Why is LIC signing with both the repositories? Is this a regulatory need?

What determines which repository is used for a policy? This should not be a choice for the policy holder as it will lead to more confusion.

1 Like

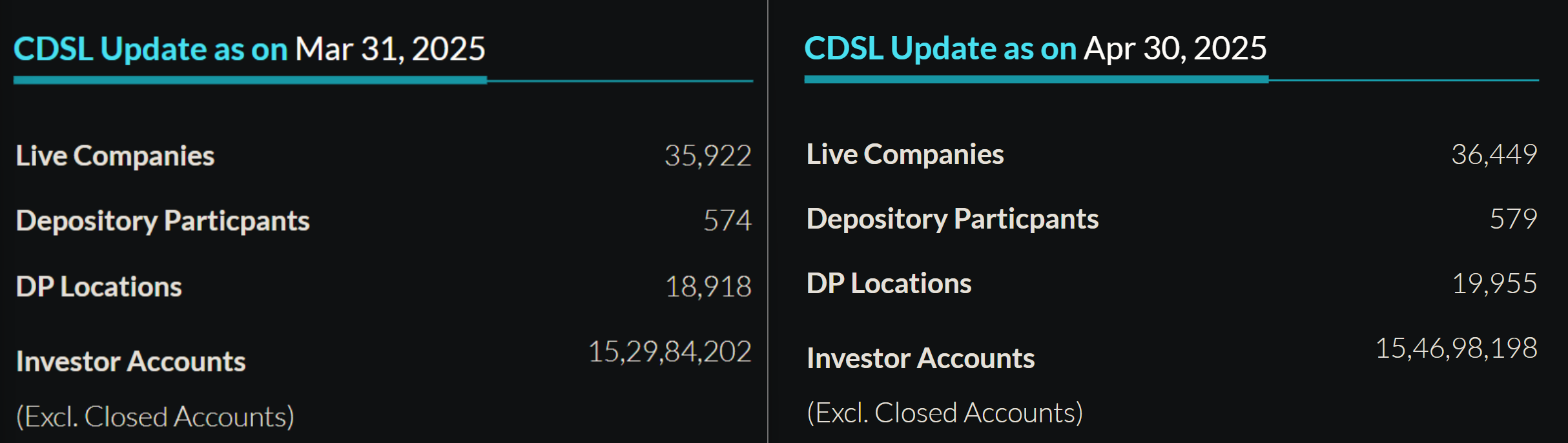

1.15% month on month growth in investor accounts. Other numbers also rised except for Depository participants.

4 Likes

Due to the ongoing bearish phase (or so-called), new account openings are taking a hit. In bull markets, capital market stocks usually grab more attention. IPO market is also out of action.

3 Likes

pretty bad results..although qoq degrowth was expected and perhaps priced in, yoy degrowth might not have been priced in

3 Likes

I think these kinds of results are expected, considering the type of market we faced in Q4. Comparing the results year-on-year or quarter-on-quarter may not be appropriate, as both of those quarters were in a relatively bullish phase, whereas Q4 was more of a bearish phase for the markets. We can mostly expect some recovery in Q1.

1 Like

If not QoQ or YoY, then to what exactly do we compare the results to? The share price is bound to correct by another 15-20% and one must be able to accumulate it between 1050-1100. Again, this is just my personal opinion!

Capital market stocks—such as AMCs (like UTI AMC, HDFC AMC), wealth management firms (like Nuvama, 360 One, Motilal), depository-related companies (CDSL, Angel One), intermediaries (like KFintech), and others (like DAM Capital)—are heavily dependent on bullish market conditions. For a deeper comparison, one should look at how these stocks perform during bearish or choppy market phases. We’ve already seen a hit in the results of Motilal, Angel One, and KFintech, and even CDSL hasn’t remained unaffected. Still, we should wait to see how the market reacts going forward

4 Likes

One of the things that I haven’t checked out statistically, how well do NBFCs do during bad times; they lend at higher rates and if they lend at prudent rates to good companies, their returns are generally higher, if they keep their NPAs under 3%. Point being is to switch to pure NBFCs from these. of course the risk is correlated and they both can go down

1 Like

Market does not react in May for something that happened in March. Market is forward looking. When it had reached less than 1100 at that time you should have taken a position in anticipation of eventual market recovery.

Disclosure : Among my top exposures.

4 Likes

Superb Yields in SLB - Probably Very high short positions leading to futures in discounts.

These yields and discounts were much higher last week (pre-earnings)

(PS- Have Lent mine)

Can you elaborate what is SLB? I also saw discounted futures since months but didn’t understand why. How is SLB related to discounted price in futures?

