Like Acrysil is doing contract manufacturing in quartz sinks for Grohe, IKEA etc., is there any potential for contract manufacturing for global players in the appliances segment also?

Disc- no holdings but researching and tracking closely

Like Acrysil is doing contract manufacturing in quartz sinks for Grohe, IKEA etc., is there any potential for contract manufacturing for global players in the appliances segment also?

Disc- no holdings but researching and tracking closely

The quartz sink vols in H1 were 301,273 and not 375k.This implies ~90% utilisation and more importantly this means peak revenue at 4x of H1 revenue,i.e.,~900 cr.Going by company’s current margins they should be doing 200 cr. kind of EBITDA at the peak.Since all the new capacity won’t be available for FY23,we are looking at 750-800cr. revenue next FY.Going by the mgt commentary it doesn’t seem growth is going to fizzle out anytime soon so the juggernaut will keep rolling at good rates.Quartz sinks still being only at 10% of the total market gives ample room.

At 2100 cr. hard to assess how much of the growth markets are already capturing but this is a well protected business with very good promoters so it could continue to trade at good multiples as long as growth rates remain strong…

Disc.: Invested.Views are biased.

Don’t think so and I doubt they’d be interested in that since it would conflict with their own business. Also, they are not into typical contract manufacturing. Worthwhile to remember that they’re driving the technology process when it comes to Quartz sink and only manufacturing as per customer design, etc. That’s vastly different from what a Dixon does and the margin profile also reflects that.

My sense is next move would be a first of the kind product in India type of product line. Lets see though.

So based on the above interview, looks like Acrysil could do revenues of Rs500crs in FY22 and Rs750crs in FY23. Assuming 14.1% PAT margin (same as that of 1HFY22) one can look at profits of Rs70.5crs in FY22 and Rs106crs in FY23 which implies at the current market cap of Rs2377crs the stock is trading at a P/E of 33.7x FY22E and 22.5x FY23E

Nicely done @vnktshb!

I think the next step should be to understand future triggers for Acrysil. Most of the earnings growth in future is now priced in the stock price. What could be the future earning triggers here?

Need to watch out for all the above.

The company will be investing 58crs in the two production lines for 3.6L sinks. Both these should be operational by Q2 next year.

At a average realisation of 5500/sink that should mean addition revenue of 198crs. This mean an asset turn of 2.75 times at 80% capacity utilisation.

Company has changed terms of sale to ex-factory from earlier CIF (this is the biggest reason why the margins have not contracted even when freight cost has sky rocketed)

Steel sink capacity also will be doubled to 180k sinks.

Did anyone catch the guidance on the composite tile segment. That’s something I couldn’t find in the concall.

