite low, I agree.

Last couple of quarters the company is paying taxes if you notice.

Low RoE is again due to building capacity. The plant is now ready and should start generating revenues.

As for the equity dilution, the company claims that it will be used for building the e-Waste capacity. Currently the company has 10.8 Crores shares and the addition of 1.72 Crore shares will dilute the equity base by 16%. The price fixed for warrants is Rs.40 which seems to be alright although it concerns me that they are already talking of building more capacity when the currently built capacity is yet to generate revenues. It could be taken as a positive I suppose but as a conservative investor, it is a cause for concern.

TTM sales of Rs.239 Crores and PAT at Rs. 11.39 Crores. TTM should improve more considering Q4 FY16 was loss making and the company should be posting profits for Q4 FY17.

Going by my estimate of Rs.1.2 lakhs per MT of e-Waste revenues - this seems to be looking at a capacity utilisation of about 8000 MT. Assuming a 20% margins on this, should add around 20 Crores to the PAT in the near term for FY18 at the very minimum. This is almost double the current TTM PAT of Rs.11.39 Crores.

Again, there is a lot of speculation here but I am hoping this is all still quite conservative.

I have not gone through the company fundamentals so this is based purely on what I have read in this thread. Equity dilution or any potential equity dilution is a big red flag. There have been enough experiences of companies - read the thread on cebco - where equity dilution often portends trouble ahead. I am not saying that this may be a problem with this company but seniors have given warnings about companies doing this. So I would be doubly cautious. Thanks - Bheeshma

Normally, a waste recycled businesses have very high margin and ROCE. That is due to lower (rather nil) input cost while value of sales (from metal/plastic etc) has marginal discount to primary/virgin products. I could not understand why the conpany with Rs 200 Cr sales have not even 1% margin. It is worse then trading business also. Look at GRP Ltd (recovering rubber from used tyre) for kind of comparable. I would suggest all members to do proper due diligence. Also, in current state of market, share prices are more driven by hope and hype then happening. So, please consider once investment style and risk profile while evaluating such small cap companies.

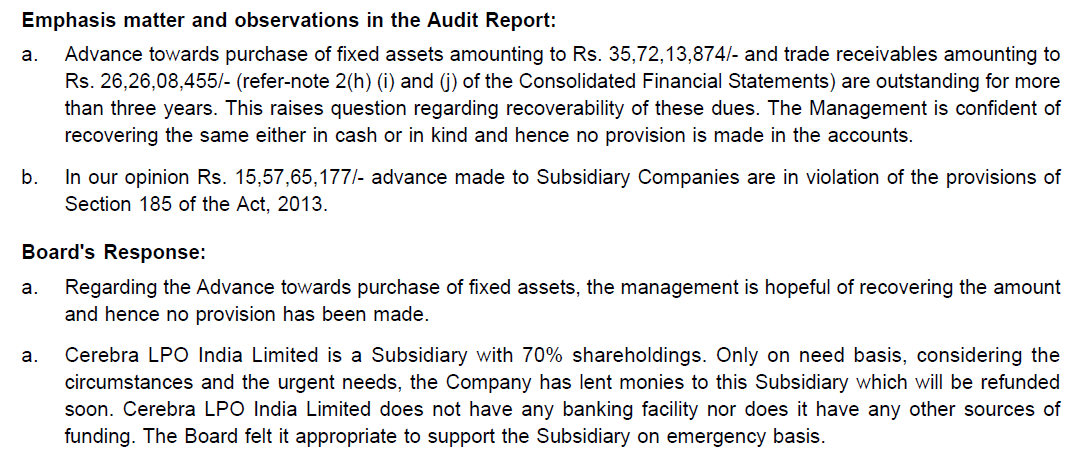

Also, find enclosed auditor commment and management response for financial FY16.

On a slightly different note, i had started a thread sometime back ( link below ) - i find a direct application of this here using cerebra as a case study. Please note - this has nothing to do with the cerebra business - i am just using it as a case study ( though i find the name of the company super duper cool!)

Their e-Waste plant is yet to contribute to revenues and should start doing so in the coming quarters. That could explain the margins being as they are at present as its from their hardware manufacturing business. e-Waste margins should be much higher. 1 MT e-Waste should yield a revenue of 1.26 lakhs while costing under 20k per MT. Margins should be higher here but e-Waste should just be about 30% of their topline in FY18 at its best so I don’t expect margins to improve drastically even when e-Waste plant contributes to the numbers.

As for trade receivables, in the more recent Sept quarter results, they have an updated balance sheet which puts their trade receivables at 13 Crore, down from their 26 Crore number in the AR FY16.

