Demand for coffee beans expected to drop by 1 million bags in 2020. Cafes, restaurants lose out as people brew their own coffee at home.

Expected second order effects of lack of travel and tourism on coffee consumption worldwide.

Demand for coffee beans expected to drop by 1 million bags in 2020. Cafes, restaurants lose out as people brew their own coffee at home.

Expected second order effects of lack of travel and tourism on coffee consumption worldwide.

Some €3 billion is spent on tea a year, nearly all of that on traditional black tea. But black tea is losing popularity in North America and Europe and this is reportedly straining Unilver budgets.

Hey, you have mentioned here that their incentives end in 2020. Could you share the source or update on that?

Thanks!

(Most of the points might have been covered in this thread)

Coffee is a very sticky category. They become your habit and gets inside your daily routine. Sometimes, if you don’t get a good cup of coffee in the morning your whole mood gets spoiled for the day. So, changing this habit can be quite difficult.

Thinking about the point mentioned above I started analysis of a company called CCL Products (India) Ltd.

![]()

CCL Products (India) Ltd was formed set up in 1994 and commenced commercial operations in 1995. It is an export oriented unit with the ability to import green coffee into India from any part of the world and export the same to any part of the world, at cost advantage like with no/less duties due to benefits received by trade agreements between nations.

Continental Coffee Limited Products India [CCL Products (India)] deals in two segment B2B and B2C.

Here is an image to explain their B2B segment:

Source: Axis Securities

So, as the image above shows CCL Products (India) Ltd is in processing business. They buy raw material and process the coffee beans and then export it to their customers.

Company does not own any coffee plantations instead they procure green coffee from Chikmagalur in Karnataka, India as well as imports premium variety like Robusta and Arabica from Vietnam and Ethiopia respectively and then does the processing.

The company works at cost-plus business model. They do not stock any raw-materials and places the order for the same only after getting an order for coffee, this protects them from coffee price fluctuations.

Further, CCL Products (India) Ltd has now also entered into consumer business.

They have launched their own consumer brand, Continental Coffee and plans to take it slowly instead of rushing it like they did in 1997.

In 1997, they had only one plain vanilla product therefore they had no USP which led to quite a bad experience. Company had to withdrawn there product due to bad response. Company was new to consumer market that time. They had done a nationwide launch of the product without understanding of the Indian market, which led to the failure.

But now they have entered the market after 20 years with the understanding of the market and taking things slowly to check the response. For example: company currently deals in South India market only and plans to expand on after gaining 5% market share.

But why would their existing customer ask for small pack from them?

If a customer takes small packs order from CCL the customer would also get cost advantage as their would be no middleman.

Earlier CCL used to process the coffee and then export it to various location from there the coffee used to be transported to the customer after getting packed in small packages but now all this can be done from one location!

10. They expand only after the demand. Like they did recently. Only the new plant in Chitoor is under debt and rest are debt free. So, currently the company focuses on clearly off debt.

11. Management thinks that their current margins are sustainable due to their new freeze dry capacity, better technology, & new processes which are helping them get better yield.

12. Company has built such strong relations that they also take advise from their customers on how to build their facilities so that it caters to customer’s demand.

13. Company has recently crack into USA market which will lead to doubling of their revenues in USA. It took them 3-4 years to get the approval. This creates an enter barrier for competitors as they can’t one fine day decide to enter USA market.

14. Comparing with competition both the players (Nescafe & Bru) the advantage which CCL has is economies of scale. CCL has double production capacity, which means per kg cost is going to be lower than the competition.

15. The company saves cost on transportation with regard to India as they receive exemption of income tax from Vietnam. Also, Vietnam enjoy MFN status with many countries which helps the company save cost.

There is lots of competition as there is lots of excess capacity in world. There is competition from Brazil, Mexico, Singapore, Malaysia, China, Vietnam, India, Europe.

But CCL Products (India) Ltd has still maintained its good position. The reasons being:

In Prof. Sanjay Bakshi’s article, Seven Intelligent Fanatics from India, he inverts the management analysis and gives four elements of dumb behavior which are as follows:

Regarding the first point company has taken debt for their SEZ plant only and rest of their all plants are debt free. This shows that debt is for excessive.

