Analogies doesnt work in making money. He is the master of analogies due to profession.

I am keenly looking at Care rating to add to my portfolio. Due to wrong doing by one person doesnt close down the company. Yes, it will be negatively impacted due to sentiments and bad results is part of the business cycle.

problem is there is a lack of buying interest in the markets causing excessive selling hit lower circuit. Prof Bakshi remarks looks more emotional to me than data driven.

As per regulations you have to get yourself rated with at least two rating agencies, Thats why we see two rating agencies name associated with any instrument sometimes all 3.

You cannot point gun out to just CARE doing fake ratings, There are other rating agencies too rated DHFL & IL&FS.

I think his tweet perhaps created a panic selling or there is something only insiders know that know one else know.

I think Prof Bakshi didn’t say anything wrong, He just pointed out the obvious that some of the revenue is gone forever due to some companies defaulted which were AAA rated.

Does it means there will not be any new addition in future ?

No.

He is not also thinking in Bayesian way, Giving more weight-age to few defaults over the over all track record of the company.

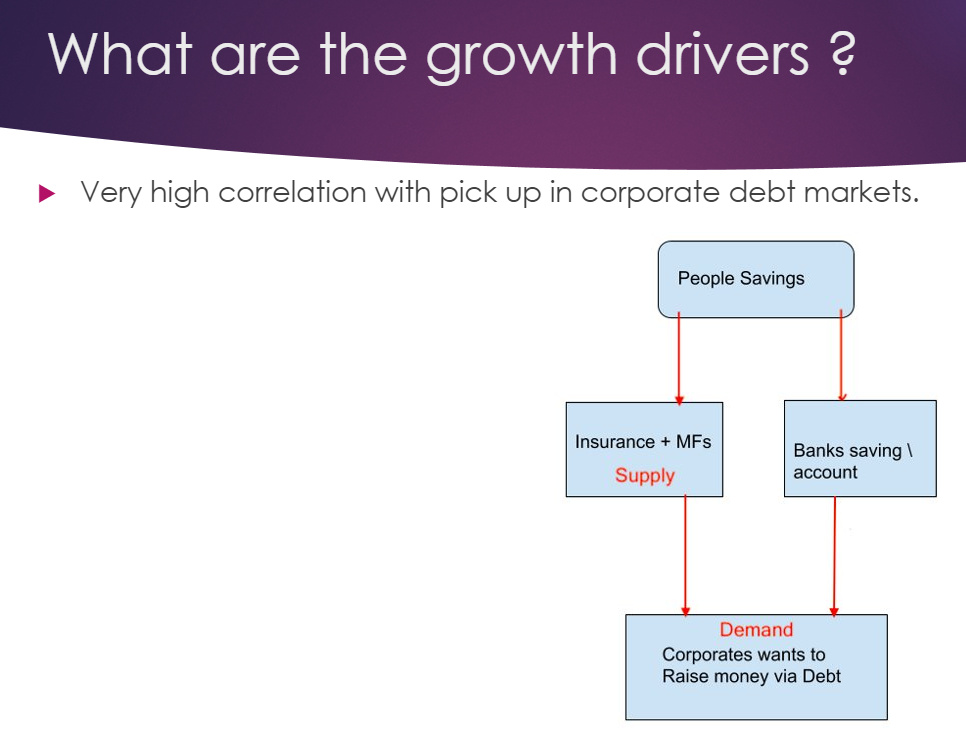

Net profit became half not because they lost revenue from DHFL & IL&FS and select few as they rate 1000’s of companies, its gone because the demand for debt is vanished from the economy ( Shown below - Demand driver )

Here flow to MFs Debt fund is -ve, Corporates not raising any Debt. either through BLR or Bond markets. Basically incremental demand is 0 in the market today ( not a forever phenomenon)

Does it means the Demand will never come back ? The answer is NO.

Now you may argue there is a certain part of the revenue which is recurring what happened to that? Like the instruments CARE rated in past has to be update YoY and those institutions pay YoY.

