I am invested in both Genesys and Ceinsys. I think Ceinsys has beaten down too much for what it’s worth. Agree with Genesys being a company in a lot of promising sectors but Ceinsys is not all about JJM anyway. They have an order book that can sustain them for a year or more. Investors are behaving as if JJM was the only thing going for them and after the 50%+ crash, the market seems to have completely removed JJM contribution from the equation.

5 Likes

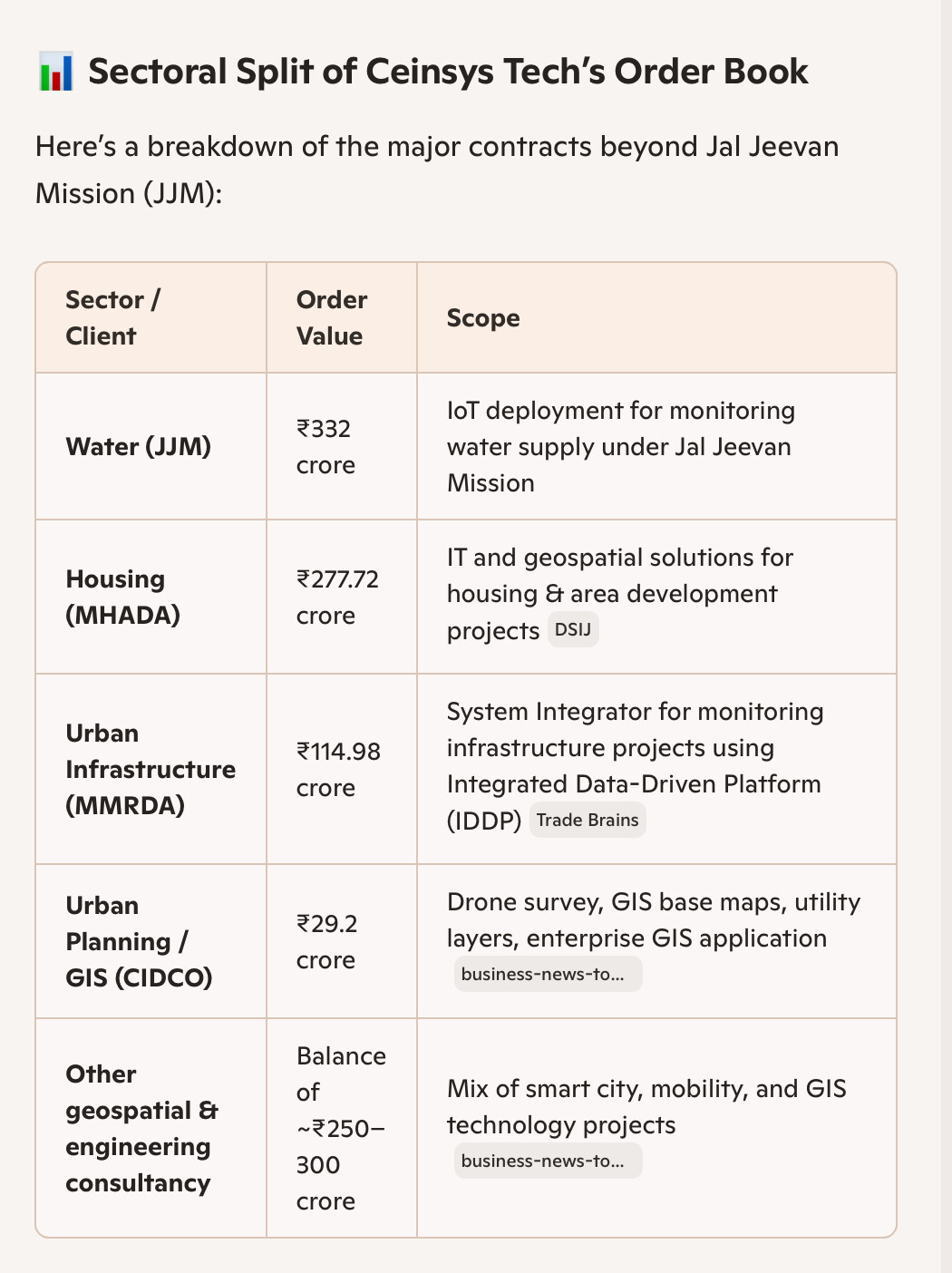

Its not all JJM and its not pipeline fitting work either .Ceinsys has lot of other things under the hood apart from what the public perception is .Their US aquisitions allygrow and VTS is also into auto sector and has Lidar etc. capabilities .