Talking of margins, I don’t think e-Waste businesses will ever have margins like a tyre recycling business. e-Waste recycling involves manual labour intensive process of stripping the components and the power intensive process of smelting to separate the materials. I doubt if these two can be compared in terms of margins. I would be surprised if the margins are over 30-35%. Hard to find a comparable business that has disclosed margins although there is a competitor named Attero which has been doing this for years. Numbers not in the public domain unfortunately.

The point to highlight risks. The company too many uncertainities. They are getting into business they do not have any experience. They paid capital advances and receivable which are not provided for and shown as good in balance sheet. They have related party transactions for which there are comment from Secreatrial auditors. They have lowest margin, even lower than hardware trader. I find it difficult to believe on management guideance and invest. However, higher the risk general perception is better the return. My limited point is every investor should do its own due diligence before investing and I always like to highlight what can go wrong then what can go right. As extent of right would determine the profit, but extent of wrong has capability to wipe out whole investment.

In case you have considered all risk and you trust the management, wish you all the best for your future investment.

I do not know about big company but I know one of the small traders in this business. This is a high risk high return type of business. They usually have some e tenders to win. And there are lot of middle men. If this company can cut off the middle men then it can do well otherwise it’s a very risky business.

They seem confident going by the capacity they are building. Once their capacity target of 96000 MT is built, they will be Asia’s largest e-Waste recycler. I remember reading in either their results presentation or AR that they have the supply chain in place for sourcing e-Waste and closing the loop on recovered materials. Being present in the hardware manufacturing business and supplying to most IT companies and PSUs, I expect them to have the knowhow. They are currently doing refurbishing and also recycling on a smaller scale. There is a definite risk which should start reducing as we see numbers in the coming quarters.

Up 17% after the long consolidation and triangle breakout. Everything now depends on the results of next few quarters to see the new eWaste refining plant’s contribution to topline and subsequent margins.

From 10.85 Crore shares to 12.57 Crore shares (1.19 Crore pref allotment and 53 lakh warrants to promoters) in March this year. That was done at a price of Rs.40.then. The reason given for raising capital was to extend the capacity of the e-Waste business from the 36000 MT which was recently built to the targeted 96000 MT.

Now again they are at it. This time again its the same 1.19 Crore shares pref allotment to the same fund (Kuber Global Fund) and again 53 lakh warrants to promoters taking the total no. of shares to 14.29 Crore shares. Price is not yet disclosed but considering that the current price as of announcement is around Rs.53, this should be somewhere in the Rs.50-Rs.60 range.

Considering that the recent capex has not yet showed results (e-Waste refining plant operational only from this month), why is the company raising so much capital and diluting equity almost 30% in a year. Should I be happy that they are able to raise capital at these much extremely elevated valuations? (Last year Cerebra was trading around Rs.15 and now around Rs.53) or is there a catch to this somewhere?

Assuming the worst that this is a pump and dump operation, what surprises me is they are able to get funds at these elevated valuations. They raised close to Rs.50 Crore from a fund in March through preferential allotment of 1.19 Crore shares at Rs.40. And now again they are more funds through the same fund. Why would someone invest Rs.100 Crores at these elevated valuations? That is something I haven’t been able to answer. The promoter is also shelling out over Rs.10 Crore for the warrants on the 1.06 Crore warrants issued this year.

From my research on the competitor Attero Recycling, they seem to have raised similar funds in 2014.

While overall they have raised $28.6 million, the most recent 2014 Series-C round raised $16.5 million which is around Rs.100 Crores. I did some research on the costs as well. It looks like it takes $2 million for 2000 ton capacity.

Going by this, 100 Crores would get about an additional 15000 MT of capacity to the current 36000 MT installed capacity. The numbers seem more or less right with what the management is claiming. Am hoping there is more to this than a pump and dump so will watch closely.

Total revenue from 1 Ton of E-waste is Rs58535.

All plants operating at average 25% to 30% capacity due to bad supply logistics.

Average Capacity Utilization around - 96000*30%= 28800 MT

If the plants run at this capacity by the end of 2018.

The total revenue generated will be around =168Cr

Bangalore itself produces around 18000T of waste per year. So Cerebra plants can handle about 5 big cities like Bangalore. Which means it can recycle most of the country’s metropolitan cities.

The only factor here is how much investment is put in developing the plant and what returns are expected out of it and at what rate.

Which can only be Seen after the plant is operational for a couple of quarters.

If they can deliver this type of result in the next 3 years this stock is worth buying.

@phreakv6 the capacity they are talking about is 96000T not 96000MT