Second point can be covered by noticing that company is not carefully expanding their B2C unlike their actions in 1997. Currently then only operate in south India and plans to expand only after gaining 5% market share.

Further, they had declined Joythy Labs offer to make new products as they were at full capacity. They could have taken debt and expanded but that would have been an unwise move. As the company only expands if there is demand. There was no guarantee of repeat orders or any new demand.

For the third point we can see that company’s core business is related to coffee and they deal in products related to that only. So, I think there are no signs of ‘DIWORSEFICATION’.

Forth point deals with ability to delegate. There is not such information regarding that but I believe they have a team which is handling their domestic business.

I try to follow the expected return model which is followed by Prof. Sanjay Bakshi. Here is the link to it: (click here)

Its a three step process:

As said by Prof. Sanjay Bakshi such practice provides margin of safety by:

“The idea behind the above is to create multiple sources of margin of safety. The first point delivers a margin of safety by keeping you away from bad businesses. Investors should recognize that margin of safety, apart from a low price, can also come from a high-quality business. “

This valuation is made further simpler by using an excel sheet (provided by Safal Niveshak, thanks to him!):

Remember depending completely on Excel can be quite dangerous sometimes. As people tend to tweak it as per their needs.

What I follow is after my thorough analysis I just put in the numbers in the excel sheet and if the market cap is near the discounted value I would buy shares of the company.

CCL Products (India) Ltd has a cost-efficient business model, long-standing relationships with customers as the product has stickiness, economies of scale as they are the lowest cost producer, they have the expertise to produce the right blends and their location which saves them logistical costs helps the company get an edge over competitors.

——

I am attaching my notes on their Conference Calls. You can have a look if you are interested in understanding my analysis. (click here)

Further if you want to be updated with my findings on CCL Products (India) Ltd follow my thread on Twitter: (Click Here)

Sources: Annual Reports, Conference Calls & as cited during the article.

Disclaimer: I am not a SEBI registered adviser. All the information provided by me are for educational/informational purposes only.

Wonderful Analysis. Wanted to know how did you value the business?

Were you including the India branded business in the calculations? Looking at your model, I don’t think you are including it and probably not giving any value to it which can add as additional margin of safety.

Like you have shown here, company has significantly improved its operating metrics over the last few years resulting in return ratios improvement. Wanted to know if you have adjusted the forecasted PnL for the likelihood of MEIS scheme (7% of exports in the past which is now 5% of exports) getting withdrawn and the resultant impact on the fair value of the business

Thanks for the compliment.

For calculation I had taken the company’s consolidated number. (I guess that means that the Indian branded business is included.)

Yes, you are right I have not cantered the reduction in the scheme. Thanks for reminding!

Also, I would request you to not pay much attention to my valuation if you are very serious about valuation, as I am not good at it.

I keep it very simple and follow what Sanjay Bakshi had explained in their email exchange with Safal Niveshak.

Hi, I know you mentioned that the 40% growth rate for their own branded products is sustainable. i have a couple questions with regard to the growth rate in the future.

I just am not sure if there is a clear growth path for them currently. Maybe they can expand like they have done so in the past. But now that they have reached maximum capacities (and demand) in B2B plus untested B2C business, I worry about sustainable growth.

Hey Pavandeep,

I welcome your opinion on the same.

Disclosure: Invested.

Thanks for the answer. Great to know that they grew the domestic part by 40% in the quarter as well.

My quesry regarding the second point was not referring to any competition. I think they definitely have the scale advantage. However, I heard management interviews where Mr. Challa has mentioned that they will see lower growth in the bulk segment because the instant coffee market is only so big and there is not a lot of room to grow there which is why they stated B2C, however because they recently added the free-dried unit, it shows that they are consistently expanding production. I do not know however, if the management is positive about the growth in the B2B segment which makes me think that they will be relying on the domestic B2C business for any further growth.

Yes you are right. That is one of the reason they had started to enter B2C.

I think easy growth can be a task for B2B but currently I think that is far away as:

These point give me enough confidence to stay invested

And I would also like to mention that in their recent con-call management said that they are planning to enter the pod segment which is currently a 35 billion dollar market and is expected to be 51 billion by 2027.