Its not that Ceinsys can’t do what genesys can . ceinsys wanted to pivot away from geospatial and B2G because of this Gov specific issues and thats why they bought those two and will buy a couple more in next few months . They are still sitting on the QIP cash done when when the price was 600 or so.Its not really Ceinsys’s fault that too many order hunters got onboard and is now jumping out not knowing whether they boarded a bus or a train .

On the other hand, Genesys is also very much Gov order dependent as things stand. apart for ADAS , all the others you mentioned are for various gov clients only(state and municipal as well) .

Also the orders declared about land digitization and city twinning till now are tiny in amount compared to the expectation .Plus, promoter holding goes down every quarter,dilution happens frequently and there is pledge as well .Both of these have not actually bloomed yet and have potential .In short ,while Ceinsys has shown clear ability to generate revenue and profit( JJM cash will come too …sometime) ,Genesys is still vague about the monetisation path of their tech stack. If the ADAS is licensed to a few other OEMs , things will be much better .

6 Likes

Hi Sir, how did you came to this potential annual figure ? Any source helps. thanks

Actually I used screener AI for estimated market size, it came around 600 cr

Constructive debates are always good for investors. Genesys is leader in twin map and land digitization. India

TAM for twin map city is roughly 6000 cr, globle TAM is 35000 cr.

TAM for land record digitization is between 4000 to 6000 cr

TAM for other utilities including water, Power is close to 5000 cr

ADAS digital twin TAM is 500-2500 cr per year

Infra, forest, flood environment TAM is 3000 cr upper limit

Total estimated opportunity size by 2030 for all twin map scenarios is between 5-7 B USD.

Ceinsystech is working in utilities domain only. If JLR ties up with Genesys for ADAS tein maps at global level than it shows what capability Genesys Maps offer.

Nothing against Genesys or Ceinsystech, i follow pure valuation methods and exited both in Dec 24 at peak levels as PE was too high to hold. My preference is genesys and today bought my second lot. Third lot if price come down to 350 levels which will be mouth watering.

Regarding promotor selling, Sajid John’s wife Sazia Ilmi opted for divorce and sold her stake.

7 Likes

This is my last post about this matter …at the moment I am not even sure whether we are in the ceinsys page or the page for genesys.Leaving aside which one we fancy more..

Genesys has no deal with JLR yet afaik.However it has 3 deals..

- With Tata motors PV for their SDV suit .TM is going to use genesys mapstacks for Indian roads in their SDV for next 6 years.

- HERE maps. Here will use Genesys maps for India in their product which is used by BMW,Mercedes,Audi .In this also,the maps are of Indian roads that goes into the product as a part.

- TomTom. Same as point 2 but for Renault and Stellantis.

Point is ,no foreign company can generate the Indian maps genesys has because of gov policy and genesys is indeed miles ahead of Indian competition here .

Almost same situation is Digital twinning of cities .Competitors are far behind. However, for land digitisation there are many other competitors like C-DAC,NIS,various local GIS, mapmyindia ,rolta etc. Ceinsys (The 29 crore CIDCO project) as well but not every company does every aspect.

Regarding the TAMs …take them with a pinch of salt.Genesys has good advantage in India but for outside India ,there are foreign competition who are far more powerful.

So I agree,Genesys has great scope in certain things and at the moment the ADAS is the most hopeful thing because those deals must be worth large amounts .I wish Genesys provides some fiscal details on those. They are very secretive and do not seem very concerned about their stock price .