All in all this looks like a rocking story. Im invested since March’21

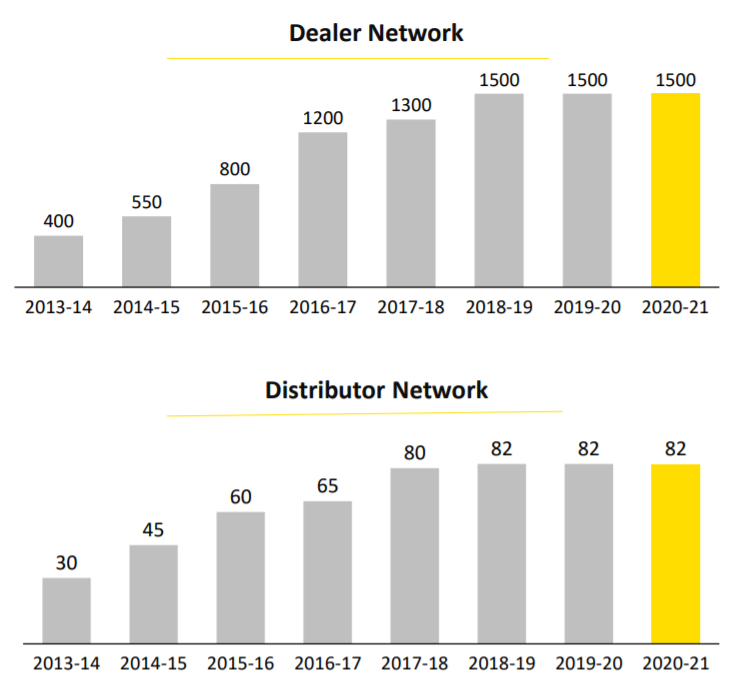

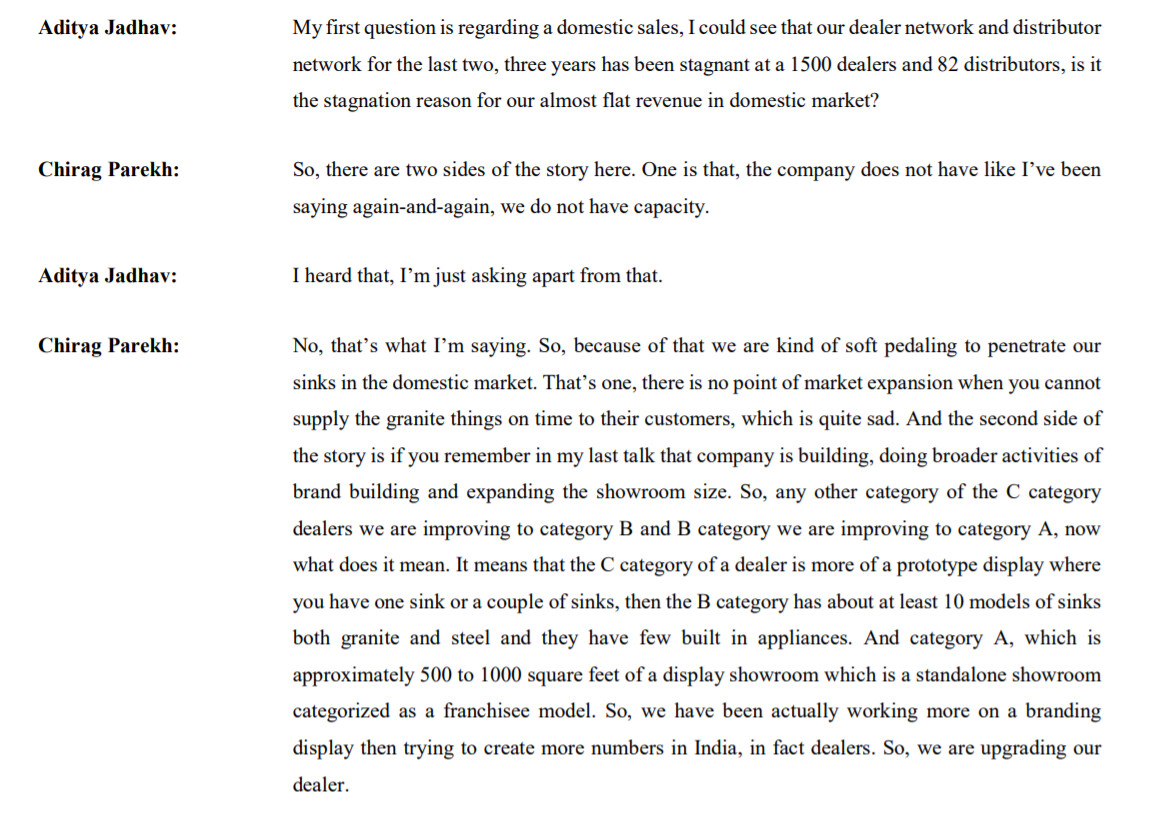

Domestic dealer and distributor networks have been constant for the past 3 years now.

What is the thought behind it? Using the existing channels to full capacity before making any further investements here or something else?

@TheWolf The management had answered this in Q1 FY22 concall. Relevant extract is below:

Perfect!

That clears up everything (much more on the positive side).

Thank You

Disc: Invested

If you see, Q2 concall also mentioned that the latest quartz capex is more due to domestic demand.

Hello everyone. I will most probably be participating in a group call with Acrysil management tomorrow. If anyone has questions, please do share and I will try asking. I will share notes post the meeting.