For this CARE clarifies the Cash has not come yet, The companies are delaying fee. Yes there are some ( very few) defaulted, won’t come into recurring revenue but there are many in stress and probably waiting it out to get themselves rated as nobody wants to get themselves rated in this economic scenario where their receivables are stuck with other ( but are good) , they might be waiting for them to become normal. ( if you go check ground conditions in SMEs everyone is saying Payment lene baad mein aana, Dhanda ruka hua h)

I would argue this is a Pause not Reset for CARE ratings.

Secondly, Earning call some analysts asked how come you your competitors are doing okay and you are doing bad? That means you are losing market share and she was pointing towards CRISIL.

CRISIL - Does 30% revenue from Ratings and if they would have reported their rating segment-wise revenue ( i didn’t check) it must have declined in line with CARE.

Coming back to Prof point they rate Rated " FAKE AAA and its all gone" - Its a right statement in a sense yes maybe 10-15% ( at max ) of the revenue gone forever but that gone for CRISIL and ICRA too, they rated them as well.

No company can do NCD if not rated by at least two rating agencies.

since 1993 of CARE existence many have defaulted overtime and many came up overtime, CARE / ICRA /CRISIL continue to grow their rating books. Its not end of the road.

It sounds more emotional to me than Bayesian to me, because data doesn’t support that.

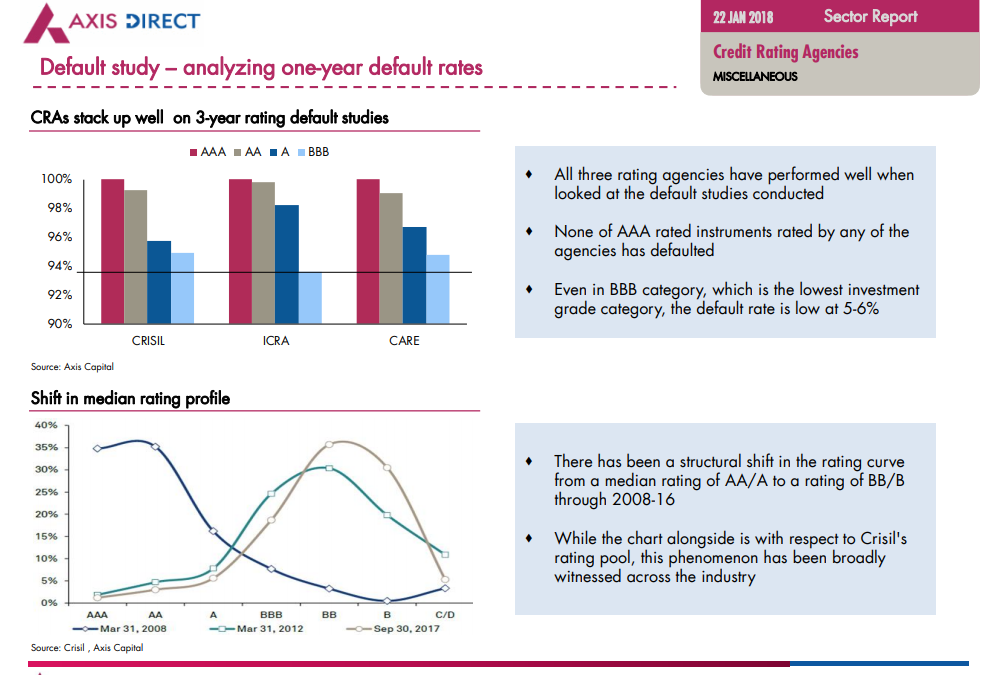

If you look at default study of all previous AAA rated instrument by rating agencies you will realize one IL&FS case is the only miss before that they had 100% track record ( AAA rated never defaulted ).

IL&FS - also if you read rating report they all assumed this company has sovereign guarantee due its PSU promoters, Thats the miss. I think only few like Prof. knew beforehand that what all is FAKE AAA.

