Increased competition for CCL from Vietnam biggest player.

2 Likes

Smallcap World Fund Inc Sold 65,12,851 Shares

its total Holding was 10,580,884 Shares 7.95% before the deal happened.

GM’s seem to be improving due to commissioning of freeze dried which is higher margin. Going forward, margins might potentially further improve due to commencement of packaging unit. Which they can use to sell smaller packets which have higher margin when compared with bulk selling. Moreover, they might all together cut out the middle guy. Let’s see how it pans out

Disclosure

Invested

3 Likes

Concall highlights

Investor Conference Call Highlights

- The margins for the company are expected to stay stable at current levels mainly due to the shift of the product mix towards freeze-dried coffee.

- The management has mentioned that the company is operating at optimal capacity in the Vietnam facility and the company is looking to expand capacity in this unit. This is because the current product mix has caused output volumes from this unit to decline and thus the company feels the need to expand capacity to address growing demand in a timely manner.

- The volumes for the quarter were according to the company’s estimates.

- The company is going to invest $8 million for expansion in the Vietnam plant to increase capacity by 3500 tons. This expansion is expected to be done by Q1FY21. The company expects the capacity utilization in the expanded capacity in FY21 to be around 75%.

- In the domestic business, the company expects sales of Rs 100 Cr in FY20 and more than half of this is expected from the branded business. Last year the branded sales were only Rs 30 Cr vs Rs 50 Cr expected this year.

- The company spent around Rs 14-15 Cr for business expansion and marketing and the company expects to maintain this proportion going forward.

- The management has stated that the company is expecting to earn around $14 million in revenues from the proposed expansion as full capacity.

- The management admits that the YoY growth in Q3 was mainly due to lower base in Q3FY19 and QoQ growth has been normal. The realization has been higher mainly due to freeze-dried capacity working at optimal utilization.

- The Vietnam business has become EBITDA breakeven in Q3 and is expected to turn profitable in Q4.

- The company has realized the Merchandise Export from India Scheme (MEIS) of Rs 30 Cr in the year so far.

- In India operations, the company expects capacity utilization of around 80-85% in the next year. The company is also planning an activity which can increase capacity by 500 tons.

- Gross margins are expected to stay stable at current elevated levels as it has been achieved as a result of the company’s upgradation efforts and other initiatives like the improved product mix.

- The CAPEX for this year and next year in total is around $23 million which includes the $8 million expansion in Vietnam.

- The rise of coffee prices does not affect the company’s sales immediately and since the company uses 6 months or one-year contracts, the impact appears sometime in the future.

- The working capital cycle for the company has increased mainly because of enhanced operations in Switzerland unit.

- The inventory days is at 60 days and receivables are at 75 days with no change in payables.

- The new small pack making facility is expected to be completed by end of FY20 and operations should start from FY21 onwards.

- The Indian subsidiary is expected to breakeven next year as this year, the subsidiary has some small losses due to high marketing costs.

- The company is the 3rd largest brand by market share after Nescafe and Bru. The company already enjoys >5% market share in major cities in South India like Hyderabad.

- The utilization level in Q3 is around 75% in the SEZ facility. Overall on a yearly basis, utilization was between 50-60%.

- The company has gained a new customer from whom the company is expecting some large orders to come in for the Vietnam plant.

- The company is seeing growth in market demand for freeze-dried coffee and thus it has already planned its expansions accordingly.

- The company is consciously focussing on growing its branded business.

- The market size of instant coffee in India is around Rs 2000 Cr and the filter coffee market size is around Rs 400-500 Cr. The company aims to reach 5% market share or Rs 100 Cr in branded sales in the next 2 years.

- The management has chosen to focus on branded sales with freeze-dried coffee as the major players like Nescafe and Bru do not have facilities in the country to make this product and importing it from overseas facilities will raise costs to unsustainable levels for these players. Thus CCL has a unique advantage in the freeze-dried coffee space which the company hopes to use to capture the market from the incumbent players.

- Regarding the company’s unique and premium products like cold brew coffee, the company is introducing it to developed markets because of higher acceptance of such products. At the moment the company’s products are unique and not manufactured at such scale anywhere in the world and the company hopes to capitalize on this first-mover advantage as much as possible.

