Yes. It is composite quartz. 80% quartz and 20% acrylic and color pigments. Please refer to the quartz kitchen sinks catalogue on their website.

3 Likes

My learning from Acrysil

Acrysil was one of my high conviction bet, had 10% portfolio allocation and I was also tracking it closely.

I had a strong belief that it will break out in a year as financial performance was good, bottom lime, top line, margins improved YoY, management started focusing on domestic market and increased it footprints, and capacity additions were going on.

But the stock didn’t move at all and was range bound during my holding period. During Covid-19 meltdown I exited it and invested that money in other better opportunities. Rational behind my decision is

- EU countries especially UK was severely hit by Covid so predicted a business headwind as exports were main stream of revenue.

- saw it as a value trap and believed Covid will keep the stock in range bound for few more years.

But Acrysil never allowed me to enter back and rallied from there and become 4x from my buy price. The investments I made out of this money have paid off but still its a regret. Markets are crazy.

Few learnings

- Aarthi Drugs too had similar chart pattern, it was in a range bound for 5 years and suddenly become 5x. Some level of technicals could help to re-enter into such stocks.

- In such micro-caps we should have good patience and stay invested as long as business is doing good.

14 Likes

I wish I had that high a conviction when it came on one of my screener screens. This almost fulfilled all the characteristics of a Coffee Can business (10%+ consistent top line growth and ROCE > 15%) as defined by Saurabh Mukherjea (also behind the stupendous gains for me in Poly Medicure, Alkyl Amines, Indiamart, Vmart and many more) and I put a pretty small amount at work at 75 in July.

Happy that it has became 5x and can now foresee it becoming 10-15x in 5-7 years based on the recent management guidance of 500-1000 cr top line targets.

One of the best things I noticed in the investor presentation is the consistent 15-25% capacity expansions over the past several years. It shows a reasonably conservative attitude to capital deployment ensuring they’re fully confident about the future demand as and when they go for any capex. They don’t want to deploy huge sums of money in one go and then wait for a full 1-2 years till the capex shows up in the P/L like some pharma cos such as Laurus. This also reduces volatility in business performance which markets love and reward.

7 Likes

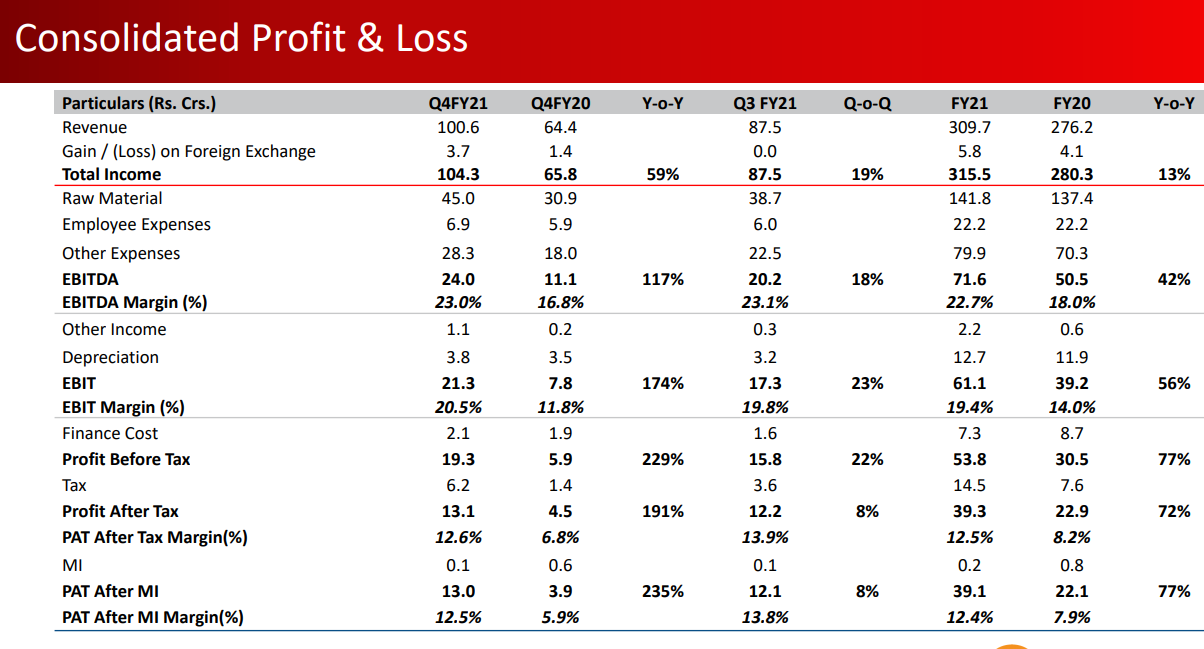

Look at this slide. The exit 4Q revenue run rate is Rs100crs. 4X100crs = Rs400crs. New capacity of 100K quartz sinks commissioned in Feb 2021 and another 100K coming in June 2021.