Most of mortal like us don’t have crystal ball to know whats going to default in future.

Here is another non- Bayesian type of reply to a good question -

First of all - there is no single NBFC NCD that is rated by CARE alone ( as you need at least two by regulation) .

secondly, If you use think Bayesian way by calculating no. of default vs the number of rated instruments you get not all revenue is phony FAKE AAA revenue. Many instruments they rated AAA, AA etc are doing okay have not defaulted.

CARE has changed the revenue recognition now they are booking only when cash comes in, and Cash is delayed by the companies they rate, most of which are SMEs. i think most of the revenue showed this Q1 is from BLR which used to be about 50% of their total revenue anyway.

This is not doomsday scenario and CARE is not all FAKE – AAA rating agency, their 1993 to 2019 track record doesn’t say that. Util IL&FS none of the AAA rated company defaulted in India.

Whatever happened will force rating agencies to improve and its a good thing.

SEBI did assessment of [

Assessment of Long Term Performance of Credit Rating Agencies

Well, hate to say that “I told you so”. I have tried to imply the same thing few times on this thread. What he is saying that there is a plain vanilla rating biz in which there is not much margin due to competition. The cream biz i.e. ‘distributing’ rating is over for now. You have double whammy of falling volumes along with “high margin” biz being taken away. Of course they would recover to pre-ILFS era earning level in a few years but with reduced margins and return ratios if they survive this storm. Corporate india will take 2 yrs to get over with the trauma of over leveraging and liquidity stress.

I believe it is good thing , it might result in a better sustainable business model .

you are right . From a slightly different perspective will country like India needs bond/debt rating . Is it feasible that all the financial institution have their own internal rating mechanism. A fairly large economy like India would definitely need rating agencies .I dont think these companies are going away and best time to accumulate is when every one think sky is falling .

No he is not saying that, India has 3 big rating agencies controlling 95% markets among themselves, Many other tried competing and failed. Same is the case in U.S and in many other countries.

why 3 ? Because by regulations to raise bonds you have get rated by at least 2 independent rating agencies.so, generally market share revolve around the 3.

If at all somebody has to worry about getting out bid, it has to be CRISIL and ICRA because CARE employee cost is the least but i don’t think they have to compete crazily with each other due to the way market works.

Just on the basis of Q1 one should not conclude that its over , CARE lost its 50% of recurring revenue.

I doubt that, they will recover over the year some of the business.Companies have delayed getting rated rather than don’t want to get rated again.

2013 also post IPO CARE fell by 50% from 950 levels to 400 levels and then markets were cheering the day CRISIL bought 9.9% in CARE for Rs1600 /- “Shares of CARE surged as much as 16.8%, its maximum gain since its listing day”

Either CRISIL was clueless about how this business works or investors today are clueless about how this business works.

I tweeted my views because I am genuinely concerned about all the gaming that has happened in the ratings space. And I have been expressing those views for a long time on Twitter and elsewhere. The impact is so huge. So many people have lost money because they trusted the rating companies e.g. old people who needed the income in the debt funds.

Now we have a situation where the trust has gone. When I say gone, I mean gone are the lucrative ratings of NBFC debt raised from bond funds. I mean lucrative ratings of structured products. They have disappeared or gone down very very substantially. Why? Because people have lost tens of thousands of crores of rupees by investing in low-grade bonds or structured products which they assumed were high-grade because they trusted the AAA ratings. And now they don’t want them anymore.

6 months ago, if you went to the website of some of the rating companies and took a meaningful sample of the outstanding ratings in terms of size of debt rated, you would have found that a very large component came from NBFCs and unlisted promoter entities you have never heard of. All that business is gone. Or very substantially gone.

A ratings business has very high degree of operating leverage. The most significant cost is people cost. If business shrinks and they don’t let people go, the margins collapse. People don’t realize just how risky that makes a business model with high op lev. It’s easy to see the high ROE, zero debt, asset lightness. But when trouble comes - and it has come - op lev can really hurt.