Also, If you are interested here is my analysis on their recent con-call with some pointers at the end: https://drive.google.com/file/d/1S1d-2Amjgt5tX7uiK2fe39sgAE3nzMjL/view?usp=sharing

(please don’t mind my awful handwriting)

Cheers!

Hello guys, just wanted to share my experience.

I recently tried Freeze Dried Coffee of CCL Products (India) Ltd. As I am not a coffee person, it tastes same to me compared with Nescafe. But I could could definitely feel the different in the aroma.

CCL Coffee’s aroma felt way better to me as it gave me a sense of natural coffee where Nescafe (the normal one, not GOLD) felt as if there was some enhancer included inside of it.

This is my personal opinion and heavily biased!

(If there is any different way to make such premium coffee please suggest.)

Item No.2

To confirm the first and second interim dividend of Rs. 2/- and Rs. 3/- each, respectively, to

the shareholders for the financial year 2019-20.

The brand has now entered in Mumbai, as one of my friends recently purchased it from CCD near his house.

All the local shops (Kirana) in Karnataka started advertising continental coffee with small sachets.

The only trigger here is that lot of people ended buying tata, bru or nescafe due to cost.

Continental coffee are expensive.

That’s strange to hear. Because management boast about them being a low cost producer and here they are trying to capture the market with charging a premium.

I hope they have a solid plan against the giants.

Could you please specify the price different between all of them.

(But good to now that they are present in all Kirana shops )

Flipkart :  !

!

CONTINENTAL Freeze Dried Coffee Beans Price in India - Buy CONTINENTAL Freeze Dried Coffee Beans online at Flipkart.com!!!g!575714134555!&gclid=CjwKCAjwkJj6BRA-EiwA0ZVPVuVg_6fKFSPXnp4V0NWSeQDTWXWn3VrCt8u9aqrbNQnmn-D2rkfRKxoCSV0QAvD_BwE

Nescafe Classic Instant Coffee Price in India - Buy Nescafe Classic Instant Coffee online at Flipkart.com!!!g!827078438786!&gclid=CjwKCAjwkJj6BRA-EiwA0ZVPVtDpybh1Gj2hUQ736QZFlPcFMPjav_L-QYpzAYSnzrFQJn9erjit8hoCyVgQAvD_BwE

