One of the main difference they didn’t mention is the contribution of NSDL Payments Bank. That’s why the margins are different for NSDL Vs CDSL.

Further most of the full service brokers have tie-up with NSDL and the discount brokers are with CDSL. So the number of demat accounts are high for CDSL. Anyhow as there are only two Depositories.. Both are good proxy to capital markets in India.

3 Likes

i did some research

here’s what i’ve learned:

overview

- nsdl was set up in 1996 as india’s first depository

- cdsl came later in 1999

- today, cdsl dominates the retail segment while ndsl remains strong on the institutional side.

group structure

- nsdl owns ndml (its data management arm) and nsdl payments bank.

- ndml supports ~1,728 sebi-registered intermediaries and managing ~1.9 crore kyc records through its central kyc registry licence.

- meanwhile, nsdl payment bank delivers digital financial products, including prepaid cards, dbt-linked accounts, cash management solutions to corporate and government clients under a b2b2c model.

- 50% of nsdl revenue come from banking service and 43% from depository service

- cdsl owns cvl (for kyc), cirl (for insurance repositories) and ccrl (for commodity repositories).

tech

- nsdl provides portals like IDeAS and Speed-e which are powerful but built for institutional or enterprise users. the ui seems complicated

- cdsl has Easi and Easiest along with integrations into apps, email alerts, sms confirmations, and even services like e-Locker and myCAS which are extremely popular among retail users.

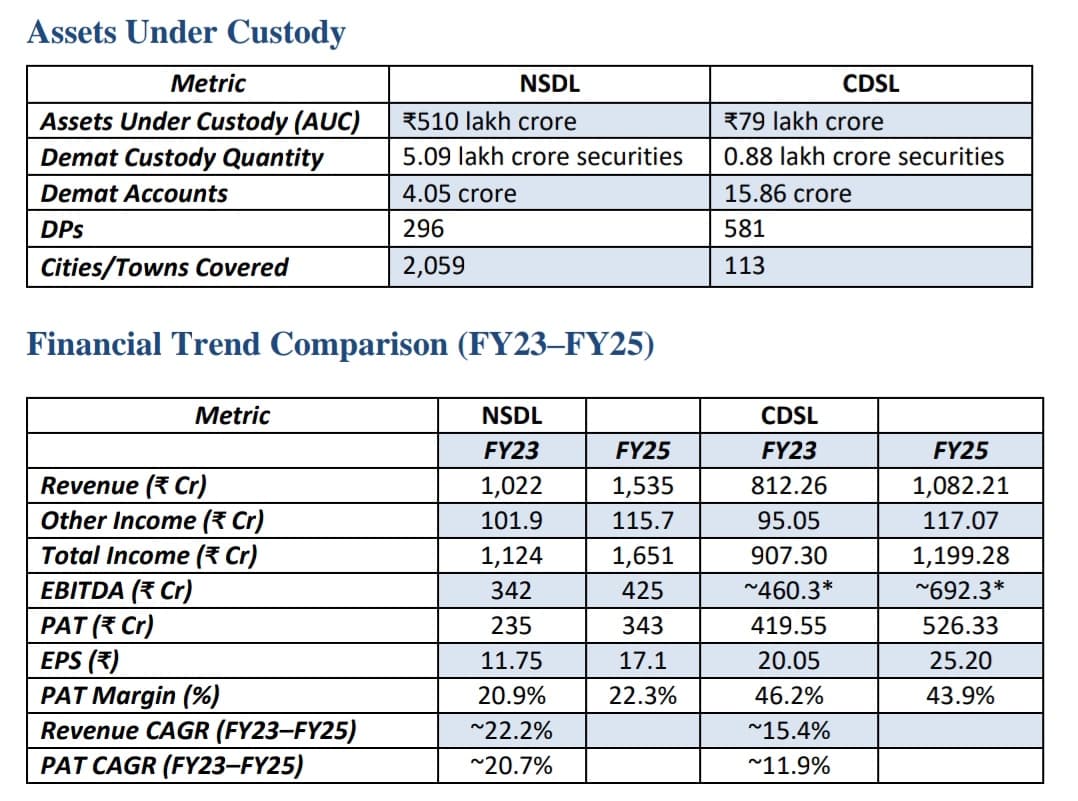

assets under custody and financials

assets under custody

- nsdl manages ₹510 Lakh cr auc (6.5× cdsl). that’s expected because nsdl focuses on big institutional clients (mutual funds, insurers, etc.).

- nsdl also holds 5.09 lakh crore securities vs cdsl’s 0.88 lakh crore.

- cdsl, however, dominates in number of demat accounts: 15.86 crore vs nsdl’s 4.05 crore.

