But is it separtely charged for Mutual funds? I mean if I already invest in stocks through Zerodha, I’d anyway pay the AMC charge. Does holding MF through demat mean I pay additional charge?

If not,it would not be a huge deterrent right?

But is it separtely charged for Mutual funds? I mean if I already invest in stocks through Zerodha, I’d anyway pay the AMC charge. Does holding MF through demat mean I pay additional charge?

If not,it would not be a huge deterrent right?

As per Zerodha, Demat AMC charge of 300+gst is collected, if your holding passes a threshold value and if not 100+gst.

In stocks, 13.5+gst is charged by CDSL on the sell-side and paid by the investor.

In MF, 5.5+gst is charged by CDSL on sell-side and Zerodha waived this for the investor and they said Zerodha will accept these charges. But I am not sure whether they pay this exact amount or they get in some agreement with CDSL for some reduced payment.

But in conclusion, we can safely say CDSL earning some money from mutual funds in their Demat

One interesting point which is ignored by many investors is just thinking CDSL as proxy play on Indian Capital Markets.

It’s actually a play on anything that is valuable and can be digitalised. Hence, it’s strong value migration play on digitalisation and not just capital markets growth.

In my earlier post in Dec’19 - I covered few examples like unlisted companies, commodity receipts, insurance, degrees etc. It can go further in future to land records, property deeds, rental deeds and much more.

Think about it.

Interestingly NSDL is now nearly half the size of CDSL with about 2.25 Crore active investors. See the NSDL statistics here. Not sure why NSDL is not trying to compete with CDSL in terms of pricing and server architecture. If they continue to let CDSL run at the current pace, NSDL will soon be a distant 2nd player and can affect its valuations significantly when they come up for listing (which may not be really far away).

Another interesting observation is that the consolidated revenue of NSDL for the year ended 31st March 2021 was 465 Crore and the profit was 188 Crore where as CDSL achieved 200 Crore net profit with a topline of 344 Crore.

See NSDL results here.

Very clearly NSDL continues to be more active in terms of actual quality of investors( i mean more active institutional trade desks continue to use NSDL) resulting in better turn over. The profitability is lower on account of employee cost being nearly 20% of top line(compared with 12% in case of CDSL).

AJ

Disclosure: Invested in CDSL.

The pandemic has accelerated the overall market size. Probably years worth of market growth has been achieved in a few months. I have definitely underestimated on that front.

But the crux of my argument still stands. I’ve never said CDSL is a bad investment or anything like that by any stretch of imagination. My argument was that CDSL has little to no requirement for the excess cash they generate from Operations. The best utility, even though it’s the most inefficient option, is to increase Dividend payout as much as possible (Even up to the extent of 90%).

I believe the question of increased Dividends was already raised to the management and they’ve responded in the negative, being more concerned about reducing the ‘Other Income’ (Income from Financial Investments).

In this respect, CAMS is better. They have an explicit policy of paying out at least 65% of Consolidated PAT as dividend - probably the only company where I have seen a specific number. Most other companies have reduced SEBI’s dividend policy mandate to a joke. Last year, CAMS’ dividend exceeded 100% of the profits, resulting in a reduction in Net Worth and boosting the ROE. It is almost an equivalent of a buyback.

Thank you. Was not referring to buy/ sell ….just for your overview and especially the last para “……if your expectation is anything other than a slow consistent grower….” But you have answered my question. The pandemic has certainly changed more than peoples lungs and lives! Thanks again