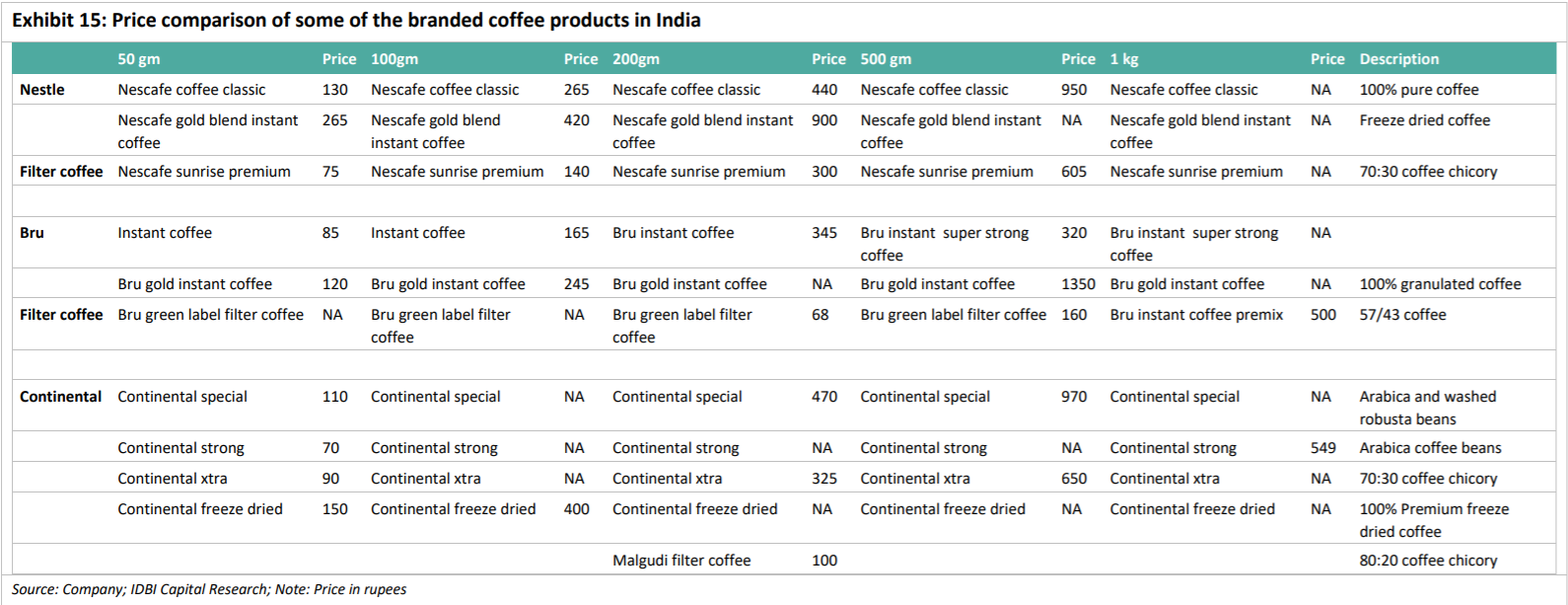

You can see the MRP for continental - High compared to Nescafe.

Coffee sachets available at rupees 2 which is same as Bru/Nescafe - however in minds of people Bru is imprinted

In MORE retails stores - have seen packets lying there for months then had to ask the lady about the sales - basically she mentioned price is high and people prefer local coffee first then Nescafe at last CCL.

I doubt that CCL will deleverage the prices - definitely Nescafe and Bru might increase price margins to meet CCL - if CCL catches up customer demand.

Thanks for sharing the details.

First of all I wanted to let you know that we are comparing the wrong types of coffee here.

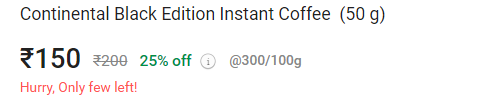

CCL Black edition is a frezee dried coffee which is premium one compares to Nescafe(Classic).

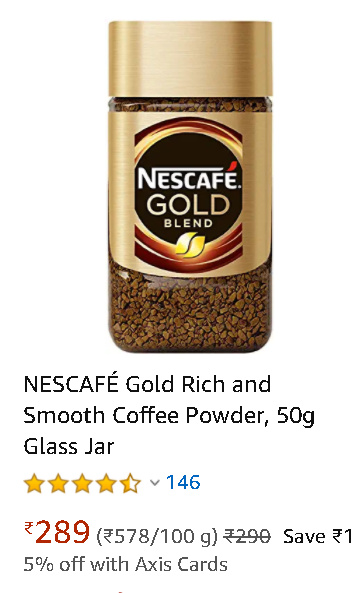

For a fare comparison we have to compare CCL Black edition with Nescafe Gold

But we need to add Rs 50 as there is delivery charges for CCL coffee which makes it Rs200, whereas Nescafe stands between 270-290.

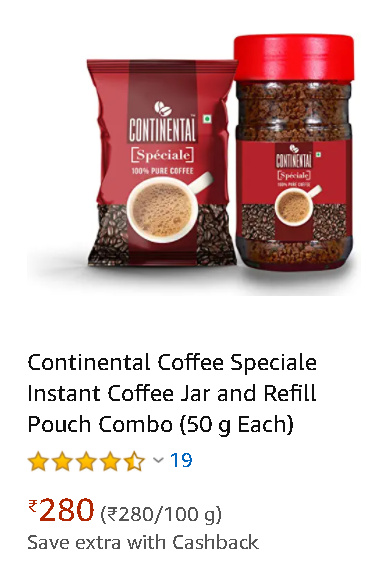

Now for Nescafe Classic we should compare it with Continental Speciale

Nestle provides 50g for Rs150 and CCL provides 100g for 330 (280+50)

Pricing does not seems a big issue to me as it can be easily dealt with the management and as we have Praveen with us who has great background in marketing I think he knows what he is doing.

But, you mentioning that CCL products was available everywhere is a huge plus sign for me!

I am sorry, I am having a hard time analyzing your data properly. Does this show that CCL is the lowest cost producer?