I will not go into what Ceinsys has…because I was not and will not try to convince ! :)

11 Likes

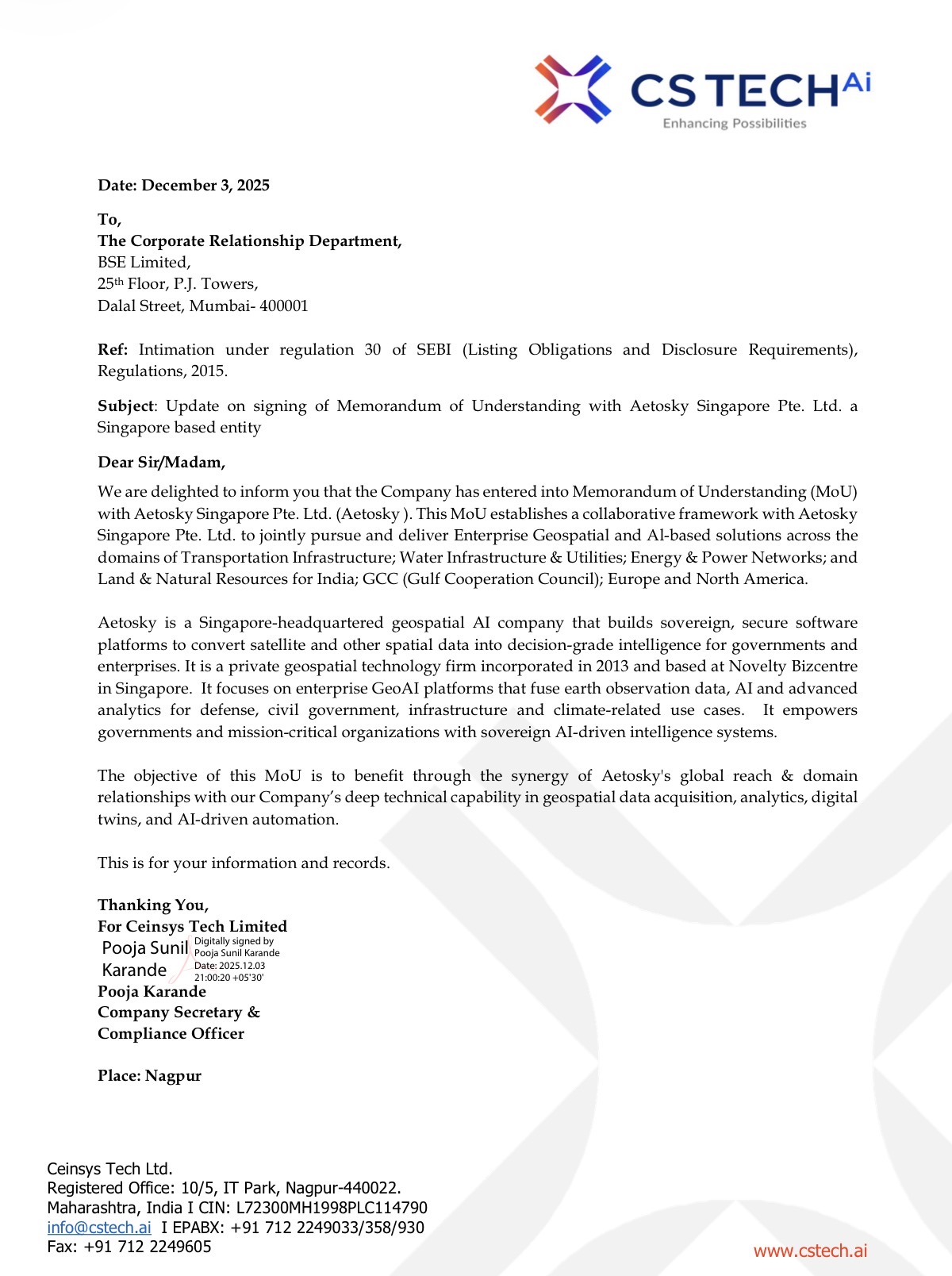

Ceinsys Tech Limited has informed BSE that it has signed a Memorandum of Understanding (MoU) with Aetosky Singapore Pte. Ltd., a Singapore-based geospatial AI company.

Under this collaboration, the two companies will jointly develop and deliver enterprise geospatial and AI-based solutions across sectors such as transportation infrastructure, water & utilities, energy & power networks, and land & natural resources. The partnership will focus on markets including India, the GCC region, Europe, and North America.

The alliance aims to combine Aetosky’s global reach and domain expertise with Ceinsys Tech’s strengths in geospatial data, analytics, digital twins, and AI-driven automation to deliver advanced, decision-grade intelligence solutions for governments and enterprises.

8 Likes

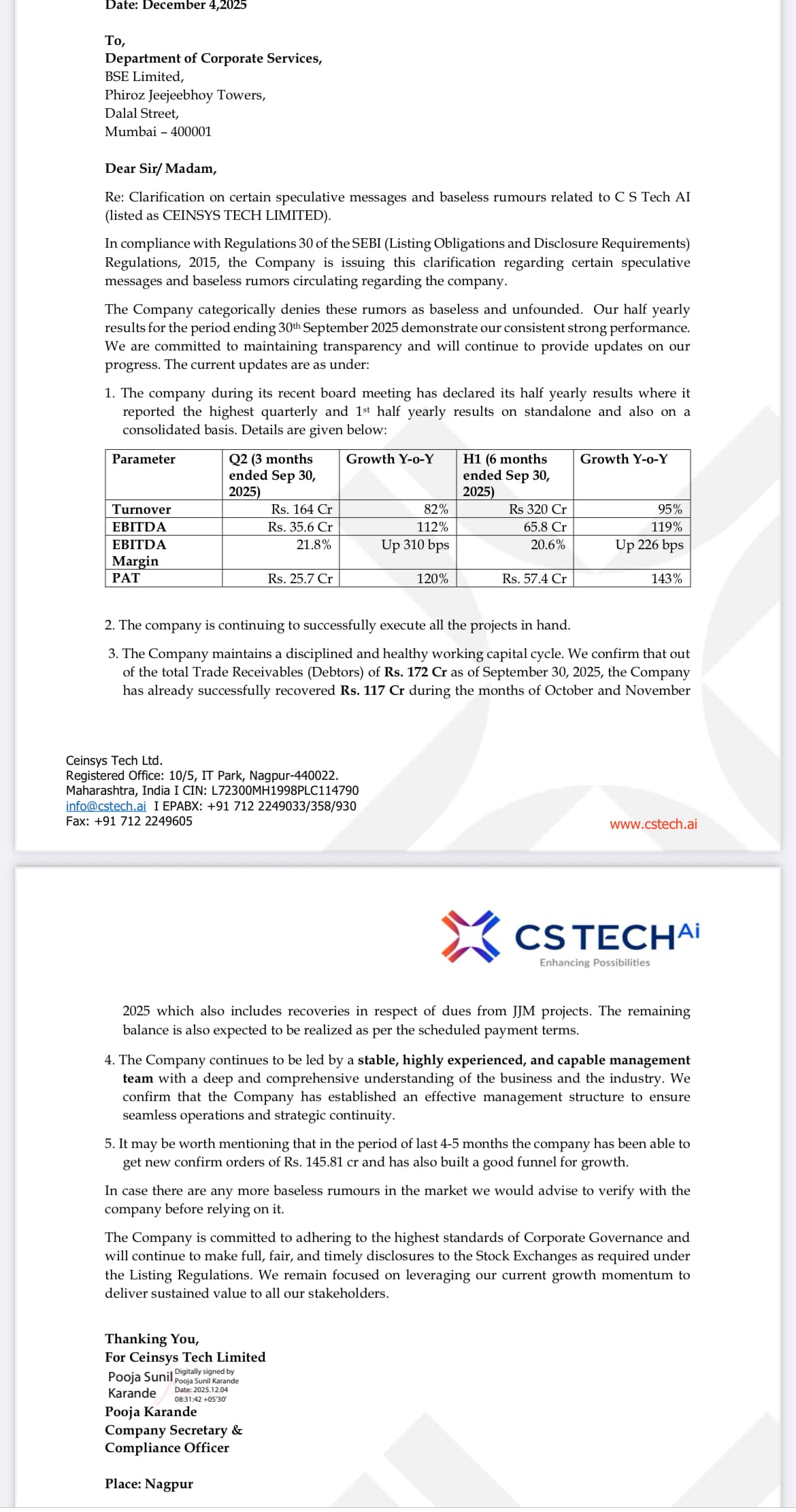

A note released by the company, somewhat answering many rumours circulating around. Again could be the price action that’d made the management take this step.

Disc: No reco

4 Likes

What rumours is the company referring to exactly here? I don’t see any specific ‘rumor’ being mentioned in the release. Not sure why they would need to come out with such a release except to stabilze the price action.

2 Likes

They are probably referring to rumours that the company is going to write of JJM receivables hence they have highlighted the fact that they have started recoveries and already recovered 117 out of 172 Cr as conveyed in the latest conference call.

It’s likely that some investors contacted management after the price drop to seek clarification, which may have prompted this response. While I generally don’t favour management intervening to influence the stock price, this appears more like an investor friendly effort to provide reassurance rather than an attempt to artificially boost the price.

24 Likes

Company made the announcement today that it’s going to be listed on NSE as well to increase shareholders participation.

2 Likes

Jal Jeevan Projects awarding restarted based on todays SPML infra 207 Crore order win - https://www.bseindia.com/xml-data/corpfiling/AttachLive/dd252c05-dabf-4009-99d1-8131331be8fb.pdf