- cdsl has more dps - 581 vs nsdl’s 296

financials (fy23–25)

- nsdl’s revenue grew over 50% in two years while cdsl saw around 30% growth in the same period.

- cdsl still earns higher margins with pat margins consistently over 40%, while nsdl stays around half that.

- nsdl’s profit grew over 45% but cdsl still earns way more profit at every level

- ebitda for cdsl grew faster and is higher than nsdl

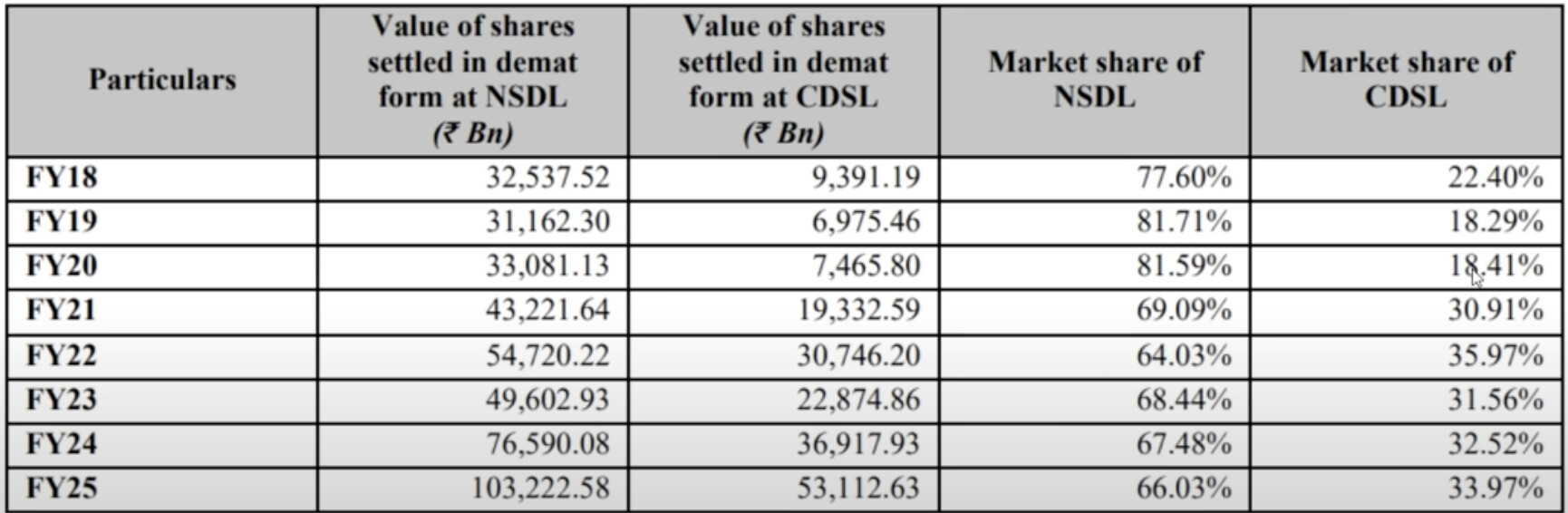

market share

- cdsl has been steadily gaining market share over the last five years. in fy20, it had just ~18% share, but by fy25, that’s grown to nearly 34%.

- meanwhile, nsdl’s share has dropped from ~82% to 66% in the same period.

core segments of cdsl and nsdl

core segments of cdsl

- depository activity (~78% of operating revenue)

- transaction charges, annual issuer fees, cas/statement income, e‑voting, corporate action charges, ipo data fees.

- data entry & storage (~21%)

- mostly kyc/kra, e‑kyc, aadhaar/ckyc validation, e‑insurance data handling through cdsl ventures ltd (cvl) and related units.

- repository (~0.2%)

- commodity & insurance repositories (ccrl, cirl). tiny and generally loss-making.

core segments of nsdl

- banking services via nsdl payments bank (≈51% of operating revenue)

- digital banking, micro-atms, remittances, mf distribution.

- depository services (≈44%)

- transaction fees, custody/annual issuer fees, registration & communication fees.

- it/database & other services (≈5%)

- kra/e‑kyc, e‑voting, national academic depository, national insurance repository, otm mandates largely through ndml

growth drivers and risks

- both benefit from rising capital market participation, fintech expansion, and overall digitization of savings.

- risks include market volatility (since a lot of their revenue is transaction-based), regulatory caps on fees, and any tech infra failures. since both are miis, sebi keeps close oversight

management / team

- nsdl is led by vijay chandok, former md & ceo of icici securities. he joined in 2023.

