I think fund raising through QIP is best option. Company will achieve several objectives. First, large amount can be raised. Second, Company will get visibility with funds raised from reputed institutions. Company will save on interest cost if it had opted for debt. Equity dilution will be low, as QIP can be done at current market price or at a premium.

I am not aware whether technical tie up is valid for Green field expansion and whether Company is presently paying for the tie up.

One thing is clear. Company’s products are very much in demand and it is a big positive for share price.

2 Likes

April 2021 exports

May 2021 exports

June data isn’t uploaded yet.

Note - I checked and this HSN code would NOT include tiles. (Tiles HSN begins with 69). Also the HSN code that i pulled the data from was sourced from https://usimports.info/exporter-acrysil-limited/data-1.html

12 Likes

Do you have similar data for the 4 quarters of FY21?

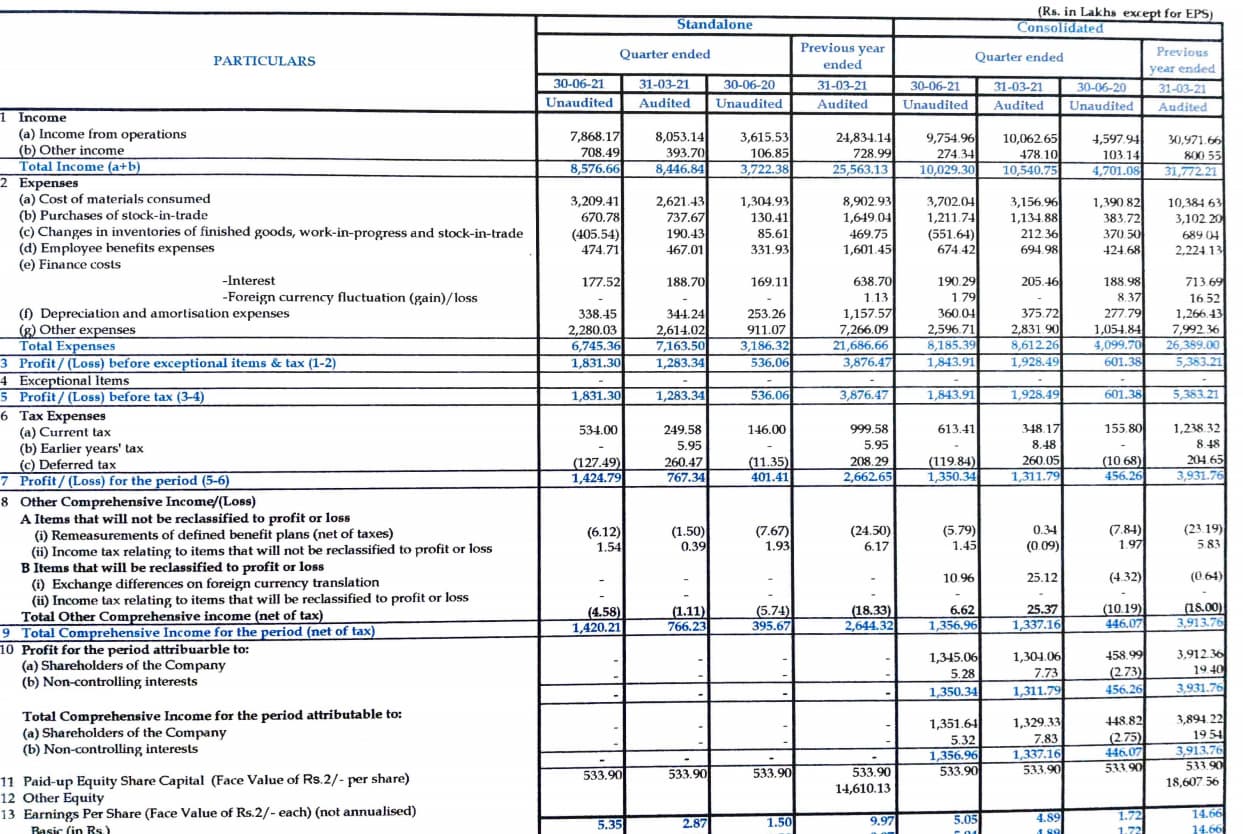

Result June 21

2 Likes

On cursory glance, the result looks very good. Though turnover is somewhat down QOQ, the net profit has gone up by a big margin. Even after adjustment of one time dividend received from subsidiary, net profit has gone up. This is quite an achievement, considering 2nd wave of pandemic and cyclone. Considering monopoly status of the Company and expectations of demand after unlocking, this appears to be a stock worth tracking and buying considering one’s own judgement.

6 Likes

Superb showing in very tough operating conditions.The QIP is definitely the most interesting aspect.Hopefully this ~9% dilution will be for new greenfield capex.

1 Like

Consolidated revenues up 112% and profits up 196% YoY. Wonder why company is not hosting a post results conference call? 150crs QIP

1 Like

Comprehensive analysis of Acrysil covering all aspects by @Worldlywiseinvestors

7 Likes

Summary of the SOIC Analysis presented below

Contract manufacturer for quartz sink kitchen workstations, using customised moulds for companies like Grohe etc. Indian brand is retailed as Carysil. US, UK, Germany are key markets. Strong growth in FY22, thereafter greenfield capacity expansion is required

Overall

• One of the 4 manufacturers of Quartz sinks – Acrysil, Schock, Blanco, Franke; only quartz sink manufacturer in India (Carysil brand – known for its premiumness, competing with cheap Chinese imports or Hindware) and Asia.