9 Likes

K.P surej resigned, CMO resigned..

Promoter Sagar Meghe will take incharge of the company..

There could be an internal rift that is resulting in this vertical fall.

First, Surej is retaining his leadership at the US subsidiary (TA Inc), so the international growth engine remains intact. Second, the vacancy at the parent level looks suspiciously similar to the pre AllyGrow era. My speculation is that a new acquisition is locked in, and just like Kamat post AllyGrow, the incoming CEO will come from that target company.

However, until that is confirmed, Sagar Meghe’s shift to ‘Whole Time Director’ is a red flag. If the acquisition theory doesn’t play out, we are looking at a promoter run business again, which changes the investment thesis.

7 Likes

Ceinsys Tech Management Timeline - December 2024 to December 2025

Here’s a cleaner chronological breakdown organized by key events:

Early 2024 (Feb-May)

Incoming:

- Feb 13 - Mrs. Maya Swaminathan Sinha joins as Non-Executive Independent Director

- Mar 30 - Mr. Kaushik Khona joins as Additional Director & MD India Operations

- May 27 - Mr. Samir Sabharwal joins as Joint Chief Financial Officer

Mid-2024 (Jul-Aug)

Outgoing & Transition:

- Jul 10 - CA Amita Saxena (CFO) resigns

- Aug 12 - Mr. Samir Sabharwal promoted from Joint CFO to sole CFO

Transition:

- Nov 6 - Mr. Surej Kunhithayyil Poyil steps down as Whole Time Director (but continues as Non-Executive Director & CEO Designate)

Year-End 2024 (Dec)

Loss:

- Dec 14 - Late Shri Hemant Thakre (Chief Administrative Officer) passes away

Early-Mid 2025 (Jan-May)

Incoming & Promotions:

- Jan 17 - Mr. Rohan Singh joins as Executive Vice President - Strategic Initiatives

- Feb 11 - Mr. Prashant Kamat re-appointed as Whole Time Director, Vice Chairman & CEO (3-year term through Feb 16, 2028)

- Mar 26 - Mr. Surej Kunhithayyil Poyil designated as CEO Designate

- May 3 - Mr. Phaneesh Murthy joins as Non-Executive Independent Director (5-year term)