This implies revenues could be as high as Rs500crs in FY22. Assuming no operating leverage and hence 12.5% PAT margins (same as 4Q) Rs62.5crs of profits seem plausible.

Stock market cap is Rs1271crs so stock is trading at 20.3x FY22E with great demand from IKEA, Grohe and Menards

Disclosure: Invested

13 Likes

The Quartz Sinks primarily people call it as a term it as Granite Sinks and why people are liking the Granite Sinks is purely because they find it more of natural product. So most of the homes in India or abroad they use natural stones for our kitchen. So they will like to have another Granite Sinks, Quartz Sinks, which has fantastic colour, shapes, matching with you kitchen décor and so across the world this momentum of the granite has been picking up quite fast.

The above is extract from the Q4 FY 19 transcript.

2 Likes

Highly unlikely that Acrysil will do 500 cr. revenue in FY22 simply because the 2nd 100k capacity won’t be available for the full year.However,post q2 they could be doing a quarterly run rate of 125 cr.On the current land,they can take the capacity to ~1 million units,cash flows continue to be good.Mr. Parikh hinted in the call that they will be looking at a larger expansion in the next round and with the Western world seeing a strong economic rebound,demand for Acrysil’s products should remain steady if not improve further.

2 Likes

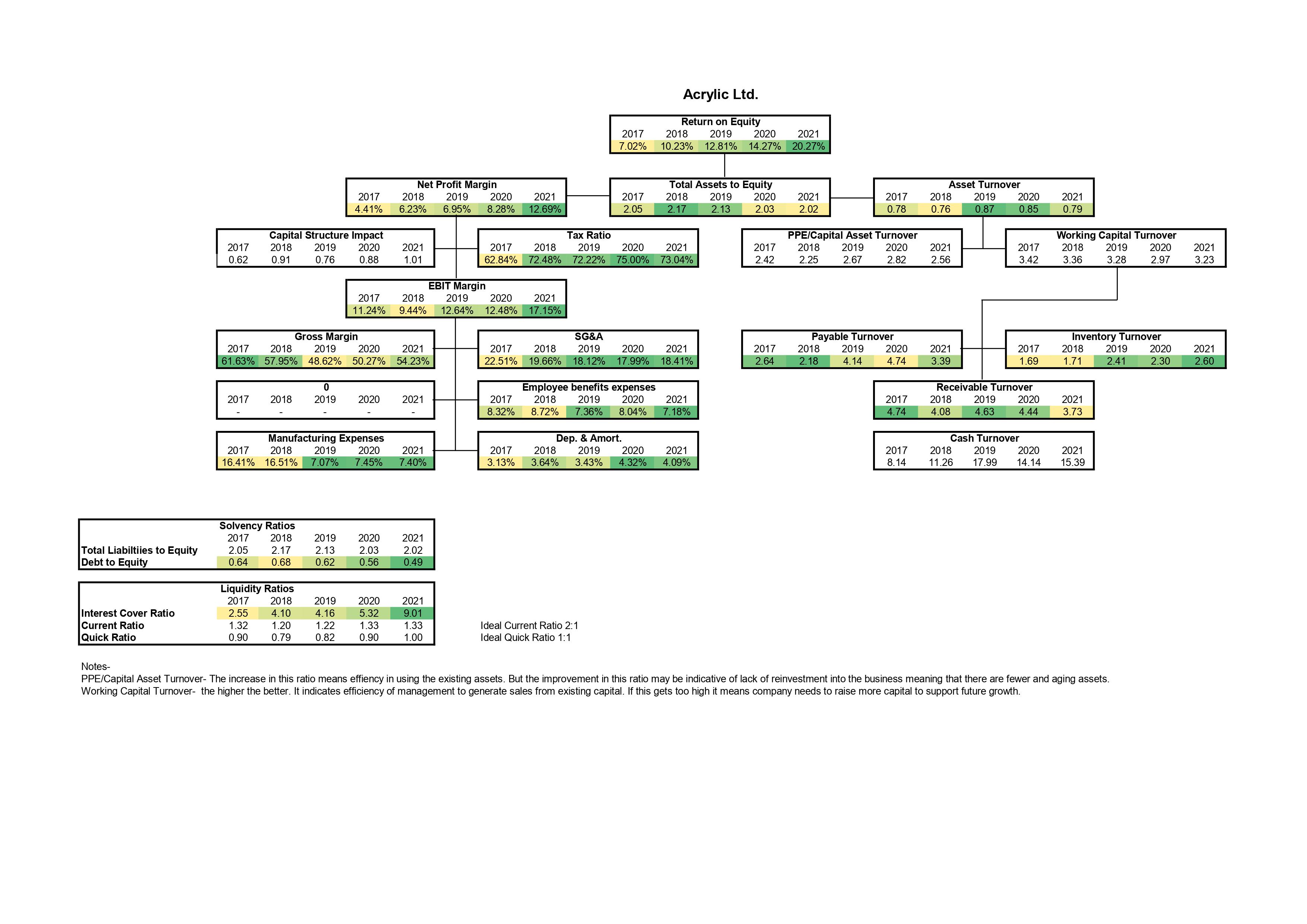

Anyone analyzing the potential of Acrysil must look at historical capital intensity and asset turnover ratio. Surprisingly, it has been a highly capital intensive business and asset turnover ratio is low.

One should analyze about possible dramatic change in future (if any) which would change the asset turnover ratio of the company and it would grow without significant incremental investments. Management’s growth guidance will be useful if there is clear answer to this.

