Does that mean that green beans available at all seasons to order green beans based on demand?As far as I know, usually coffee beans is a single season product with harvest season around January to March in Southern India

CCL works on a cost plus model. So there is no effect on margins (evident from stable gross margins).

But, if coffee prices are higher, then on absolute terms, CCL does makes more money; coz 10% of Rs100 is different from 10% of Rs110 right.

So, my understanding is that they have a % markup and thus if coffee prices are high, they make more on absolute terms and vice-versa.

1 Like

can you please share source of the information % based margin , asking to make sure whether it is % based or Fixed on Rs per KG based .

“Your Company has adopted a business model, wherein the fluctuating prices of green coffee have minimum impact on the sales of your Company. This has been achieved by your Company entering into fixed contracts with customers taking the prevailing green coffee prices at the time of entering into the contract.” This is given in Annual report 2010 on page 16 under heading “Opportunities and Threats”

It’s not stated anywhere; but since the Gross Margins are relatively constant over the years, it has to a % markup.

1 Like

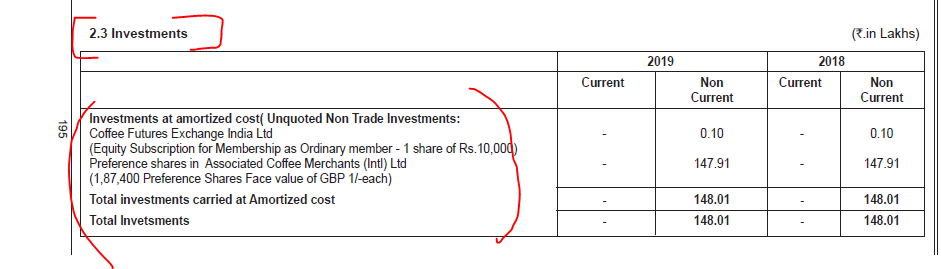

CCL Products had purchased in 2003 a 49 stake in Associated Coffee Merchants (International) Limited which is one of the oldest coffee trading companies in the UK. An extract from the annual report in 2003 is shown below

In the 2019 Annual Report we can see this under non current investments as seen in the extract below

Since coffee is a traded commodity this must have been acquired to fix pricing for coffee when the company gets a contract for supply. The trade payables on an average have been lower than 5% so I feel the coffee must not be coming directly from the farmers but somewhat though this trading entity which they have a stake in.

1 Like

Its a long term investment so it should be carrying on cost . Why investment value decreased from 4.81 cr to 1.48 cr , have they written off part of it ?

1 Like

The gross margins is marked up on per kg basis. However, it needs to be noted that they sell some coffee (10-20%) in spot market. Here is where margins shrink when there is an event like bumper crop production in Brazil.

Also, it seems that on a larger base, they are struggling to grow volumes by 15%. Global instant coffee market may be growing by only 5%. On a larger base, its a struggle to gain market share IMO.

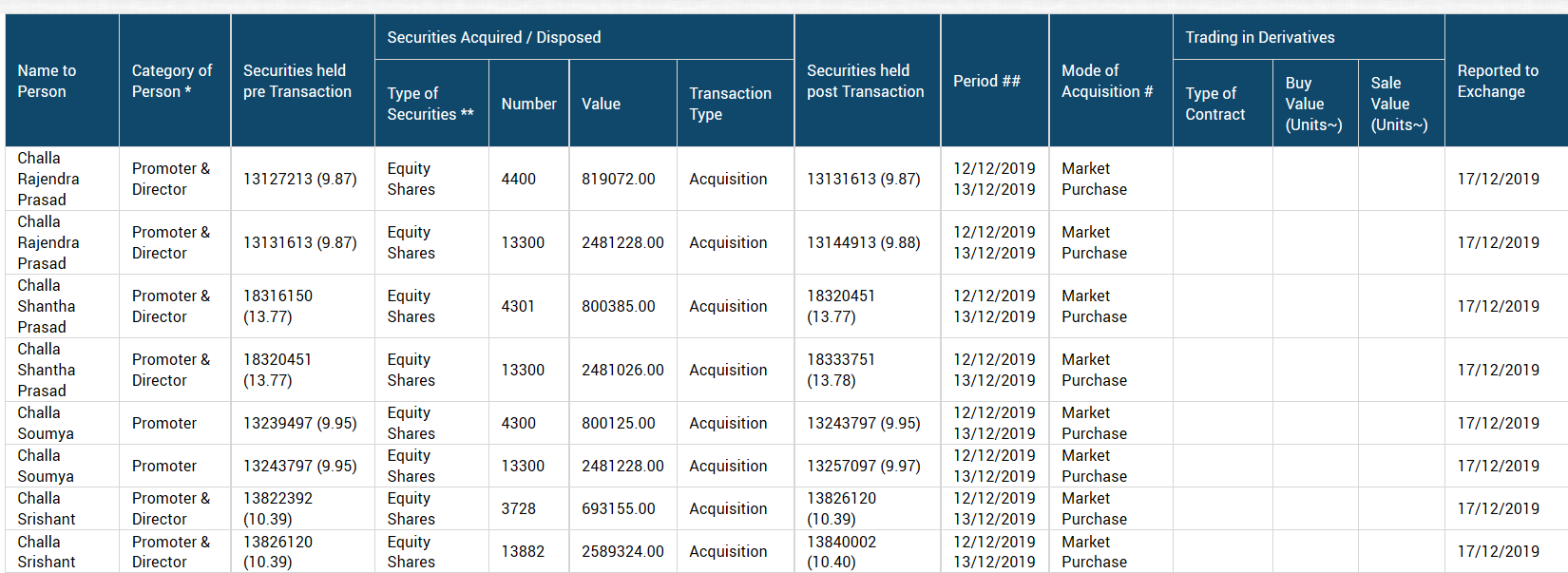

Hi Vivek, very useful. Can you please tell me which website you are sourcing this info from? I checked bulk deals and corp actions on BSE but couldn’t find anything.