1 Like

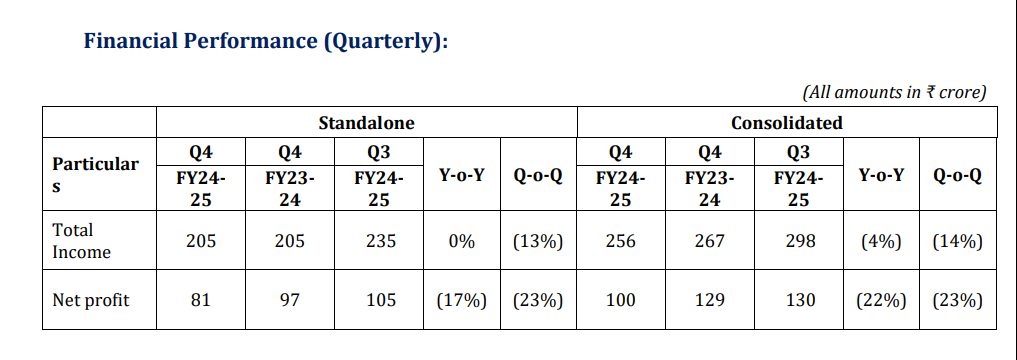

Highlights from Q4 FY25 earnings call

Financial performance (consolidated)

FY25 performance:

CDSL closed the year with revenue of ₹1,199 crore (up 32% YoY) and profit of ₹526 crore (up 25%)

Q4 result:

Total income was ₹256 crores compared to ₹267 crores in Q4 FY24. Net profit at ₹100 crores versus ₹129 crores in the same quarter last year. Q4 revenue and profit were down YoY due to lower market activity, IPO slowdown, and fewer account openings. Transaction income and KYC-related revenue also saw some pressure.

Tech:

They rolled out unified features in the MyEasi app and integrated e-cas (electronic consolidated account statement) across platforms

There were a lot of questions on tech costs. Management said infra upgrades are ongoing (infra, security, app layer), and they treat modernization as a continuous process not a one-time thing. they didn’t break down how much is recurring vs. one-time.

KYC business:

Some uncertainty around the future of KRA systems with SEBI pushing centralized KYC. Management’s watching how that plays out. For now, KYC income is mostly driven by DMAT-related activities.

Subsidiaries update:

CVL (CDSL’s KYC arm) saw income up 35% yoy and profit up 28% yoy. Insurance repository is still early stage. LIC integration is in progress. They said it’s underpenetrated vs peers and said a lot of infra groundwork is being laid.

Demat accounts:

India added 4.1 Cr new demat accounts this year. Total now at 19.24 Cr in India, of which CDSL holds a massive 79% share (15.29 Cr).

Some other points:

- CDSL is active as an FIP (Financial Info Provider). Still early stage, no major revenue yet.

- Revenue from unlisted companies was around INR 36 crores for FY25. they earn one-time processing fees of ₹15,000 per company.

- some shareholder concerned on cash usage, margins, and infra costs came up. Mgmt responded saying the long-term view remains strong

- Demat accounts have grown 8x in 5 years (from 1.8 Cr to 15.5 Cr)

- Employee count and brand value have scaled meaningfully

- They want to build infra for “Viksit Bharat”

- No specific guidance, but management seems confident

Feel free to add if i missed anything

D: Invested

8 Likes

Hmm, there’s a couple of threads on VP.

But essentially markets Probably expecting bad results/ underperformance in the near run due to lower capital activity.

They Probably shorted so many lots that - E.g from the Screenshot- JULY delivery is 45 bucks cheaper. (99% of the times futures are at a premium)

So a long term investor(bull) can lend it for 35 bucks.

The Arbitrager will pay you T+1 35 bucks - Then he will sell the shares in cash and buy in futures.

He will return the shares after taking delivery of the futures in July.

In this case his profit is 10 bucks MINUS expenses.

You gain is 35 bucks. (Exchange guaranteed for counterparty Risk)

Hope useful ![]()

3 Likes

Thanks for trying to explain. If you have links to any resources to understand it better, do share! I would love to understand more.

Current valuations appear stretched & recent quarterly performance indicates potential short term challenges attributed to decreased transaction volumes and fewer demat account openings.

6 Likes

Basic flaw in the video, Ishmeet said that the bottom P/E of 20 is no longer valid considering new avenues of business being introduced. He suggested bottom P/E could be considered 30-35, but he did not factor this in while discussing avg. P/E of 40.

I believe there is limited downside to the stock and potential to make new ATH soon.

@praveenks74 Previous tow quarters were bad for overall markets and CDSL’s revenue is linked to ADTO and IPO activities. I expect recovery starting Jun quareter and major bounce back in 6-12 months time. Considering that I am bullish on overall market (expect choppiness but overall should trend up) and upcoming IPOs.

I am positively biased considering I have holdings in CDSL. Views are not Buy/Sell recommendation.

5 Likes

NSDL IPO Next Week

CDSL has a Bigger Market Share, but NSDL has better transaction income

Please share your Views on the rival of CDSL?

2 Likes

1 Like