CCL came out with quarterly results today:

Below is the concall summary: (please cross-check with original transcript once it is out)

-

Revenue growth guidance consistent around 15-20%

-

Vietnam volume similar to last year (except a dispatch of a pending order) - lower off-take

-

Domestic market volume was flat due to effect of severe summer

-

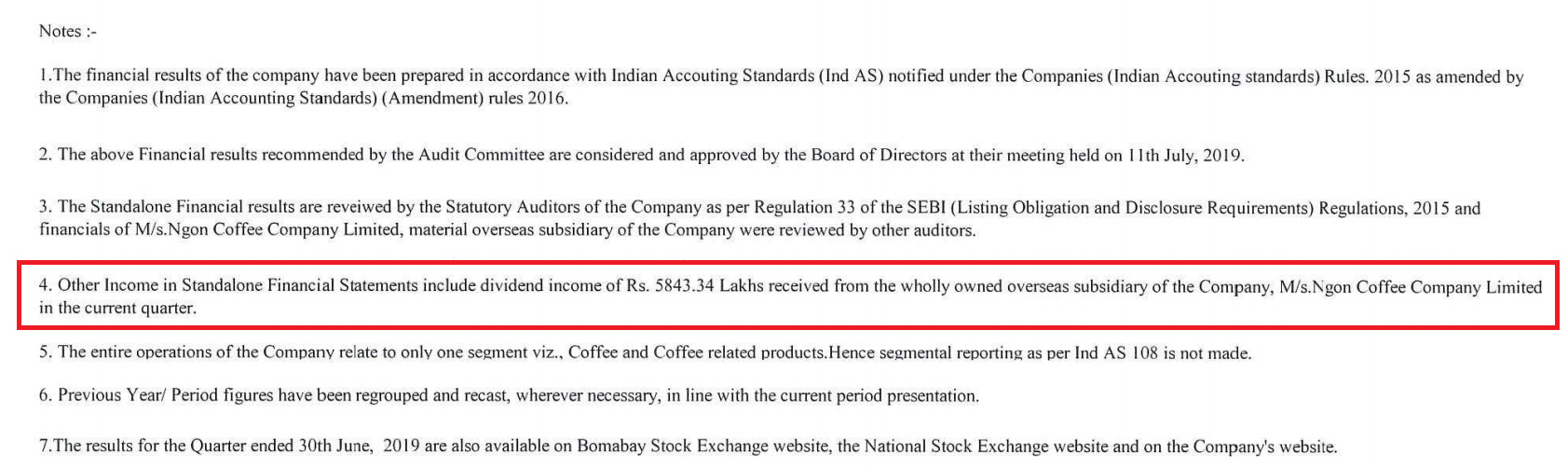

Dividend payout reason: Amount for capex provisioned, remaining amount got as dividend (~58 cr); Vietnam entity now debt-free

-

Rise in depreciation due to operational SEZ started in April this year; Same with deferred tax increase

-

Volume contribution from Europe ~1/3

-

Coffee price decline impact on freeze dried coffee: Realizations has come down vs. what it was 2 years back; This will be new normal for now

-

Freeze dried plant to run full capacity in 1-2 years (can contribute 270-300 cr at full capacity)

-

Domestic business: ~15 cr.; It was lean quarter vs. 8-9 cr. QoQ (continental);

-

FSME law in-force, not being effectively enforced; Some uptick in US now visible (there is 20-25% growth in US, current volumes ~2,500 tonnes)

-

Packaging capacity can come on-line by this FY and commercial production could start in Q1 next FY

-

Volume loss due to loss of customer last quarter: might again start buying few quality of products; Added few other customers on premium side which will help to meet revenue guidance

-

Debt repayment over next 4 years; OPM broadly in-line with Q1 2019

-

Price premium of freeze dried ~20%

-

Capacity utilization (across all plants) ~90% (except SEZ which will be 50%)

-

Depreciation and finance cost run-rate to remain same for this year

-

Freeze dried till date from new plant ~300-400 tonnes production

-

Branded India business: additional 15 cr spend projected; Next year might break-even

-

Profit growth guidance ~10-15%