• Acrysil establishing themselves as a preferred global supplier with cost competitiveness. Scope to increase market share high – ie capture market share from other players as well as increase volumes due to a growing market

• Sector tailwinds, especially for next 2-3 years

a) Recovery in world housing market: US being the fastest

growing market with demand from housing starts.

b) Shift in Taste and Preference from Stainless steel sinks to

Granite sinks (Composite Granite is Quartz) – 10 yrs ago, 3%

of total sinks (market size of 8-9 mn sinks) were quartz;

currently, it is 8% of total sinks ; of this Schock technology

based sinks is 75%

• Current capacity is 7 lakh tpa; 6 lakh for quartz sinks, 0.9 lakh for stainless steel sinks and 0.1 lakh tpa for kitchen appliances.

• Technology:

a) Technical know-how through access to Schock Technology which

leads to higher precision & lower manufacturing defects.

b) In stainless steel sinks, they are bringing a PVD vapourisation

technology for which they incurred Rs 3 cr capex; stainless steel

with metallic finish

• Advantages of quartz sinks over traditional sinks – stain resistant; anti-bacterial treatment, scratch proof, UV protected. Quartz sinks are made from 76-80% quartz and 20-24% acrylic with easy installation. Finishing better than Hindware

• Strong partnerships with Ikea (contract manufacturing agreement for proven models Quartz sinks. Acrysil will take market share of current suppliers and this can be a very large opportunity), Grohe (contract manufacturing for Grohe for quad sinks and now stainless steel sinks), Menard (confirmed orders for Rs 25cr; will expand to 18 SKUs from 4 SKUs tie up to sell quad sinks), B&Q, Homebase, Home Depot and Lowes (online sales program). Grohe is 10% of export sales (started as Rs 50-60 cr annual order, which was achieved in 7 months itself). If capacity constraints are removed, more strategic tie-ups possible

• Sets up customised moulds for clients

• Indian quartz sink market is growing at 20%

Revenue profile: In FY21, 76% Quartz sinks, 14% Steel sinks, 10% are kitchen appliances

80% of revenues are exports which comes through contract manufacturing and rest 20% is domestic business. They started focussing on domestic business from FY12 onwards- dealer network has increased to 1500 in 2021 from 400 in FY14; and now have a pan-India network; distribution strength higher in south as compared to the rest of the country

Future revenues (assuming 8.4 lakh tpa capacity onstream) will become~ Rs 462 cr, assuming constant realisation of Rs 5500. In FY21, revenues were Rs 315 cr. Company has guided a medium-term revenue target (12-18 months) of Rs 500 cr and long term revenue target of Rs 1000 cr.

Long term revenue target: The existing location can only house 8.4 lakh tpa and there is no further land for expansion. They will need to go for greenfield expansion in FY23, likely doing a QIP for the same to reach long term revenue target.

Volumes:

• 20% capacity expansion from 7 lakh tpa to 8.4 lakh tpa by Q3FY22

• Housing sector tailwind in US and India (share of domestic sales increasing)

• Growth in India will come with a lag (although market is growing from a small base), but main growth is coming from exports to Western countries (especially US).

Margin expansion:

410 bps GPM to 55% and 470 bps EBITDA margin expansion to 22.7% in FY21 vs FY20. Average price realisation increasing – starting prices of quartz sink is Rs 7500 till Rs 40,000

Maintained net working capital – especially important since this is an export driven business

Strong management execution capabilities

RISKS:

• Threat of substitutes for quartz sinks

• Capital misallocation in newer segments

• Slow-down in US housing market

• One time product and not an annuity product. There is no repeat business, even though management claims replacement cycle of 5 -6 years. This company can become a large fish in small pond

PS: Invested

21 Likes

Not sure if it has been noted by the forum or not but the MD in his opening remarks in the investor presentation has said that they are conducting prelim activities to take the capacity to 1mn eventually.

So in a years time, we’re seeing the company announcing nearly double the capex.

2 Likes

Any updates on the investor call held today between analysts and the management?

Annual Report now avaliable

10a33c03-ed96-4074-8df0-a4ae65c56996.pdf (5.3 MB)

Another capex announcement of 160,000 quartz sinks barely a couple of months after the last one but this time it’s a greenfield project in Bhavnagar as they’d have run out of space at the current facility.

Overall capacity will soon touch 1 million sinks by Q1FY23, doubling the capacity from 500,000 just 1 year back.

Phenomenal growth backed by the solid real estate boom across the globe.

Disc: Invested from 75 levels

10 Likes

Real Estate boom is definitely on full swing. But why such rapid expansion just with the quartz sinks? Why is the company not able to capture the real estate upswing with its home appliances and bathroom fittings?

1 Like

As per statement, company witnessing huge global demand. Expansion is basically to met the global demand. Indian market is still lagging. As Indian we are getting ready for these high quality sink. There is low penetration of quartz sink in Indian market. Till now we are believing in old steel type sink only. When quartz sink will gain share in the Indian market, Acrysil will be direct beneficiary of that…

Views are biased

Discl: Invested

4 Likes

Their products are very premium products and most of the real estate developers don’t use that kind of premium products, this might be one the reason may be.

1 Like

July 2021

Good growth. Q2 should be good too. Aug data not out yet but expected to be on similar lines especially with the increased capacity on steam and no 2nd wave effect on manufacturing.

5 Likes

Thank you for the info, But HS data is a generic.export data for the kind of material explained in the code, how can we make sure this export data is for acrysil?

Is there any way to find company wise data ?

Thanks

Abhilash

If you see my post above, you can see where i’ve picked the HSN code from. Also, Acrysil did 100cr in June quarter. Assuming a 30cr run rate, that’s around USD 4mn or 30% of the exports coming up under this HSN. Not a perfect barometer, but a decent one.

Also, if you have any better way to find the monthly sales data, please share. That would indeed be very helpful

Updated investor presentation: