Aug 2021 data. QoQ growth of 25%. Acrysil does 75% in export revenue and quarterly revenue run rate is around 100cr (maybe more in Q2), 70% of which is exports i.e. INR 70cr. So we have USD 10mn of exports in 3mo or around USD 3.3mn every month.

Therefore, Acrysil would be around 20 to 25% of the numbers shown in trade portal. Maybe a bit more because expanded capacities got commissioned in June 2021 if i remember correctly.

Hello. I have the following silly questions on Acrysil, if someone can please answer them:

Regarding the partnerships with IKEA, Grohe etc., given that contract manufacturing is B2B and IKEA would have multiple suppliers, I believe margins in partnerships would be lower. What impact will this have on overall margins?

Are they giving % contribution to sales of contract manufacturing partnerships v/s own brands? (I could not find it)

Since they are importing moulds, are there domestic suppliers available where it can be procured at lower cost?

Given the rise in debt levels in recent years (perhaps to fund capex), are there plans to deleverage?

Going ahead, will incremental capital (in capex, R&D, advertising etc.) go towards quartz sinks or stainless steel sinks or appliances or bath?

What is the competitive landscape in kitchen appliances segment? I am guessing there is fierce competition already present with strong brands e.g. Faber in chimneys

Can appliances products be sold through existing distribution network?

The distribution network has remained flat for past 2-3 years because of insufficient capacity to supply, so with the new capacities coming up, is it reasonable to expect the distribution network also to expand and if yes what could be the potential numbers?

Are they giving % distribution of A, B and C category dealers?

Thank you.

Disc- not holding but researching and tracking closely

I believe that since Acrysil is only one of the few suppliers in the world with Quartz technology, therefore, bargaining power would be more in the hands of Acrysil. You add in the low cost Indian mfg and suppliers would definitely not mind Acrysil making a few more bucks since big retailers (like Ikea etc) typically play on volumes.

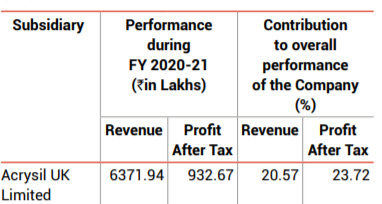

Good question. I don’t think they are giving this number but you can estimate fairly reasonably since all exports are basically contract manufacturing (apart from those to UK subsidiary).

My guess again would be that for the moulds, it would be a tie-up from Shock GmbH. So imports from them would be part of the larger technology tie-up.

We need to wait for H2FY22 balance sheet to see the debt levels. Lets not forget that they had also passed a board resolution for fund raising through QIP. So i don’t think debt would be of any concern here. Growth drivers are the key monitorable in Acrysil i.e. tie-ups, export volumes, etc.

No such guidance but from the past trend, its clear that they’ve been on an expansion spree of quartz sink capacity. And that’s the product which is gaining traction in foreign markets as well because of the natural feel of the product.

I don’t think Acrysil competes with them. Their products in the appliance segment cater to niche (ice cube maker, wine chiller, etc.) and luxury segment in India. Not many players there today I guess?

We’ll have to check this. But from the limited I know, the channels for appliance and sinks etc are quite different.

They have said that they will focus more on domestic markets and recent marketing efforts do point to that. But we need to get more insights on the distribution network etc on the latest con call.

And exports is 79% so to confirm approximately 59% of revenue (non-UK exports) is contract mfg? Exact figure may vary of course but is my understanding correct?

It’ll be higher than 59% since revenue of UK subsidiary includes the profits kept by UK subsidiary. I see that the profit of UK subsidiary is 15%. You can roughly expect that exports to UK would be 10/15% with rest of the margin kept by UK subsidiary for its own expenses / profits etc.

EDIT - Margin in exports vs domestic margins. I’m not fully sure on this. While contract mfg margins are lower, but exports also come with benefits. RoDTEP in future for example.

Just went through the annual report. A bit late but still it would be grateful if someone could help me with a few doubts:

The company mentiones of being among the top 4 globally in quartz sink manufacturing using german tech. Who are the other 3 players? What is the market share of this german technology within the global quartz kitchen sink market? Any pros and cons of this german tech with the other available tech?

Any idea of the annual supply contract with IKEA? (any fixed volumes)

The annual report talks about IoT and Artificial Intelligence. Is acrysil already using them or are they giving a hint of their future plans?

Risk factore mentioned “Entry of New Players” saying that business could be impacted by new players deploying comparable ‘networking prowess’. Someone using better tech and quality is a valid risk factor but what do they mean by ‘networking prowess’. Does it mean that rather than its products, the management feels that their contacts and connections are a better USP for the company?