- May 3 - Mr. Surej Kunhithayyil Poyil promoted to Executive Category Additional Director

Late 2025 (Dec)

Major Restructuring:

- Dec 16 - Mr. Sagar Meghe elevated to Whole Time Director & Chairman

- Dec 16 - Mr. Surej Kunhithayyil Poyil resigns (focuses on USA subsidiary operations)

- Dec 19 - Mr. Vishal Pawar (Chief Marketing Officer) resigns due to personal reasons

Quick Count:

- Total Incoming: 5 new appointments

- Total Outgoing: 4 resignations/departures

- Total Promotions/Transitions: 7 role changes

There has been too many role changes hopefully get some clarity in Q3 Concall, they should do a call explaining their exact strategic outlook

20 Likes

The Art of Finding Optimism in a Board Resignation

Ceinsys has been aggressively expanding its footprint in the US through its wholly-owned subsidiary, Technology Associates. Following the acquisition of VTS in July 2024, the company has integrated high end geospatial capabilities alongside its legacy automotive engineering business.

The VTS team specializes in bringing cutting edge 3D LiDAR scanning, imaging, and data processing technologies and workflows to customers in Telecom, Utilities and other Infrastructure segments by having developed a world class capture operations team with a nationwide network of 3D capture professionals, drone pilots, and data experts.

Part 1: What Work Does Ceinsys (via TA) do in GIS?

Technology Associates now operates a specialized geospatial and “Digital Twin” vertical, leveraging the assets and capabilities acquired from VTS. This division focuses on creating precise digital replicas of physical infrastructure to solve critical utility challenges.

The company uses technologies like LiDAR scanning, 360 imaging, and drone surveys to map physical assets, such as water treatment plants, university campuses, and utility networks, creating interactive 3D models utilized for remote management.

The problem of “The Invisible Infrastructure”

US based water and utility companies require geospatial mapping (GIS) because their physical assets are widely distributed, often buried underground, and constantly aging. Without this technology, these companies are essentially flying blind.

- In the past, utilities relied on paper maps or employee memory. If a pipe burst, crews might dig blindly, hitting gas lines or wasting days finding the leak.

- GIS creates a “Digital Twin” of the underground network. A field technician can look at a tablet and see exactly where a pipe is, its depth, and its material (e.g. PVC vs. Lead) before they start digging.

- US water utilities lose an estimated 14% to 18% of treated water to leaks. By overlaying flow sensor data onto 3D maps, utilities can pinpoint leaks to specific city blocks rather than inspecting miles of pipe.

Secular Tailwinds for GIS:

- As senior utility workers retire, they take decades of institutional knowledge with them. Geospatial mapping digitizes this “tribal knowledge,” ensuring new hires can locate valves and assets they have never seen before.

- The EPA’s “Lead and Copper Rule” requires utilities to identify and replace lead service lines. GIS allow utilities to color-code service lines by material to prove regulatory compliance.

- During events like deep freezes or hurricanes, GIS command centers allow utilities to visualize clustered outages and prioritize repairs for critical facilities like hospitals.

Part 2: Ceinsys Involvement with the US Government Ecosystem

Ceinsys has secured entry into the US Public Sector ecosystem through strategic sub-contracts and channel partnerships.

Proof 1: The Fugro Order

Source: Ceinsys Tech receives service order from Fugro USA Land Inc | Capital Market News

- Fugro is not a commercial developer; they are a massive geo-data specialist whose primary clients include US State Departments of Transportation (DOTs), the US Geological Survey (USGS), and the Army Corps of Engineers.

- By winning a service order from Fugro USA, Ceinsys is effectively acting as a Tier 2 supplier.

- Order proves Ceinsys meets the technical quality standards required for US Government work, positioning them to eventually (possibly?) cut out the middleman.

Proof 2: The Maintenance Care Partnership

Source: We Just Made VR Maintenance Management More Affordable

- VTS (the Ceinsys US arm) is the exclusive VR/3D partner for Maintenance Care.