Disc- no holdings

What plans do they have for the QIP money utilisation & when will the QIP take place ?

They had mentioned about High End ceramic tiles as a project they like to focus on, whats the status on that?

Any further expansion plans for Quartz sinks for the next year?

Can you find out what plans they have for their Sternhagen brand of bath fittings and what is the path to achieve breakeven? And if they seeing any interest for this brand from their current clients?

Hi Malhar,

A few queries from my side which can help to understand the growth trajectory after FY23.

How do they see the share between domestic and exports segment change by FY 25? - it looks like FY23 is going to be even more skewed towards exports since they have a lot of orders on hand from large global retail chains for which the capacity addition is being done. However, given that they are quite confident about the domestic market too, how big can the domestic biz become by FY 25 and what would the share of exports and domestic segment be like then?

Does the company expect these export orders to sustain beyond FY 23? Given the cyclical high in housing worldwide currently, does the company expect demand to sustain in the medium term as well?

Disclosure - Invested from lower levels

Regards,

Vivek

Hi Malhar,

Great and thanks a lot for checking here :-). Much appreciated. Some questions below, in addition to those above.

Their long term target will be met in FY22 with Rs500crs revenues. And they expect Rs750crs in FY23. So what is their new long term target?

Here are my notes from the meeting with Acrysil CFO Mr Anand Sharma Sir. Please note that Q and A may not be ditto verbatim/word-for-word as what the participants said. Idea is to summarize and get the key points. Also, there were 3-4 other participants and not all questions are mine.

Q: There are four players having Schock technology for sinks. What is Acrysil’s edge over the other three?

A: All players having Schock technology have the same quality and quality is not different between these four players. But Acrysil has a cost advantage due to being based in India (e.g. labour cost).

Q: Are dealers and distributors Acrysil-exclusive i.e. they sell only Acrysil products?

A: Dealers are not exclusive but 90% of distributors are exclusive for Acrysil.

Q: There is a big RPT with Acrycol Minerals, can you please elaborate?

.

A: We are buying a raw material which is coated silica from Acrycol Minerals which is a promoter owned entity.

Q: Given that long term is now short term for us, are there any new targets?

A: We are not revising targets till the long term target is achieved.

Q: We have brought Vaani Kapoor on board so what is the ad budget?

A: Ad budget is 5% of FY22 domestic sales but it should not affect margins.

Q: Can you elaborate on contracts? Can we pass on RM price hikes?

A: Contract is a long term supply contract. The price is fixed for 6 months unless there is a very sharp RM price escalation. Otherwise, price is fixed for 6 months and it is a long term contract.

Q: What is the % split between category A, B and C dealers?

A: As of now we do not have the data and we are still progressing and working on these dealer upgradations and strengthening. We have noted your point and we can probably include this in the investor presentation from Q4 onwards.

Q: Is there potential for contract mfg in appliances like we are doing for sinks?

A: As of now we do not have. But the potential is there as they are happy with quality and the relationship is good so the potential is there.

Q: The margins in contract manufacturing would be lower as compared to our own brands?

A: In fact that is not the case. Gross margin is roughly same for both. On net margin in fact contract mfg has higher margins as own brands also have advertising costs etc. But this is the current status, it may change going forward with brand establishment.

Q: Sir, is the distribution network for kitchen appliances products the same as the existing one for the sinks or will we have to establish a new network altogether?

A: There is 80-85% overlap between the two networks. Remaining is a new network.

Q: What is the % contribution to revenue from contract manufacturing and what is the % from the sales of our own brands?

A: Domestic is 100% our own brands. Domestic is 20% and 80% is export. Now to add the portion where there is branded sales in exports. So 70% is contract and 30% is own brands.

Q: What is the competitive landscape in appliances segment especially in the domestic Indian market?

A: In appliances our products are customised, in-built appliances. There are 3-4 competitors but this is also a niche segment. Competition is there but growth potential is also there.

Hope this is able to add value.

Disc- no holdings

New Marketing campaign featured in AD magazine