It’s from BSE - Insider Trading disclosures. Thx

1 Like

@ankush12495 I remember the CEO mentioning in one of the con calls that whenever the coffee price is lower, their turnover may be lower but the margin will be more because they work on a fixed margin. This means that the margin is not linked to the coffee price.

Dis - I have been investing in this company at different price points in the past one year. The promoters have also been buying.

1 Like

Another risk might materialize

4 Likes

I if understood it correct , 8 crores to 40 crores -ve impact on bottom line ?

Potentially. Market cap might go down by 10-20%, if I multiply 40 cr by the current pe multiple (purely speculative though)

1 Like

Ok the MEIS or duty credit scrips are worth 51.1 cores as on FY19. CCL reports this under income from operation and as it doesnot inccur additional cost, it adds directly to pretax profits.If it goes off in all( worst case), then the impact on PAT would be 40 crore appox. And if we assume the present valuations being fair, it would knock 25% marktcap.

Also in any case to calculate core business margins such incentives shall be taken off to see actual sales and margins, which investors don’t do. It then creates mirage, like the increase in PAT over last few years is mostly due to DCS/ MEIS income.

Happy investing.

Regards !

6 Likes

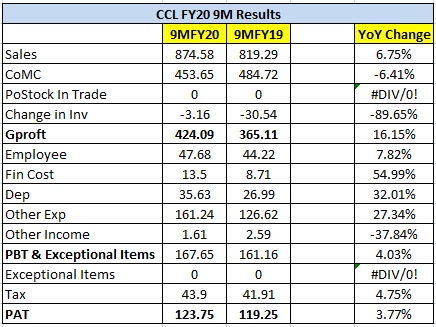

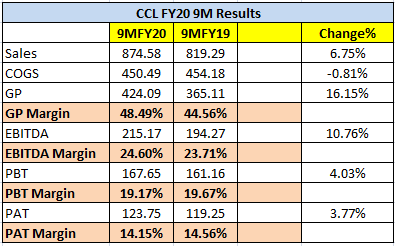

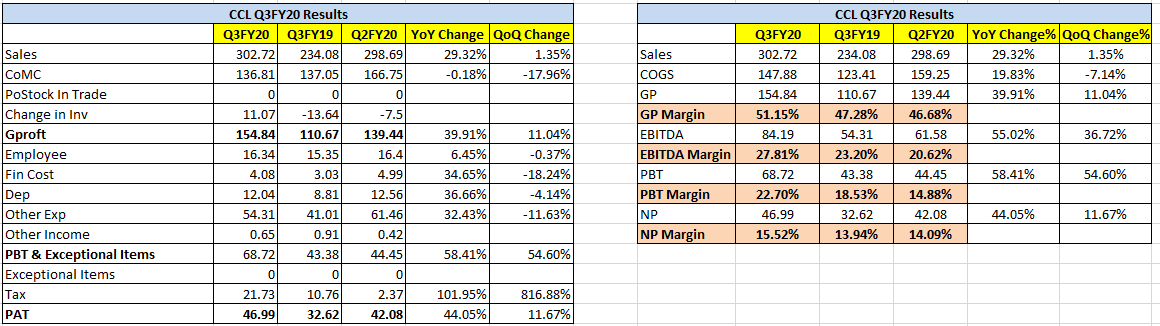

CCL Products_Q3_FY20.pdf (2.5 MB)

- Performance in-line with management commentary.

- Rs. 2 interim dividend declared with record date as 7th Feb 2020.

9M numbers look flat but a lot of money being spent for bringing future growth especially from domestic business.

GM are impressive for this quarter.

8 Likes

Q3FY20 Concall Update

Domestic Business: The company has started the freeze dried capacity during the quarter which is aided in improving the margins. CCL is looking for 80% capacity utilization next year. The management believes that current margins are sustainable. On customer addition, the company is expected to add one major customer from this year. Going forward, the key margin drivers are (1) Freeze dried capacity (2) Retail business (3) Shift from opportunist customers to brand owners

MEIS (export incentive) – booked 30 cr till now on cash basis.

Vietnam is operating at optimal capacity @70-75%. Due to the product mix, the output has reduced during the quarter. Seeing the steady demand, the company is increasing the capacity next year with capex of $8mn (for 3500MT). The company is expecting 75-80% capacity utilization next year.

Retail is growing steadily. The company is expected to close the year with retail sales of Rs 100 cr out of which branded sales is Rs 50 cr as against last year of Rs 30 cr. It is likely to breakeven next year

13 Likes