Then there is the stigma factor. Many raters don’t want to be associated with “tainted rating companies.” So even if you are not an NBFC or a promoter entity who was shopping around for a AAA rating, but you are a conservative manufacturing company with modest amounts of debt which needs to be rated, you may not want to get it rated by a “tainted rating company” anymore. So you not only lose business from charlatans, you also lose business from the good guys.

Things were really crazy. There are only two AAA companies in the US and none of them are banks. Or NBFCs. Even BERKSHIRE HATHAWAY is not AAA! Over here in India, there were dozens in the BANKING and NBFC Space. Such has been the degree craziness on the part of some of the rating companies here.

To think that after all this has happened, the earnings of some of the aggressive ratings companies won’t fall very significantly would also be super aggressive. At least I feel so.

The only thing a rating company has is reputation. If reputation goes, earnings go. If earnings go, valuation goes. The business may survive, but it takes a long long time for things to get back to normal.

I would disagree with you that people lost 10s of thousands of dollars because of rating agencies alone. Everyone was greedy Entrepreneur, Investor, Lenders, builders and Rating agencies, Its a much deeper debate than it appears to be.

I would like to think about this unemotionally and in terms of numbers and logic. I take your point that trust is gone and no one wants to get rated by them - Let me slice & dice it numerically so that i can keep your emotions away from what objective reality going to be -

Given the regulation mentioned below lets think about where all the business will go?

non-government provident funds, superannuation funds, gratuity funds can invest in bonds issued by public financial institutions, public sector companies/banks and private sector companies only when they are dual rated (i.e. rated by at least two different credit rating agencies).

Further, such provident funds, superannuation funds, gratuity funds can invest in shares of only those companies whose debt is rated investment grade by at least two credit rating agencies on the date of such investments.

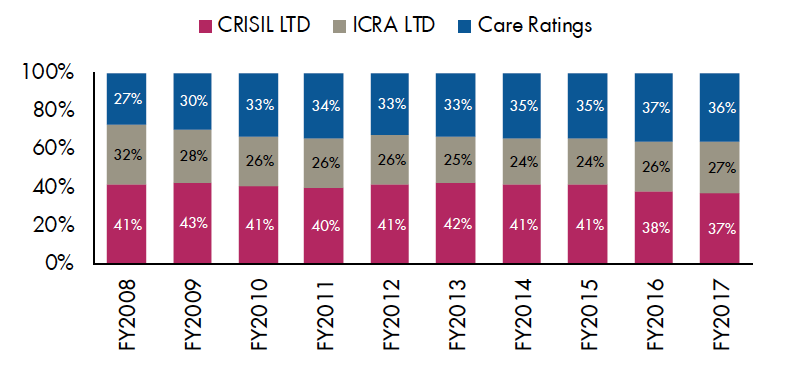

Below three rating agencies dominate the 97% of the market among them- Of that till Fy17 CARE was number 2.

So, I just find it hard to believe its all phony fake companies shopped rating market share.

Do you mean 36% of the overall rating revenue of India is phony and faked? I’ll go to website do what analysis you did but I think if you keep base in the prospective you will find it’s not all very bad. I still believe you are thinking more emotionally (bcoz people lost money) rather than bayesian. ( This homework I’ll do because whatever data I have I think Prof base is against you).

Now coming back to your original hypothesis - Nobody would want to get rated with CARE then by regulations all the ratings will be done by CRISIL & ICRA? Are they going to have a 50-50% market share? ICRA & CRISIL will be allowed to set rate whatever they want as companies have to pick two and they are the only two. I would argue markets won’t work that way and I would say why after the similar condition in U.S during 2007-09 financial crisis where everyone’s was greedy ( Not just rating agencies ) things did get back to normal.

All three rating agencies have a similar market share what they had pre-crisis. why because no one wants just 2 or 1 ( a very honest one) to dictate the prices.

and like you have the feeling all ratings were shopped, I feel the Cash (rating fee) has been delayed & there were some phony ones which are not significant.

A full-year picture will tell the truth.