- The company is now targeting customers with higher quality requirements to remove its dependence on price-sensitive customers.

- Around 60% of customers are ones that are quality customers who get unique offerings from the company while 40% are vanilla customers with whom the company does not have any competitive hold other than price.

- The expenses for the branded business that has been booked by the parent company is around Rs 10 Cr.

- The management has said that from next year onwards, the company will also be looking to use some of its cash flows to pay back term loans in a timely manner.

- The Switzerland business has been doing well and is generating deals with major supermarket chains in the EU region. The revenues from this unit is Rs 83 Cr in 9M period and the company expects this to reach Rs 110 Cr by the end of the year.

- The company has around 60,000 retail outlets in reach and around 600 distributors for the branded business currently.

- The company is looking to balance the low margin bulk business and the high margin premium business and not reduce dependence on its traditional strengths in the bulk segment to chase premium growth.

- The management has said that the govt is likely to incentivize industries to promote exports even if MEIS regimen comes to an end. Thus some form of export incentive is expected to stay preserved for exporting companies like CCL.

- The company is still sticking to its earlier guidance of 10-15% volumes growth for FY20.

17 Likes

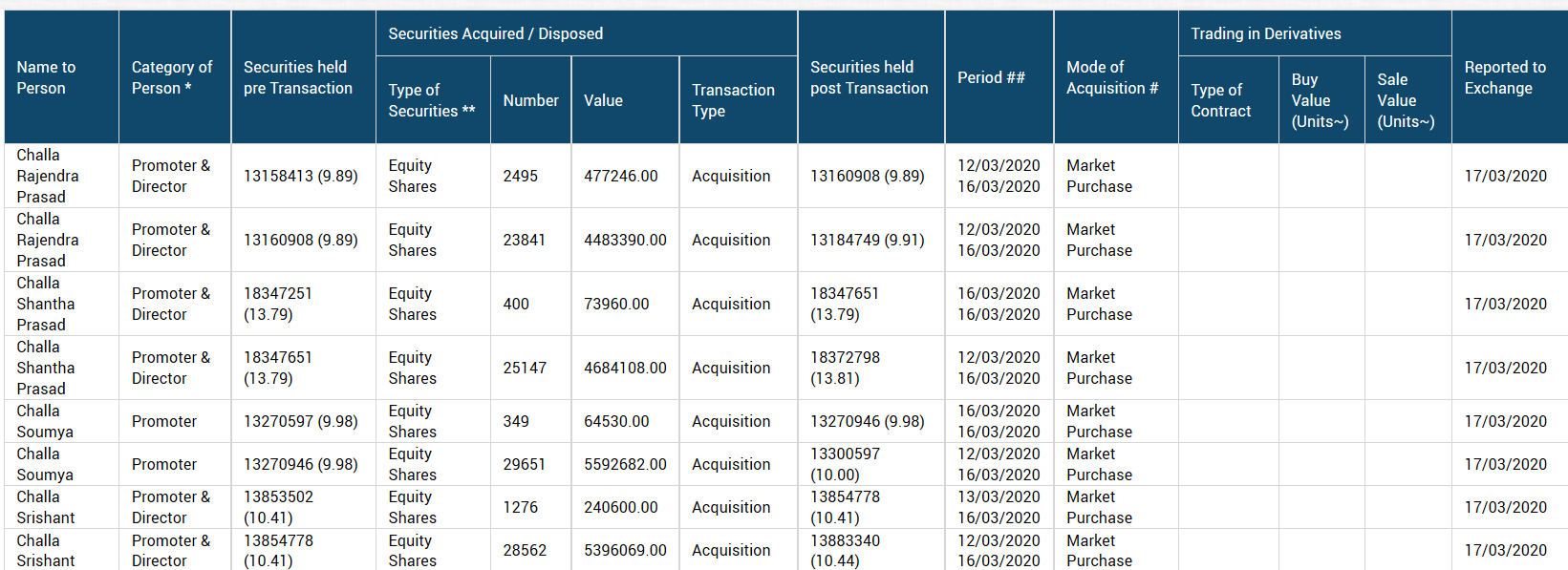

Promoter group again bought ~50,000+ shares from open market on 30-31 January as per latest SAST disclosures.

5 Likes

The promoter’s buying is continuing as per market disclosures.