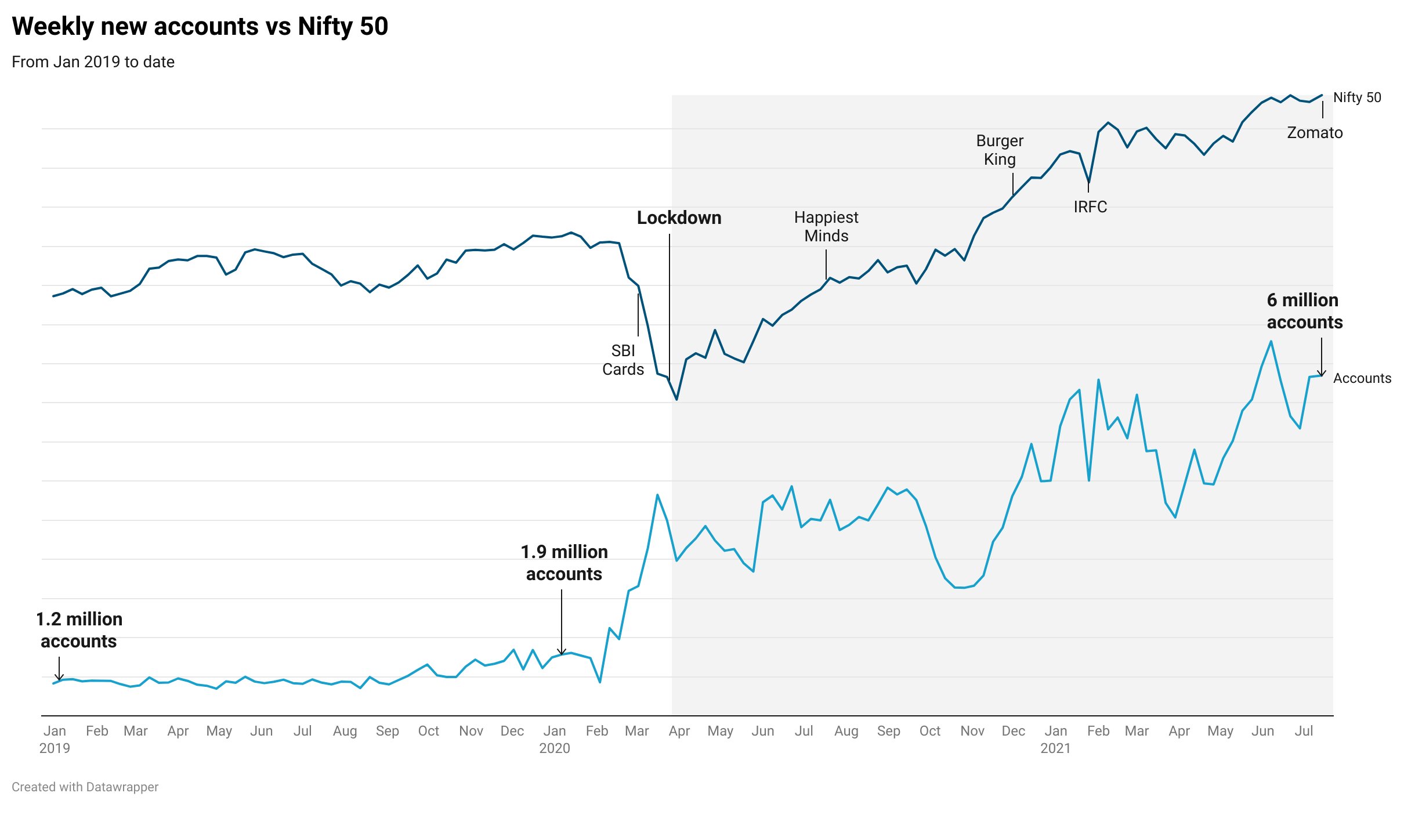

The pandemic and the resultant increase in Trading Activity was unprecedented. I believe even the growth in Zerodha’s accounts was equally stunning. Years’ worth of growth has been achieved in the matter of a few months.

The question is, then, can CDSL continue to grow accounts at historical rates from this large base? The market certainly seems to think so, going by the current Price it is quoting.

Hello sir

i havent really gone through your old posts…and i may not be as informed or have the expertise of your level…

but,the way i see it…

7-8 years from now…CDSL wont just be about Zerodha and demat accounts…CDSL would become a custodian and record keeper of ALL OUR FINANCIAL INSTRUMENTS (be it bonds,shares,mutual funds,insurance policies,loan agreements,guarantees and even title deeds when they r digitised)

and i think…this is the reason the market is giving it such high premium…

Its slowly transforming into a Fintech

I think even by simple calculation if CDSL price per share was quoting 350-400 pre-covid times at a lesser accounts/earnings growth rate than present… now there are 4x more accounts… so 4x into 350 = 1400

One thing I fail to understand why the market is not bothered about the risk due to legislation. If there is a huge growth witnessed and every financial instrument is going to get dematerialised, why would any government restrict only to two depositories? Or allow two depositories to make money. Govt could allow “No Frills” Demat account or might allow only a wafer thin margin for depository service providers. Not sure if I miss any big picture? If these risks are probable, I fail to understand the picture perceived by the market about the prospects of CDSL to provide rich valuations.

two reasons why this risk isnt a big one…

If new depositaries come up…they will take years and years to reach the level of the first 2…and become financially viable

even if 2…3…4 more custodians r made by legislation…even then the pool of profit will be highly

concentrated and the bigger fish will get biggest…because they will eat the food of the other fish too…

" Almost 20% of all zomato applications through zerodhaonline, returning the favour from everyone at Zerodha for all the tasty food Zomato delivered when we were hungry. Wishing you and the team at Zomato a blockbuster listing. " - Nithin Kamath

This tweet is the proof of the growth of discount brokers and thus CDSL. A quick google search reveals that the top brokers with the most active accounts are mostly discount brokers having DP with CDSL. While the valuations might have run ahead of the fundamentals but this is a bull market and almost every stock looks expensive right now.

Already some talks of expanding scope of Digi Locker into newer areas including insurance depository, etc. Could be further expanded. This could be a very potent threat in long run.

Disc: Holding CDSL from lower levels.

There is some invisible entry barrier for getting into depository business. Minimum 100 Cr capital and promoter can hold upto 15% stake. BSE was forced to cut down stake in CDSL few years back.

Anyone knows how CDSL stock being moved to T2T segment by SEBI and circuit lowering to 5%,how much negatively will it impact the stock price in short run ,or any past examples on stocks being moved to t2t segment and what happened thereafter

I don’t think DigiLocker is going to be a big threat. Unless there is a big technical change this market belongs to first movers. The first major customers will bring more customers for network effect. And then switching costs will create a moat.