- Maintenance Care is a CMMS (Computerized Maintenance Management System) provider whose client base heavily includes “Local Municipalities, Housing Authorities, and State Agencies.”

- Ceinsys integrated its 3D viewer directly into the software that city managers already use. This serves as a frictionless distribution channel into the public sector.

Part 3: Thesis - Why Surej Had to Resign Due to US Government Rules

On December 16, 2025, Ceinsys filed a disclosure stating that Surej KP resigned as a Non-Executive Director and CEO Designate of the Indian parent company to focus completely on leading the US subsidiary, TA Inc.

While this looks like a simple role change, it is likely a mandatory compliance move. Under FOCI (Foreign Ownership, Control, or Influence) regulations, the US government identifies specific individuals who must be cleared to hold a Facility Security Clearance (FCL).

- The CEO is always a mandatory Key Management Personnel (KMP). Having John Chwalibog (Head of Geospatial), a US citizen as a division head is not enough.

- The Conflict: If Surej (the US CEO) simultaneously sits on the Ceinsys India Board, he has a legal fiduciary duty to Indian shareholders.

- The Violation: The US Government views this as a direct conflict of interest. You cannot hold a US Security Clearance if you have a competing fiduciary duty to a foreign entity.

Why John Chwalibog (US Citizen) wasn’t enough:

- John’s Role: He is the “Operational Face” for clients; he sells the work and manages the projects.

- Surej’s Role: He is the “Legal Face” for the government; he signs the liability and holds ultimate authority. The US Government requires the liability holder to be free of foreign influence.

Why give up the prestigious “Group CEO” title?

The answer lies in “32 CFR § 117.11” of the US Code of Federal Regulations. (Source: ECFR - 32 CFR § 117.11)

- To bid for US contracts involving sensitive geospatial mapping of Critical Infrastructure (like energy grids, dams, or defense adjacent utilities), a company needs an FCL or must undergo a specific FOCI assessment.

- The Defense Counterintelligence and Security Agency (DCSA) considers a US facility to be under “Foreign Influence” if its KMP, specifically the CEO, holds a position on the board of the foreign parent.

- The Fix: By resigning from the Indian Board, Surej effectively “Americanizes” the leadership structure. He is now legally liable solely under US jurisdiction, removing the FOCI “Red Flag.”

Why City work (The Fugro Order) was Safe, but Federal work required a Change

- The Buy American Act (41 U.S.C. §§ 8301–8305) restricts purchasing foreign goods (steel, iron) but does not strictly ban foreign services at the municipal level. Major foreign firms like Arcadis and Veolia manage water systems for US cities daily. Ceinsys (via VTS) could legally service municipal clients like Fugro even without this resignation.

- However Federal and Defense-adjacent work (Tier 2/Covered Contracts) triggers FOCI mitigation.

-

32 CFR § 117.11 states that a company under FOCI is ineligible for a clearance unless it implements specific mitigation measures.

-

DoD Instruction 5205.87 (issued May 13, 2024) dramatically expanded these rules. FOCI assessments are now required even for unclassified contracts with a value of $5 million or more if they involve sensitive supply chains or data.

-

Surej’s resignation is the textbook execution of this mitigation, creating the necessary governance firewall to bid on these sensitive contracts.

-

The US Government offers a menu of ways to fix the “Foreign Owner” problem. Ceinsys appears to be executing Option 2:

- Voting Trust: Parent gives up ownership. (Unlikely).

- Special Security Agreement (SSA): Parent keeps ownership but builds a strict firewall. (Most Likely).

- Proxy Agreement: Parent keeps profits, but voting rights go to US Citizens.(Possible but unlikely).

Therefore, if Surej had not resigned, Ceinsys would likely be ineligible for the necessary security agreements required to bid on contracts governed by DCSA rules.

- Does the resignation instantly give them a Federal Contract? NO

- Does the resignation make them eligible to sign the agreement that gets the contract? YES

What Happens Next?

Since Surej has resigned, I am expecting the company to be silently executing Option 2 (SSA) right now.

