@DAB - The pdf is from 2013 and my estimates are from 2017 so that could explain the difference in calculations. Also, the recoverable amounts were from their investor presentation based on the technology they have.

The capacity they have built which is operational is only 36000 MT (Metric Ton) and I am not sure when it will start adding to their numbers in any significant fashion. The management has promised many things in the past none of which have materialised. The most recent is 100 Crore topline from e-Waste business in FY18 (Promised sometime last year). I don’t think they are anywhere close to this number, unless their revenue recognition is such that we get a positive surprise in Q3/Q4 which again I don’t have very high hopes for.

@agferrari - This keeps happening in this stock. It has moved in pretty peculiar fashion and has not followed any semblance of Price/Action and Supply/Demand. I think Rs.40 will be sort of a bottom though since this is the price where significant dilution has happened (Almost 30% dilution through Pref allotment and Warrants).

Disclosure: Holding significant quantity and been buying since Rs.17. Last purchase over 6 months back.

Warrants , Preferential share & Mauritius forms a really good Cocktail & have given even better hangover to investors in past.

Right now you must be feeling high just be aware of hangover might follow soon.

@phreakv6, the diluted share capital as per sep qtr is at 120.38cr. I dont see any further warrants/dilution pending. Can you confirm if there are any? This qtr results at 7cr bottomline looks good. Would be interesting to know how much is being contributed by the new e-waste plant and its current utilization levels.

25% of the equity base by volume gets traded in-between and as if on cue, the new year has moved the price from 40 to 60 levels and post notice, a 10% correction. Nothing smells right.

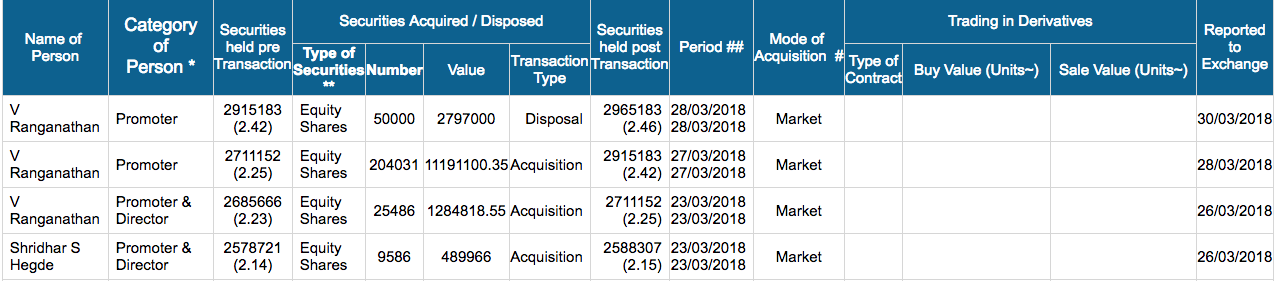

Promoters buying. The one on 30th March is also Acquisition marked as Disposal incorrectly. These purchases are definitely not from open market having observed the price action in this scrip for well over a year now. These must be from SSJ Finance which has been accumulating for awhile. Everything here is shady of course. Best case e-Waste business is going to contribute well going forward, worst case this is a pump-and-dump operation in concert with the Promoters and some FPI entities (probably round-tripping money from some receivables that have been pending for years and some other transactions done years ago)

There is a possibility of a 1000 Cr market cap post Q4 results. It is still a mystery if this is a pure pump-and-dump or if there is some semblance of business underneath.