Company states that it is the first PVD sink manufacturer in the the country. Now PVD is primarily for stainless steel kitchen sinks. PVD tech is supposed to provide better glamor and finish to steel sinks. If such a great tech, then what was stopping the other players (eg. Nirali) from using the same till now?

2% of PAT being paid as commission to Mr. Parekh. A possible red flag?

The other 3 are Blanko, Schock, Franke

Acrysil is the only one in Asia

I am not aware of this either. Management mentioned that the opportunity could be large but they haven’t quantified how large. This might help:

Not sure but my guess is they are referring to the distribution network perhaps. Also, contacts and connections are helping them get contract manufacturing business from IKEA, Grohe etc. and this may be a competitive advantage

I am unaware of the other questions.

Disc- no holdings but researching and tracking closely

These are more buzzwords every co likes to use today. Take them with a pinch of salt. As of now Acrysil has a) ultra premium sinkware and bathroom accessories and niche kitchen appliances. We do not know R&D efforts etc beyond this to understand if there are any actual investments in IoT, AI, etc.

Don’t think so. Infact it is linked to PAT, which is a key factor for the larger shareholders as well, so i’m pretty happy if he gets 2% of PAT as commission.

Btw was it PAT or PBT? The accounting would be a circular error if its PAT

I am sorry to have called it PAT. Its actually profits calculated as per section 198 of companies act (the calculations are little different than what we see in our P&L statement).

But my point of calling it a possible red flag was commissons would give you an incentive to fudge with P&L as per your convinience.

Why would you risk so much to take out a few crs? Would have been easier to receive higher salary. I personally think any promoter taking higher bonus and less salary is a great thing.