Source: Insider trading data on bseindia.

Disclosure: Not invested, on the watchlist.

3 Likes

Does anyone have clarity on how the brands are doing in India now? Are they likely to cross 100 cr mark ?

They are doing good and growing steadily. Their branded sales is still much less than 100 cr (see above).

It takes at least 3-5 years in my view to build a strong brand in such space, particularly when you have strong competitors.

Consider this more like an optionality.

7 Likes

“CCL Products (CCL) is the newest entry into our portfolio but has been in the coffee business

since 1994. Today it is the world’s largest private label instant coffee manufacturer with operations

spread across India, Vietnam and Switzerland. CCL’s strength is its growing customer base which

is both dispersed (across 90 countries) and sticky (selling over 200 unique blends). More recently,

the company has also launched its own brand `Continental Coffee’ in India to take on the market

leader Nestlé. Three competitive advantages – a) low cost manufacturing with economies of scale,

b) strong reputation in the market with consistency in quality and long term client relationships

c) technical know-how to produce high-quality instant coffee using all grades of raw coffee beans.

CCL’s earnings have compounded 19% CAGR over the last five years and demand for its products

remain strong (including during COVID-19). We expect the company to grow its earnings at 15%+

CAGR over the next three years driven by both volume growth and increased profitability (mix

and productivity). Success in its domestic branded market play could lead to a further rerating of

the business.”

10 Likes

CCL Products Q4FY20 Results

-

Total income improved from 262 crores to 267 crores YOY (Need to check volume growth thought)

-

Total expenses fell YOY from 215 crores to 210 crores.

-

PBT increased from 47.48 crores to 57.67 crores i.e.an increase of 21% YOY

-

PAT increased from 35.63 crores cr to 42.19 crores i.e. an increase of 18.6% YOY.

-

Most importantly the Operating margins of the company improved from 21% to 27% YOY.

Balance sheet update

-

Property,plant, and equipment increased from 383 crores to 723 crores due to capitalization of fixed assets. New capex for Freeze Dried coffee came on stream.

-

There’s still an amount of 100 crores that is there in CWIP, which has reduced from 424 crores to 100 crores.

-

Inventories went up from 200 crores to 260 crores YOY.

-

Trade receivable increased from 235 crores to 266 crores.

-

Long term borrowings saw an increase from 192 crores to 249 crores.

-

Short term borrowings fell from 183 crores to 142.7 crores.

-

D/E was at 0.42 when compared to last years 0.45

Cash Flow Statement Updates

-

Net cash generated from operating activities fell YOY from 161 crores to 90 crores.

-

As there were adverse changes in inventories and Trade receivables due to COVID 19 impact (mentioned in footnotes) and Management trying to win business in US, they had too loosen the credit terms a bit.

-

Cash and cash equivalents fell YOY from 72.66 crores to 37.65 crores.

Dislosure- invested and biased, seeing positive sign of thesis in margin improvement due to product mix changing towards the higher-margin Freeze-dried coffee playing out

8 Likes

CCL products concall Q4FY20

Business

-

Full year topline was at 1143 crores compared to 1084 crores. Profits grew YOY from 155crore to 166 crore. Ebitda was at 290 crores.

-

Chittoor Unit(new higher margin capacity), Capacity utilisation was close to 50% majorly in Q3 and Q4.

-

Gross margins improved to 60% majorly due to improve in product mix as higher margin capacity came into picture.

-

Built up inventory due to Covid disruptions have been cleared off in Q1FY21.

-

Retail demand for coffee has gone up, though offices and institutions demand has come down. Don’t know when the institutional demand will normalize.

-

Capacity Break up: 25,000 Mt in India

10,000 Mt in Vietnam -

Capex break up : Packaging capacity capex of 120 crores to kick in Q1FY22 and 3500 MT expansion in Vietnam, capex in Vietnam to be at $ 8million. Vietnam capex to come on stream in Q3FY21.

-

Gross Margins at highest in operating history. Expect it to sustain.

-

Capacity utilisation breakup

India:80-85%(excluding new plant), Vietnam: 65-70%

- Geographical Breakup

Switzerland plant, 135 crore sales and 3.7crore profit.

Vietnam plant, 268 crore sales and 56 crore profit. Rest from Indian plant.