I am with you on the NBFC point, There was a bubble everyone was greedy not just rating agencies. every tom, dick and harry were opening an NBFC investors were eager to put in equity, which is gone now. Unfortunately, I don’t have DATA to prove it’s indeed the major revenue contributor.

Hi, why aren’t you considering the market share gain by the other players, e.g. Fitch Ratings (India Ratings). I know CARE has the second most market share but if their market share has to go down after this fiasco and we have to keep 3 players, then there is a big chance for the 4th one in the list to gain market share.

In India, the first credit rating agency, Credit Rating and Information Services of India Limited (“CRISIL”), was set up in 1987.

A second rating agency, ICRA Limited (then known as, Investment Information and Credit Rating Agency of India Limited) (“ICRA”) was established in 1991.

Third agency, CARE, was established in 1993.

Duff and Phelps Credit Rating India (P) Limited which started its operations in 1996 was renamed Fitch Ratings India Private Limited (Fitch) in 2001 and renamed again to India Ratings and Research Private Limited in 2012.

Brickworks Ratings India Private Limited (Brickworks) began its rating business in 2008.

SME Rating Agency of India Limited (SMERA) also began its rating business in 2008.

If you see those who started early enjoying the >95% of the market share. Fitch exists from 1998 but still minuscule in terms of market share.

Similar story in U.S -

In 1909 when John Moody started to rate US railroad bonds, and subsequently utility and industrial bonds.

Poor’s Publishing Company issued its first ratings in 1916.

Standard Statistics Company issued its first ratings in 1922.

The Fitch Publishing Company issued its first ratings in 1924.

In 1941, Poor’s Publishing and Standard Statistics merged to become Standard & Poor’s Corp.

Moody, S&P and Fitch started early than anybody else they are the top three.

Now questions is why is it so ? Did they never screwed up like CARE today ? Did CARE never screwed in last 24 years ? Is it the first time their reputation in on fire ? Is it all over as prof saying for CARE ?

I have a feeling these things happen over and over again, rating agencies have unbelieve kind of moat that they survive. That’s what history suggests, for example rating agencies in U.S have completed 100 years with no impact on market share among three. Think about it why is so ? So many people lost money in AAA rated mortgage debt in U.S. but none of the rating agencies lost their shirts and pants as Prof. predicting for CARE ( has to be seen) although sounds logical.

I think Prof got a very strong point and this is the reason there is a panic selling in CARE ( but today’s lower circuit was on very low liquidity .3% of total float),

I feel there a good case to be contrarian here. A very few times consensus is wrong but when they are wrong & you are right you make lots of money.

There are very good reasons why moat is very strong for top 3 and it’s hard to displace them. Here one more example of new rating agency didn’t succeed.

My below post is not specific to CARE, but overall Indian rating industry in general. Sorry, I decided to post it here as I believe it will help everyone understand the ongoing industry dynamics since CARE is very much part of it. And also sorry for the long post.

I have always had questions on inability of Indian rating businesses to grow at decent rate which has kept me away from investing in them. End of the day, if there is no growth in equity, it will be treated like bond. Bharat Shah has nicely said that “When growth goes away, Equities reduce to a Bond. It will be Treated like a Bond for a while. If the Picture Deteriorates Further, then it will be Treated Worse than a Bond.”

In a growing country like India where you have decent number of great compounding growth businesses, I don’t understand why would one want to buy a business at 40+ PE where earnings are growing at meager 6-7%. This has been the case with all rating businesses in India in last 5-6 years. All of them were available at north of 35-40PE most of the time with earnings not growing more than 7-8%.

It is a great moated business which generates excellent ROE, throws tremendous cash flows and dividends. Just 3 players capturing 95% of the market. I believe most of us will agree that it is a great business.

If US rating agencies survived 2008 debacle, what’s happening in India is nothing compared to it. So one can have reasonable confidence in its longevity.

I believe Warren has been holding Moody’s in his Berkshire portfolio for last 30+ years. And now Berkshire would be getting 20%+ return on their initial investment as annual dividends.