At work, will look at the results later but my quick takeaways:-

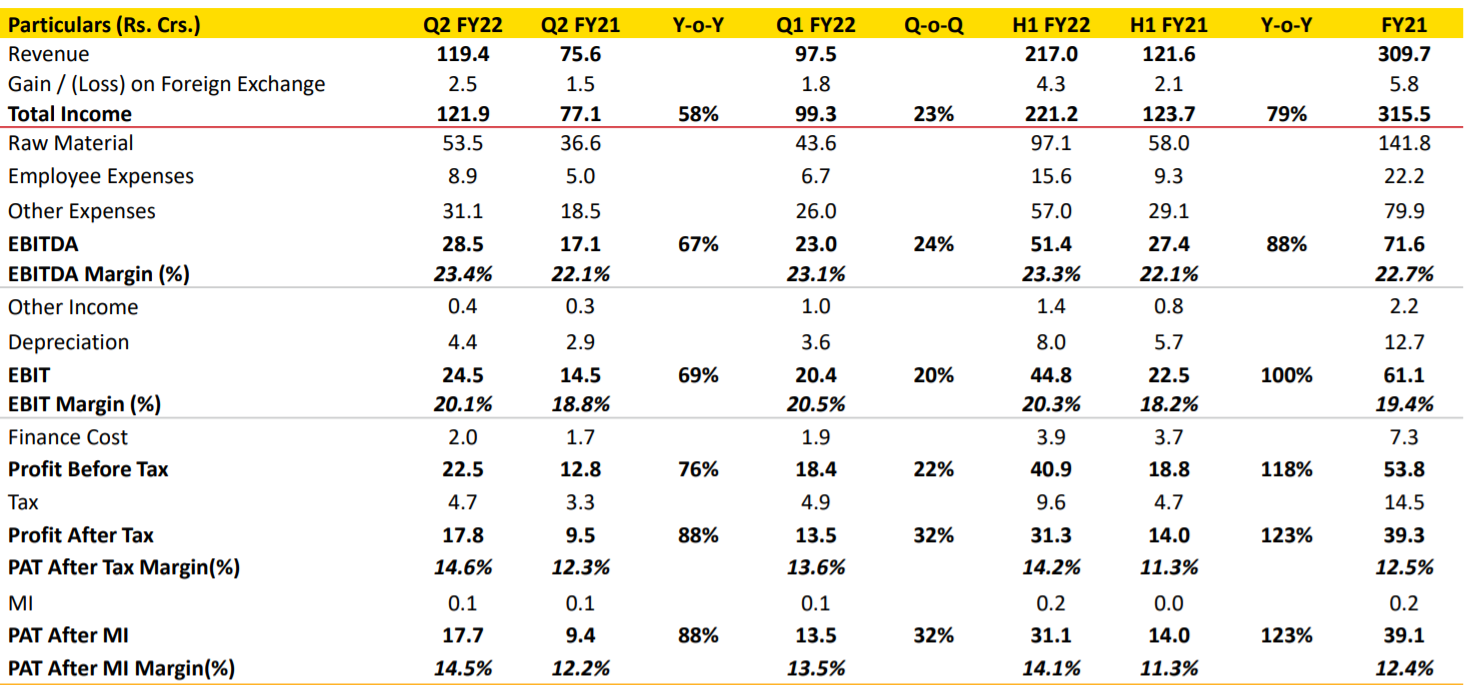

Revenue increasing QoQ by almost 20%

Board meeting took place in Washington just days after US opened travel

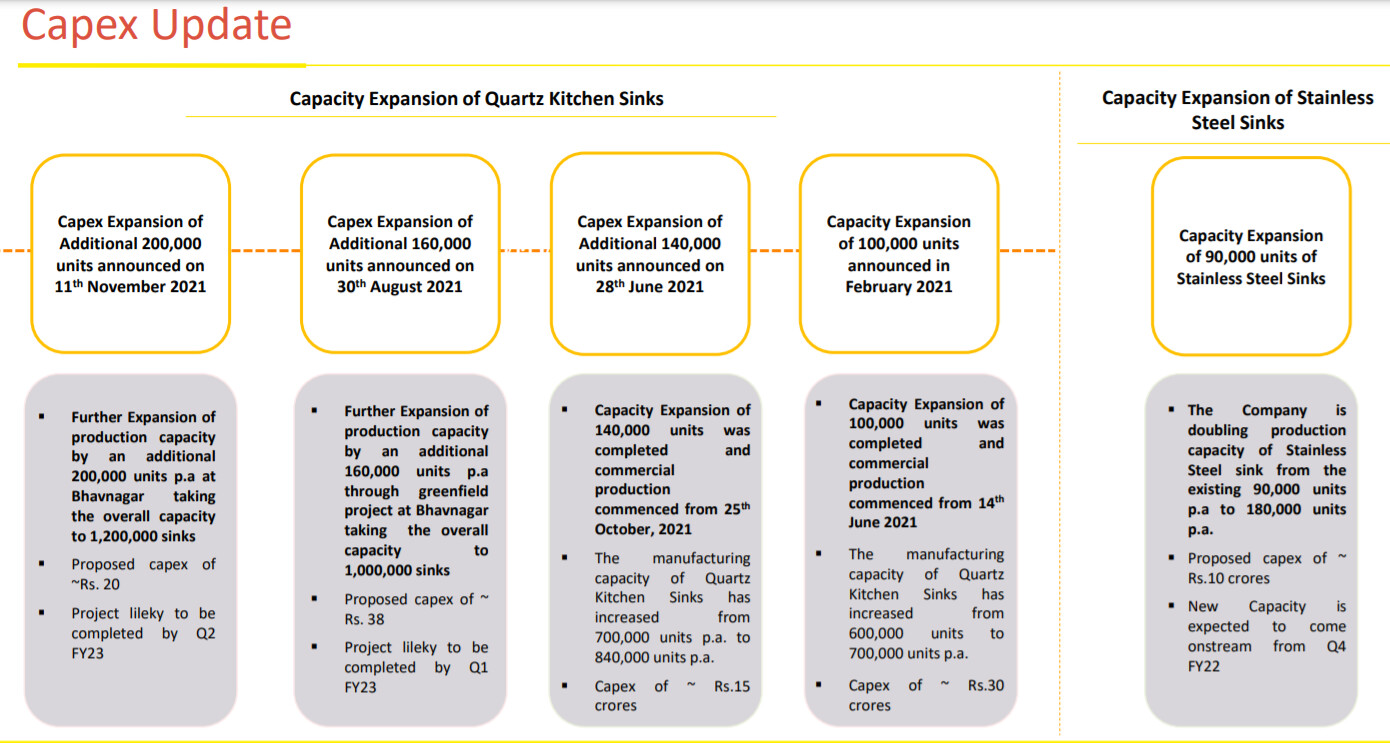

Acrysil announcing additional capex. Total capacity to be ramped upto 1.2mn units now.

#2 and #3 are not coincidences. Demand drivers are roaring here.

Capacity utilisation numbers need to be closely tracked since new capacities came on steam during Q2 and have also come online during Q3. Gradual ramp up will lead to better operating leverage.

As on date, commissioned capacity is 840k units. 360k units more to be commissioned and capex yet to be fully utilised. Lots of steam left in this counter.