- cdsl’s md & ceo is nehal vora, reappointed in 2024. he was earlier chief regulatory officer at bse.

tldr;

- cdsl has grown faster, is more profitable, and has built a strong retail moat. it runs at higher margins but is also expensive (trading at ~67x pe)

- nsdl is more institution-driven and integrated into india’s financial system through mandates and corporate actions. it has larger assets under custody but operates less efficiently. ipo price at ₹750 implies ~44x pe.

will add more later; feel free to add if i missed anything

14 Likes

A detailed explanion with good comparison points with CDSL and Fino payments bank are given below, Eventhough content language is regional, you can get a better comparision for valuation metrics in the following

2 Likes

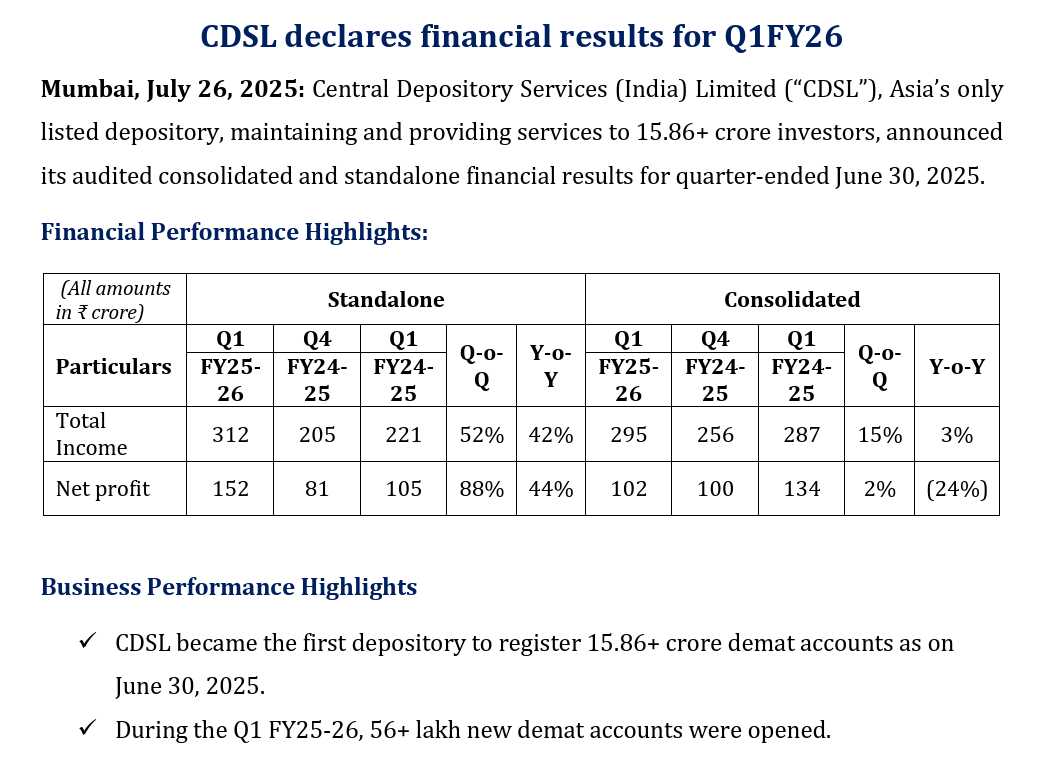

bad result from cdsl

net profit down 23.6% yoy

revenue up 0.6% yoy

ebitda down 15.1% yoy

margin at 50.44% vs 60% yoy

https://nsearchives.nseindia.com/corporate/CDSL_26072025134453_FinalOutcomeBM26072025.pdf

1 Like

Why is there a sudden increase in annual issuer income? Is it from one time fee charged to unlisted cos?

as mentioned in note 3, other income includes dividend income received from a subsidiary amounting to ₹62 crore

1 Like

While the result seems bad because pf pat drop, it’s still good considering cdsl had a transaction charge drop to 3.5 from around 5 also the infra costs it expenses were called out before management, the result looks bad because of it’s higher PE now but still market activity is doing considering revs were stable after drop as well

3 Likes

recent shareholding as of 30th sept shows public shareholding has reached an all time high which makes me slightly concerned. (disc : heavily invested)

4 Likes

CDSL Q2 FY26 Results

• Revenue: ₹319 Cr (↑23% QoQ, ↓1% YoY)

• EBITDA: ₹180 Cr (↑36% QoQ, ↓11% YoY)

• EBITDA Margin: 56.36% vs 51.2% (QoQ), 62.7% (YoY)

• Net Profit: ₹139.9 Cr (↑37% QoQ, ↓13% YoY)

Numbers in Line as Expected YoY were expected to decline due to Dull Markets. Strong QoQ Performance

7 Likes