2 Likes

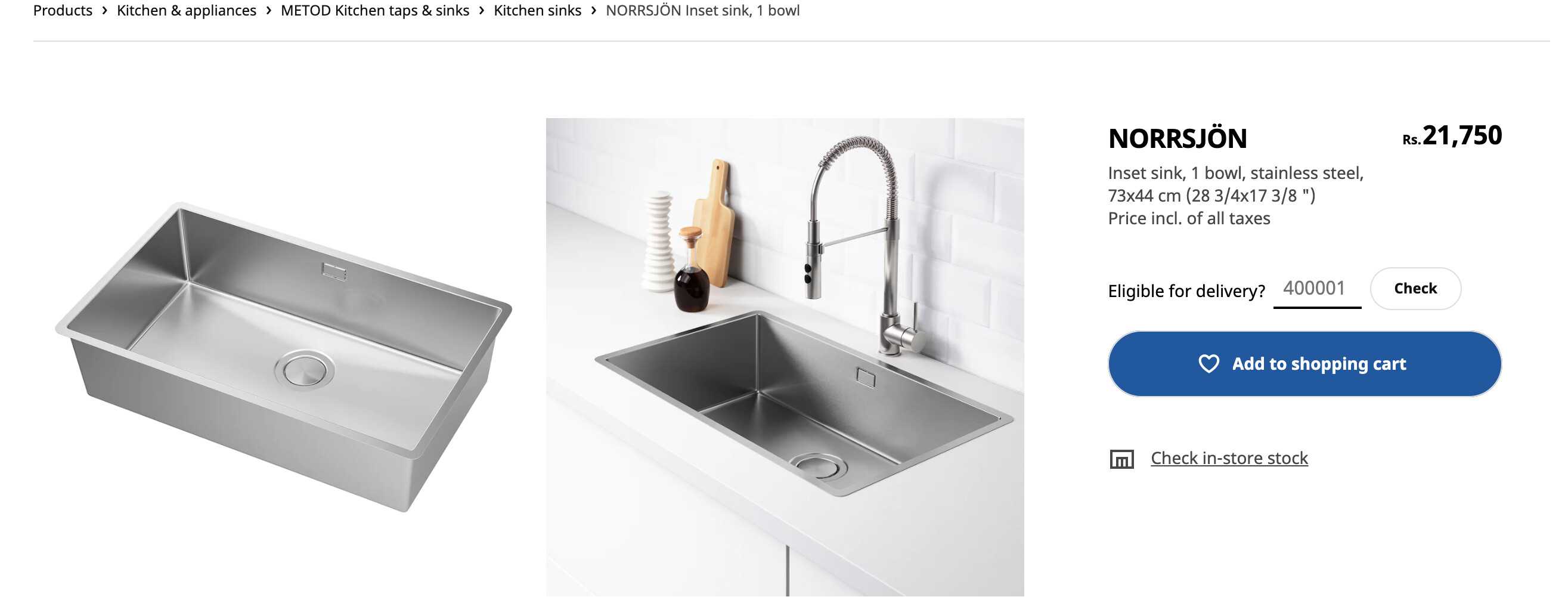

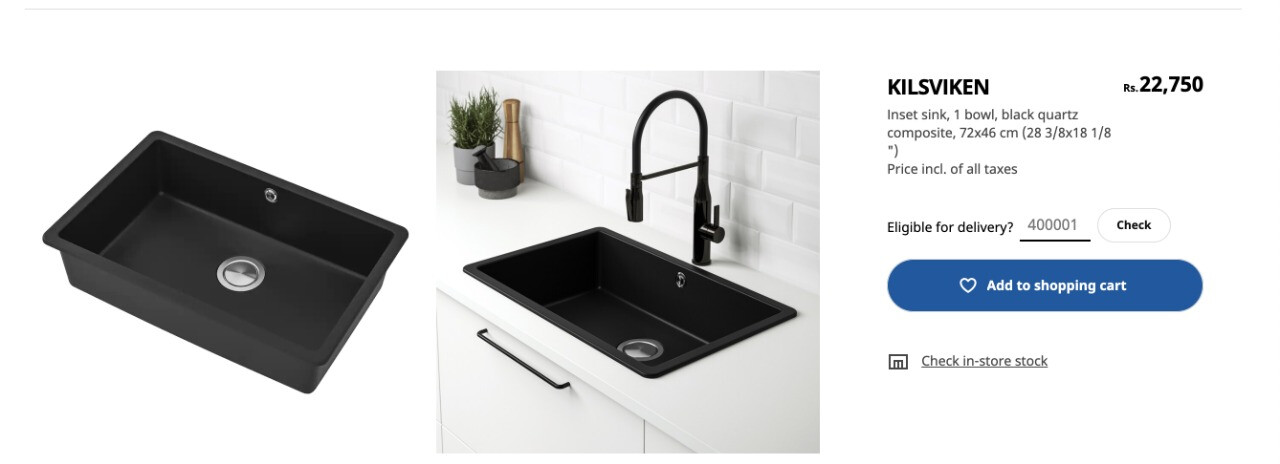

Just checked IKEA site. Even if one takes steel sinks and quartz sinks from IKEA, the price gap has reduced drastically.

A superior product now available at a small premium over steel sink.

2 Likes

The manufacturing capacity of Quartz Kitchen Sinks has increased from 600,000 units to 700,000 units per annum.

3 Likes

Agree. infact I see higher margins, and 70 cr PAT for fy 22 possible imho and good increase to 100 cr PAT in fy 23. developing story imho with more tie ups & capex.

Was lackluster earlier when exports used to grow at 12%, hence had gone domestic, but positive momentum makes it a different stock versus when it was Rs.200

disc: recent purchase. invested. Feel comfortable holding.

1 Like

Acrysil is expanding capacity by another 20%.This will take capacity to 840k units and revenue to 600 cr. at 100% utilisation.Management had earlier said that on the current land they can do about 1 million units at the most.The day is not far when company will have to seriously consider greenfield expansion.

12 Likes

Is it reasonable to expect that if products of Acrysil find good customer acceptance in US & elsewhere, then the margins of Acrysil from exports may see a further expansion considering greater leverage?

I was surfing Menards, which tied up with Acrysil for Quartz kitchen tops and I see products there are selling upwards of USD 300. The average realisation for Acrysil in Q4 was around 7000 per sink.

Can we see a concurrent margin growth along with volume growth?

1 Like

Acrysil having wide MOATS

Disc…invested

2 Likes

Is the schock technology they are using is only accessible to them or a new competitor can emerge and they can partner with schock too? Because often high growth industry or product attracts more companies and can be a bad sign for long term story of this business.

I have read pokarna also started manufacturing quartz sink ofc not with schock technology and they too parterned with ikea.

2 Likes

I dont know present status of shock technology liscence agreement.We also have to search out weather liscence is exclusive or nonexclusive to acrysil.

Shock gmbh has 8.47% share holding upto sept 2020.Then they have sold their holding.