-

In B2B business, sell 50% to brand owners directly and 50% to repackagers/Bulk buyers. Doing a capex for small packaging as even brand owners are asking for it. Took inputs from brand owners for plant designing.

-

Key positive after 4-5 years of patient engagement with the Us customer, have finally procured orders for the whole year which will commence from Q1FY21. Have procured orders for bulk+ first time for us in small packaging . Order quantum is 4500-5000 MT.

-

Debt repayment of 76 cr per year and full debt to be repaid by FY23-FY24.

B2C business

-

Indian business at 90 crore revenue and 3 crore loss. 60% is branded business and rest is private labels/bulk. Experienced 40% growth in the domestic business.

-

Focused more on South Indian market. Have close to 4-5% market share in Indian instant coffee market.

-

Really happy with the team in Domestic business and B2C performance. Creating a new market from scratch by launching various new products.

-

Branded coffee market size in India is only at 2000 crores, it is very consolidated between HUL and Nestle. Foreign players are not interested due to this small size.

-

Distribution reach of 55-60 k retailers in South India. Potential is of 8-9 lakh retailers in South India. 6-7% of sales are online sales.

Management

-

Expect 10-15% Ebitda growth this year.

-

Strategy of differentiation in our domestic coffee business. As soon as we strengthen south Indian market share, we have the system in place to target other metro cities. Trying to build a different coffee culture, will be selling Premium coffee at lesser prices to get people hooked.

-

Give out close to 1 Lakh cups for sampling.

Risk

-

Coronavirus cases close to factory everyday.

-

Lost entire production month in April and operated at 33% utilisation in March in India. No difficulties in Vietnam.

-

Built up inventory in March has been cleared off. Inventory got accumulated due to lack of logistics available to transport.

-

Meis (export incentive) reduced from 7% to 5% YOY. Likely to see an impact. In my view Meis might get removed eventually.

My opinion- invested and biased, solid margin expansion in the current environment. Mostly a recession proof business. But, yes volume growth will be likely between 8-12%. Margin expansion thesis is on track. Us customer win is a big postive as Us is one of the largest coffee market in the world.

19 Likes

Given the reduction in Export incentives over time, do you think there is scope for margins improvement even after considering the effect of it?

The more I dig into this company ( nd I’m still digging), wat I find is that this less of a MOAT case and more of a MANAGEMENT execution play. Below are the reasons for the same : -

-

The entry barriers to competition are low. Coffee processing techniques are same - Freeze dried and Spray dried; the equipment\processes are standardized and a period of stable to rising commodity prices enables capacities to come up. This, as accepted by the management, has been the case over last few years.

-

Revenues or revenue growth per se is again dependent on Coffee prices with a lag. And being a commodity, Coffee prices are bound to be cyclical. So, the focus is more on EBITDA growth than Revenue growth. This is where scale and cost savings gives the company an edge.

-

Coming to Branded play - Again, as per the company, in most of the countries, instant coffee or coffee drinking market is highly competitive with lots of regional\national competitors. In fact, this was the reason for company’s B2B diversified customer base. If Indian coffee market is to grow like-wise, then its safe to assume that here too competition will prevail on similar lines.

Case in point above if the filter coffee drinking south Indian market :- We’ve got lots of local filter coffee brands there e.g Narusu, Bayar’s etc.

Taking the above points into consideration, the management has done very well by investing in initiatives like Brand Building, Agglomeration unit, moving away from bulk orders etc. and it will aid EBITDA margin to some extent. But end of the day, sustained scope of revenue growth is what drives up the value over long term. And in absence of high barriers to entry, any margin expansion will be eaten up by competition sooner or later.

Wat say??

Disc : Not invested. Analysis in progress

4 Likes

If its a commodity play as you have laid out , management doing a commendable job of maintaining margins and more or less consistent growth

Agreed. The management has done a good job owing to their industry expertise and smart focus. But the above analysis and their resultant conclusions serve as a guide to 2 critical variables for evaluating this investment : -

- The long-term sustainable EBITDA margins that the company will attain

- The valuation multiple you will give to the business, now considering that more than structural advantages, it depends upon the moves the management makes

annual report

1 Like

CCL Products AR 2020 Notes

Company did good on the margin front this year. They have completed a major capex during the year and it would be interest to see the kind of Fixed Asset Turnover they get from it, in the past 5 years they had an average FA turns of 2.64 times but they did not commercialise any major capex during this time.