The SSA Process:

- Step 1 (Done): CEO Resigns from Foreign Board.

- Step 2 (In Progress?): TA Inc. forms a new Government Security Committee (GSC).

- They must hire 3 Independent US Citizens (Outside Directors) to sit on the TA Inc. board.

- These 3 US Citizens will legally have “Security Supremacy” over the Indian owners.

- Step 3 (The Goal): DCSA signs the SSA. NOW Ceinsys (TA) is “Cleared” (Qualified) to bid for sensitive US Government GIS contracts.

Disclaimer: Invested & Extremely Biased. I hold zero law degrees; I just have an internet connection and too much free time. I was bored, went down the rabbit hole, and surfaced with this theory. Treat this as “Regulatory Fan Fiction” until proven otherwise.

58 Likes

Did you get it validated by the mailing to the company?

1 Like

Announcement under Regulation 30 (LODR)-Award_of_Order_Receipt_of_Order

Ceinsys Tech Ltd-Management Meeting KTAs

CMP INR 1,066 | Market Cap INR 1,902 Cr

Board Member clarity

Mr. Prashant is retiring from executive responsibilities but will continue as an Independent Director, ensuring continuity in governance and strategic oversight.

Sagar – Executive Chairman

Kaushik Kona – India

Abhay – Business Development

Surej – International Business

Phaneesh – Independent Director on the Board

Management stated that the promoter’s appointment as Executive Chairman is aimed at sharpening focus on US and international expansion, with Suraj’s role realigned solely to drive overseas growth, clarifying this as a strategic strengthening move rather than any performance-related issue.

The acquisition is sizeable and not a INR 2–3 cr business. It is largely focused on the US market.

There is INR 240 cr of unbilled revenue, which is realized as per contract terms over a period of 60–90 days. None of this revenue is static.

JJM

September quarter contribution is expected to be ~<25%, depending on project execution, project stage, and contract structure. The company has better capabilities than peers, particularly in execution. CS Tech is strong in geospatial solutions and is capable of delivering across multiple infrastructure projects, with geospatial being the core focus.

The company has strengthened its CMO function and built a strong marketing team.

River Linking

Revenue has already been accounted for over the last three quarters. Other river-linking projects fall under priority sectors and have strong credit profiles. While river-linking projects are inherently challenging, execution is ongoing and remains on track.

Working capital

Improved materially, with ~INR 120 cr of receivables recovered post 30 September effectively, entire September debtor levels have now been recovered. Over the last 3–4 quarters, the working capital cycle has improved materially, trending towards ~105–150 days, aided by better order selection and milestone-based billing.

Q3 performance tracking in line with Q1 and Q2 trends, indicating continuity of growth momentum.

Order book

Order book stood at ~INR1,100 cr as of 30 September, with ~INR 108 cr added subsequently, while management reiterated a diversified, company-wide FY25 exit order inflow target of INR 700–800 cr across JJM, urban infrastructure, energy, and municipal segments, with real-time disclosure of new wins.

Management clarified that the INR 108 cr order pertains to JJM, which was never discontinued, with delays stemming from temporary state-level audit pauses; ~INR 118 cr of receivables have been recovered, execution is normalizing with traction expected from Jan–Feb, and JJM will remain a key but not sole growth driver*.

Geospatial remains the company’s core backbone, with mobility and AI positioned as horizontal enablers embedded across all verticals, while expansion into GCC and Europe will be pursued via a direct-to-client model rather than subcontracting.

Cost Structure

The operating cost base is largely people- and technology-driven, with manpower costs being the key cost driver. This remains central to the company’s execution-led delivery model.

Order Conversion Rate

The order pipeline-to-order book conversion rate is strong at ~80–85%, as the company selectively bids only for projects where it has clear execution capability and competitive advantage.

US Subsidiary

The US subsidiary has never been loss-making. It has been profitable throughout and serves as the primary vehicle for investments and expansion in the US market, making it the most efficient structure for scaling international operations.

Arihant Capital notes.

32 Likes