Acrysil Limited (“The Company”), largest manufacturer of “Quartz Kitchen Sinks” in Asia with German Technology, has announced additional production capacity expansion by 20% (200,000 Quartz Kitchen Sinks p.a.) at Bhavnagar in Gujarat. Thus taking the Overall Capacity to 1.20 million sinks (1,200,000 sinks) p.a. from current announced capacity of 1 million sinks (1,000,000 sinks) p.a.

The expansion in production capacity is to meet the growing demand of Quartz Kitchen Sinks in the Domestic & Global markets. The proposed Capital Expenditure involves an investment of Rs.20 Crores approx. in Building, Moulds, Plant & Machinery, Utilities and other related infrastructure. The project is likely to be completed by end of Q2 FY2023 and will be financed by mix of internal accruals and debt.

Going thro’ today’s results it seems like the Employee Benefits expenses have almost doubled from the previous year. As per the notes included:

Employee benefits expense for the current quarter include Employee Stock Options (ESOP) Compensation Cost of Rs.98.49 Lakhs and Rs.122.35 Lakhs in the Standalone and Consolidated Financial Results respectively

Couple of questions:

Are these ESOP expenses part of the normal course of business or are there any concerns ?

119crs revenue (we need to see the segmental breakup for quartz) is on a capacity of 700k (not optimally utilised is my guess). Assuming 80% revenue from Quartz sinks, we get to 96crs of revenue from quartz sinks. This can potentially double by the end of next year assuming that Acrysil reaches optimum utilisation by Q4FY23.

Capex involves low cash and quarterly OCF more than covers their capex needs (if you ignore WC needs since that can vary quarter to quarter). Things to watch out for in tomorrow’s con call:-

QIP plans - why and when?

Dividend policy in future

Quartz - more steam left? Any update on partnerships? Volume offtake from IKEA, Lowe’s, others

Plans on other business lines especially kitchen appliances.

1H22 revenues Rs217crs. With better capacity utilization in 2HFY22 Rs500crs revenues could be possible. Extrapolating hence 1HFY22 14.1% PAT margins to FY22 one can expect Rs70.5crs of profits in FY22.

Stock market cap is Rs2153crs so stock is trading at 30.5x FY22E with great demand from IKEA, Grohe and Menards

Completed expansion of 140,000 units of Quartz sinks in October 2021.

Announced greenfield expansion of 160,000 units in August 21 which is progressing as per schedule and further announce additional capacity expansion by 200,000 units taking our total capacity to 1.2 million sinks by Q2 FY23.

Raising of capital through Issue of securities to Qualified Institutional Buyers through a Qualified

Institutional Placement (“QIP”) subject to the approval of Shareholders, for an aggregate amount

not exceeding Rs.150 crore…

Current 1.2mn capex is looking at the current demand estimates and our desire to fulfil all orders in time. And we’re seeing a massive demand surge.

Demand driven by renovations outside India and by new home constructions in India

Renovation demand is cyclical with it picking up every 4/5 years

We’re the sole supplier to Grohe and one of the many suppliers to Ikea, Menards and Lowe’s.

Received 5 star feedback rating from IKEA a month back;

200k capex is at a site adjacent to existing Acrysil mfg site

Scoping nearby locations to acquire land for further capex

H1FY22 quartz sinks volume was 375k (indicates high capacity utilisation and going forward volume gains would be from incremental commissioning of the capex)

Realisation per sink is roughly around 5500, so every 100k capacity gives 55cr in revenues

Protected margins through FoB sales and partial price increases. “We are a margin conscious company”

Capex has a short lead time from commissioning to optimal capacity utilisation since the demand scenario is very strong.

Cost competitiveness is an advantage for Acrysil (on questions of Shcock itself setting up a plant in USA) and demand / market is huge (5 to 10% of overall sinks is Quartz and consumer preference is changing)

Domestic Market

Existing 200k capex is considering demand in mind which is seeing a “sudden spurt”

Roped in a brand manager to focus on branding activities

Want to remain niche and not be a mass player - the branding is aspirational

Plan to upgrade dealers to large showrooms

QIP

Looking at adjacencies - 2 of which were given as examples (mentioned below)

High technology ceramic tiles (for export markets) which would be first of a kind in India OR faucets as a complement to kitchen sinks

China

Current surge for Acrysil has two components to it. One demand surge due to pandemic.

Inability of China to make good this demand due to them shutting down many units and geopolitics

Future Guidance

“Long-term has become short term for us”

New vision statement soon

Sounded confident to hit 500crs annual revenue in FY22 itself.

Want to export to 100 countries

My conviction has increased further in this counter and it feels Acrysil will gain a lot due to global and Indian housing boom courtesy low interest rates.