I think negative has been fairly documented in the thread on Order book slowness, acquisition delay and Receivables etc, i saw certain important positive indicators during the last concall which are listed below

- Consolidated Level profitability

There are certain large contracts which are under negotiation also over there, and we expect to kind of give some kind of update on that in the Quarter 4. So, the investments which are happening and the standalone results are better than the consolidated. Your observation is right.

But I think what is the EBITDA negative is more of investment rather than expenditure.

So, if you look at this quarter also, we expensed out around Rs. 7-8 crores. And that is what has been happening in the last two-three quarters because we are substantially investing into the business development in the U.S. market. The result of this is what we are expecting, as we already clarified in the previous investor call, in the Quarter 4 of this year and Quarter 1 of the next year onwards, we should see a bigger pipeline.

- Order Book pipeline and Win rate probability

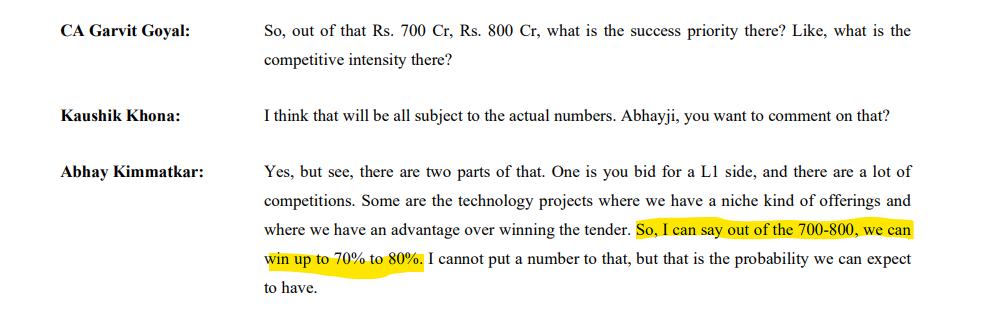

CA Garvit Goyal: So, out of that Rs. 700 Cr, Rs. 800 Cr, what is the success priority there? Like, what is the competitive intensity there?

Kaushik Khona: I think that will be all subject to the actual numbers. Abhayji, you want to comment on that?

Abhay Kimmatkar: Yes, but see, there are two parts of that. One is you bid for a L1 side, and there are a lot of competitions. Some are the technology projects where we have a niche kind of offerings and where we have an advantage over winning the tender. So, I can say out of the 700-800, we can win up to 70% to 80%. I cannot put a number to that, but that is the probability we can expect to have.

- Acquisition Revenue range

Darshil Jhaveri: So, what is the rough size of it? Like, for example, a Rs. 50 crores company or Rs. 20 crores

company? I don’t want an exact figure, but a rough range, okay, this is what we are looking at

because we have improved our margins and everything very well. So, will it be margin accretive,EPS accretive? Just any kind of color on that would be really good. This is what we are looking at. I know whatever closes, then that closes, but at least that is a filter for us.

CA Amita Saxena: Kaushikji, please, you can take it.

Kaushik Khona: See, as I said, I don’t want to speculate. And if you have seen our intentions, we have already mobilized $28 million, which is Rs. 235 crores. So, our target is not to look at Rs. 2, 5, 10 crores company, small companies. We are looking at companies which have a potential of either generating a revenue of Rs. 50, 100, 200 crores is what we are looking at.

So, let’s keep our fingers crossed. Let’s wait for some more time. We have waited enough, and I think in the next one or two months or maximum by the next one quarter, we should be able to give some kind of good news.

- US Sales & Marketing effort results

Nirvana Laha: Give some color on what these employees are exactly going to do for us?

Kaushik Khona: No. So, these employees are. Surejji, you are there?

Surej K. P.: So, just to answer your question, the focus is way beyond what VTS was doing beyond telecom.The idea is to take the capabilities that we have developed outside the U.S. into the U.S. market.

So, there is active engagement with customers across multiple domains which are a stronghold ,which is in water, in telecom, in utilities, also road transportation. So, it is broader. Obviously, the mobility business continues to grow from an engineering standpoint. So, these are all the areas that we are targeting to engaging and growing the businesses outside of India.

Nirvana Laha: Good to know that. Last question on this one is, you have mentioned that the costs will sort of start tapering from Q4 to Q1. So, does that mean that the revenues will start growing and they will start absorbing the costs? Or are you saying that the costs on an absolute basis will start

going up?

Kaushik Khona: No, I think what I expect is the revenue will be substantially improving, which will absorb the cost.

- AI/ML Benefits

This is my last question. Like, sir, what are the AI solutions we provide to our customers which

help them in reducing costs?

Kaushik Khona: So, I had already mentioned in my speech that the present AI/ML solutions we are enhancing in-house, where we are trying to improve efficiency and reduce the cost of people, and also increase the turnaround time. So, I think at present, we are not selling this to the customer.However, we have done a good amount of, I would say, POC even for the other customers, and we have been successful with the kind of accuracy more than 95% as required by the customers.

We have also filed two patents for the kind of process technology which we have developed on this AI/ML technology.

So, I think presently, we have been focusing on getting efficiency benefits within the project which we are handling. Some of the projects which we have also used, I would say, also a little bit application has also been made in the river linking project, in the DPMS project. Some of the

projects have benefited because of the AI initiatives which we have taken.

Abhay Kimmatkar: I will add into that. Geospatial technology is more of a remote sensing kind of application, which is completely relying on the AI side. We have been doing a lot of tooling all this while, but since the advent of AI, we have been able to do a lot of efficiency in data processing, which has contained the costs and benefited the customer.

There are two direct benefits. One is the timeline wherein the delivery was happening. So, we are drastically reduced by 30%. And then, of course, the productivity on the cost side. So, those two are the major benefits we have got, and we have passed it on to the customer. As we have been on the core geospatial and data side, we have been able to do this advancement in our delivery side.

Disc: Invested