- During the year, the SEZ unit of the Company situated at Kuvvakolli Village, Chittoor District in Andhra Pradesh has commenced its commercial operations.

- Continental Coffee Private Limited promoting instant coffee brands of the Company in the domestic market made sales of Rs. 77 cr in FY20 against Rs. 47 cr in FY19 and Loss of Rs. 3.49 cr in FY20 against Loss of Rs. 6.10 cr in FY19.

- Ngon Coffee Company Limited is a wholly owned subsidiary of the Company incorporated in Vietnam. This is an instant coffee manufacturing unit. Sales of Rs. 267 cr in FY20 against Rs. 261 cr in FY19 and PAT of Rs. 57.79 cr in FY20 against Rs. 66.20 cr in FY19.

- Domestic Market

- Continental Coffee Private Limited promoting instant coffee brands of the Company in the domestic market made sales of Rs. 77 cr in FY20 against Rs. 47 cr in FY19 and Loss of Rs. 3.49 cr in FY20 against Loss of Rs. 6.10 cr in FY19.

- CCL created a dedicated team exclusively for domestic market, drawing professionals from FMCG companies for this brand creation. Over a two year effort, we are identified as third largest domestic brand coffee in South India for the year 2019-20.

- Company had launched 3-in-1 premixes in various flavours like Hazelnut, Cappuccino, Mocha, Caramel etc., under the brand name THIS, mainly providing younger generation with an option of hot beverage of their palate.

- Also your Company launched premium Freeze Dried coffee in different flavours like Coconut, Spice, Lemon and Hazelnut etc., to give a varied option for the customers in the premium segment.

- Continental Decaf was also launched under speciality coffees to cater to the niche market segment that prefers decaffeinated coffee.

- The current instant coffee market in India is growing at a guestimate rate of 8% year on year.

- In light of the current pandemic situation, people have become more health conscious and tending towards value added products in health segment. Your Company’s R&D team is working on developing new products, focussing on the wellness category to catch up the upcoming trend.

- Company is able to enhance its presence in the in-house brands of supermarkets in Europe and impressed by the quality of products, greater levels of service etc., these supermarkets have been consistently increasing our share of volumes. Your company is also confident that it will achieve the orders of various other supermarkets as well in this year. Necessary capacity augmentation is being done during this year to meet this additional demand.

- The major threat being faced by the instant coffee industry is the creation of huge additional capacities in several countries which is resulting in unhealthy competition and stress on prices. Your Company is making efforts to mitigate these threats by increased volumes of high quality niche and new products.

- Covid Impact

- Dispatches were affected due to restriction on movement of finished product to the ports for exports towards the end of the financial year.

- On the demand side, we are visualizing that there is a substantial reduction in institutional requirements (particularly those serving HORECA segment) in view of the lockdowns. However, majority of this is being compensated by the increase in the in-house consumptions.

- The impact of covid-19 is less in Vietnam and this is helping your Company to supply to new markets from the Vietnam Plant.

- The covid-19 pandemic unveiled the opportunity in premix and functional coffee segments due to increase in in-house consumption of speciality coffees.

- Pandemic is likely to have a profound impact on the global coffee sector, including production, consumption and international trade. A one percentage point drop in GDP growth is associated with a reduction in the growth of global demand for coffee of 0.95 percentage points or 1.6 million 60-kg bags.

- There were 617 permanent employees on the rolls of Company as on March 31, 2020.

- In the financial year, there was an increase of 6.45% in the managerial remuneration.

- Cashflows from operations were lower during the year due to extended Working Capital Days from 128 to 161 days yoy. Debt as on march 2020 Rs. 441 cr.

- Company has best operating margins of 25% in the past 10 years which were led by increase in Gross Profit margins from 44% to 51% yoy.

Regards

Harshit Goel

16 Likes

Does anyone have a breakdown of the domestic business (branded, bulk, etc.) for the last 3-4 years? I tried going through the transcripts but my numbers don’t quite add up on considering the % growth that management has stated? Feels like they haven’t been able to catch up with the guidance for the recent past.

Thanks!