Does someone know the HSN code for exports by Acrysil? Would be a good metric to track. Indian ceramic exports are rising but I guess this would be more tiles as many players have indicated in con calls.

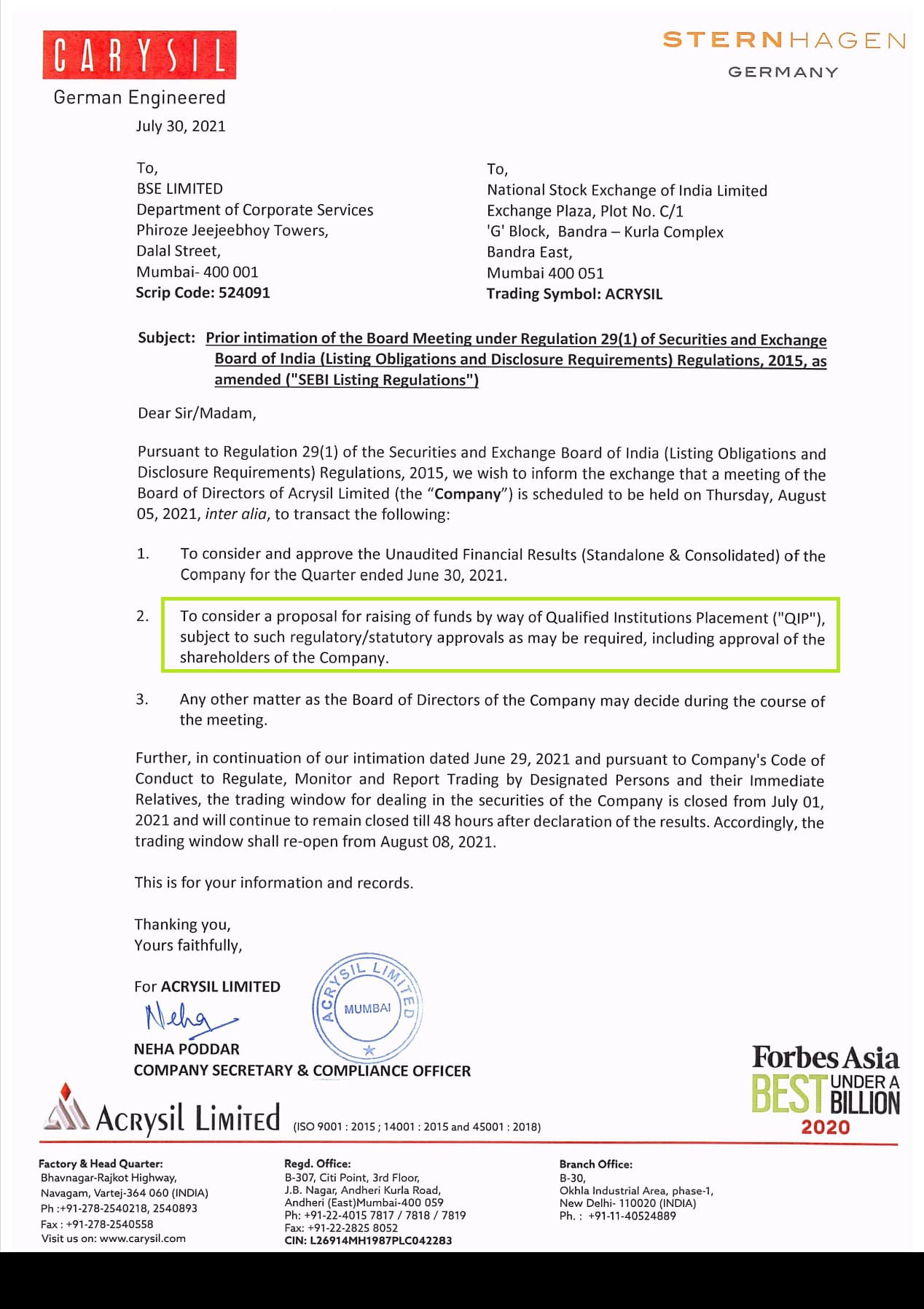

Really surprised by this decision. The new CapEx was supposed to be funded by debt and internal money.

I had noted earlier that the company will have to do a greenfield expansion since they’ll soon run out of land if demand keeps up.In that case,investment required will be much larger and that might not come from internal accruals in the quantum that the company requires.Though as of now it seems like an enabling resolution only.

5 Likes