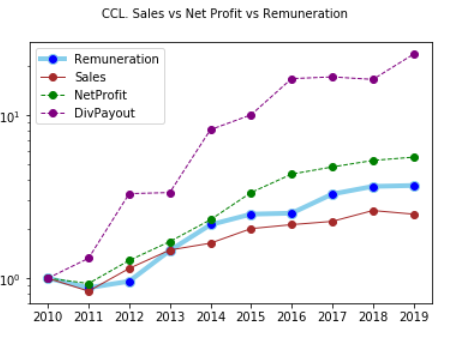

I wanted to see the historical trend of the management performance by comparing the sales, net profit, dividend payout and management remuneration.

Please let me know what you think about this approach.

Here is a chart of the numbers, base lined to 1 starting from FY 2010.

Source code:

import pandas as pd

import matplotlib.pyplot as plt

FY_2010 = 4.2287324

FY_2011 = 2.2851753 + 1.41

FY_2012 = 3.7037 + 0.3458

FY_2013 = 5.9259 + 0.3298

FY_2014 = 8.68 + 0.3298

FY_2015 = 9.5535 + 0.1245 + 0.4500 + 0.3298

FY_2016 = 10.6035

FY_2017 = 13.8955

FY_2018 = 15.487

FY_2019 = 15.6846

data = {

'Remuneration':[FY_2010, FY_2011, FY_2012, FY_2013, FY_2014, FY_2015, FY_2016, FY_2017, FY_2018, FY_2019],

'Sales':[ 437, 364, 502, 651, 717, 881, 932, 976, 1138, 1081],

'NetProfit':[28, 26, 36, 47, 64, 94, 122, 135, 148, 155],

'DivPayoutPct':[7, 10, 18, 14, 25, 21, 27, 25, 22, 30],

'Year':['2010', '2011', '2012', '2013', '2014', '2015', '2016', '2017', '2018', '2019']

}

df = pd.DataFrame(data, columns = ['Remuneration', 'Sales', 'NetProfit', 'Year','DivPayoutPct'])

df['DivPayout'] = df.NetProfit * df.DivPayoutPct * 0.01

df.Remuneration = df.Remuneration / df.Remuneration.iloc[0]

df.DivPayout = df.DivPayout / df.DivPayout.iloc[0]

df.Sales = df.Sales / df.Sales.iloc[0]

df.NetProfit = df.NetProfit / df.NetProfit.iloc[0]

# multiple line plot

fig = plt.figure()

fig.suptitle('CCL. Sales vs Net Profit vs Remuneration', fontsize=10)

plt.plot( 'Year','Remuneration', data=df, marker='o', markerfacecolor='blue', markersize=8, color='skyblue', linewidth=4)

plt.plot( 'Year','Sales', data=df, marker='o', color='brown', linewidth=1)

plt.plot( 'Year','NetProfit', data=df, marker='o', color='green', linewidth=1, linestyle='dashed')

plt.plot( 'Year','DivPayout', data=df, marker='o', color='purple', linewidth=1, linestyle='dashed')

plt.legend()

plt.yscale("log")

plt.draw()

Not a Recommendation.

Disc: Invested (about 5% of portfolio).