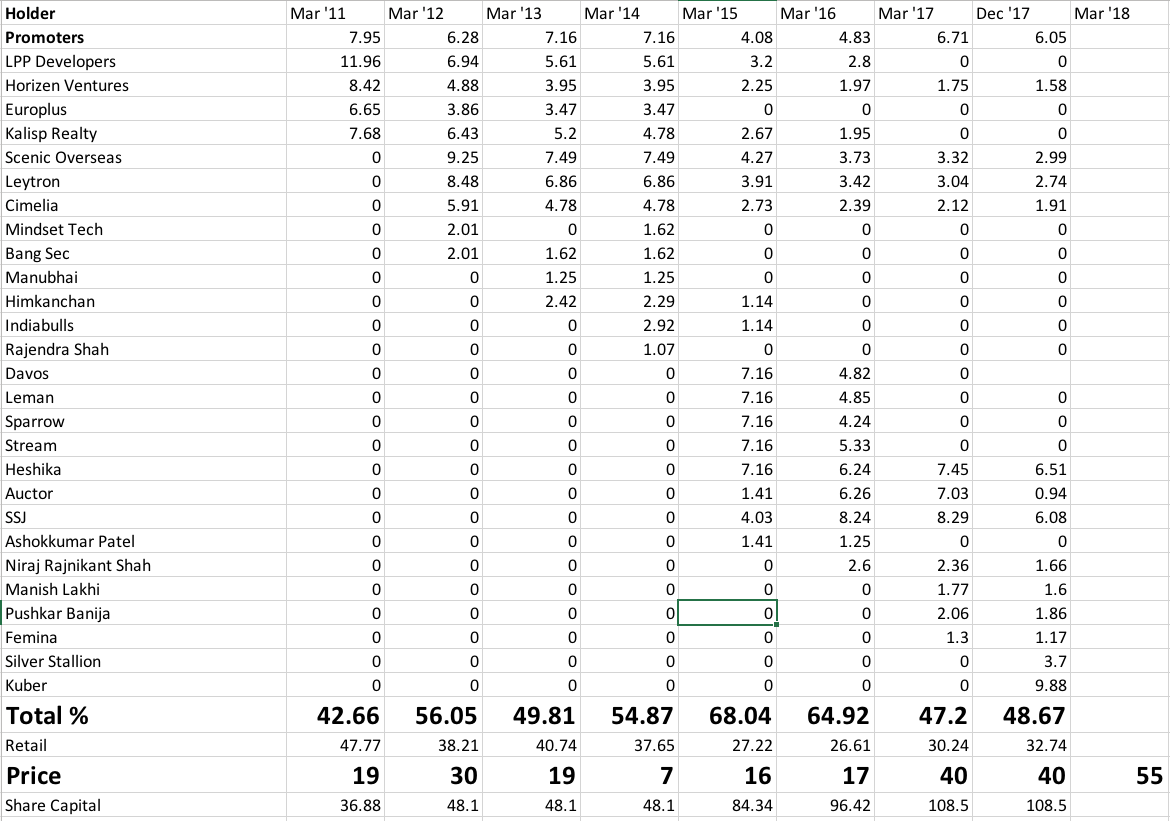

Having done a detailed shareholding pattern analysis

I think the management has round-tripped a lot of money via Mauritius and grabbed equity via FCCB (between 2015-2017). I believe promoter and PAC shareholding here should be seen as sum of promoter holding + Heshika + Auctor + SSJ + Silver Stallion + Kuber. Scenic + Leytron + Cimelia was an advance given in 2010 for e-Waste technology from Cimelia in 2011 which they never got and the high court has barred them from selling or benefitting from that in any way so in the future there is a possibility of the company extinguishing that part of equity through a buyback. Then there is the problem of large receivables pending for a long time. Lot of things which I suspect may all fall in place if the e-Waste business is in fact legit. Otherwise this is just cooking the books for a plain pump and dump. Tempted to trim the holdings but being watchful. I am more interested in the shareholding pattern here than the P&L. That’s saying something.

Super observations form data. Really i liked your way of interpretation of data, it may be wrong but i think at present situation we have to be careful. I have burnt my fingers in these types of news oriented stocks.

Results look good with sales up 91% YoY and PAT up over 10x.

I was looking for a 25 Cr PAT for FY18, they have posted 35 Cr. At current mcap, its trading around 21 P/E. They claim a phenomenal e-Waste contribution. Nothing except a dividend will prove the cash is real though.

Receivables still high but considering sales have gone up considerably (20% YoY with Q4 alone contributing 42% of yearly sales numbers), perhaps its not too bad. Still holding 70 Cr cash (10% of mcap from the dilutions) with zero debt. WC has gone up.

Auditor’s remarks on some receivables still remains same for years and so has management’s response. Still ambivalent on the legitimacy, still holding.

@phreakv6 The promoters have been buying the stock in past few months. Are you stil tracking the company. Their additional plant was planned to be operational in December 2018.

Cerebra Integrated Technologies Limited undertakes EPR commitment of LG Electronics as its second EPR client to collect and recycle E Waste for the FY 2019-20.