My understanding is that business of rating agencies should grow at some function of growth in your debt market and underlying economy. At a high level - Moody’s revenue have grown from $349mn to $4.2bn in last 21 years at CAGR of 13% which is much faster than underlying economy growth rate of the US. This growth rate has been achieved despite of dot-com crash and 2008 financial crisis.

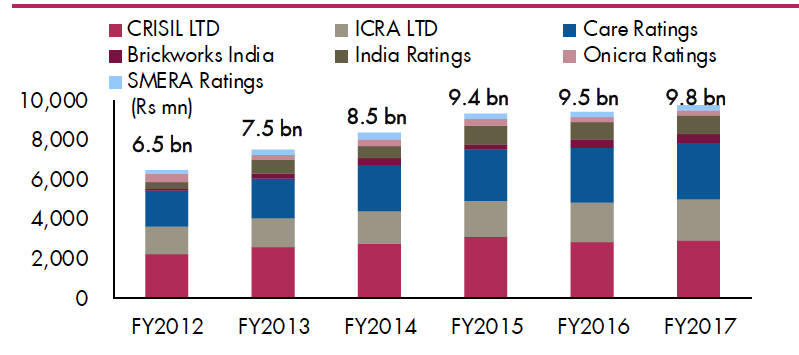

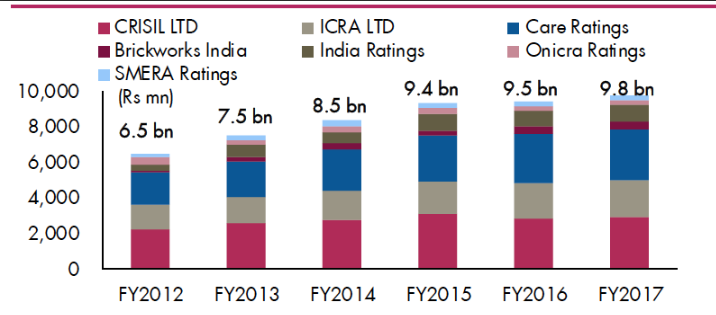

Per @AmitContrarian’s below screenshot it looks like top-line for all players have grown at CAGR of 8.56% from 2012 to 2017.

CARE’s revenue has grown at CAGR of 8.11% between FY11 to FY19. CARE’s growth is inline with the industry growth rate. But underlying nominal economy has grown at much faster rate. It is short period but still things have been flat.

With this backdrop few questions that I have are:

Is this slow growth rate in Indian rating businesses because debt markets in India are not well structured yet?

What is that structural hindrance that is causing slower growth rate for all players compared to economy growth rate? (especially in last 5-6 years)

I apologize if these items have already been covered in their Annual Reports. I admit that I have not looked beyond CARE’s AR and have not done a deep dive to find out answer for above questions. Any help with understanding above questions will be much appreciated.

Let’s ask this question: If the AAA ratings were not there on these sub-standard debt instruments, then how many of them would have been sold in the first place? In my view, very few. The malice started at the ratings companies. You see, crooked people who want to steal money from the public or aggressive people who will always try to find ways to take it “legitimately.” And so gaming in ratings was a key weapon for them.

This applies not just to the crooks but also the fools who were super aggressive in borrowing money. The cost of borrowing is linked to the quality of the rating. The high the rating, the lower the cost. And the temptation to borrow short and lend long comes from the shape of the yield curve - short term rates are almost always lower than long term rates. And borrowing short term money in very big way - tens of billions of dollars - was made possible because of those fake credit ratings I was referring to. That sort of borrowing, running into tens of billions of dollars is over.

I would use common sense here. Does ANY NBFC which has huge leverage ratios and asset liability mismatch (not all do) deserve a AAA? Why? And if they do, then why don’t we see AAA NBFCs in the US?

I really think the rating companies have used double standards and are now rationalizing by say oh this is apple and that was orange…

No I don’t

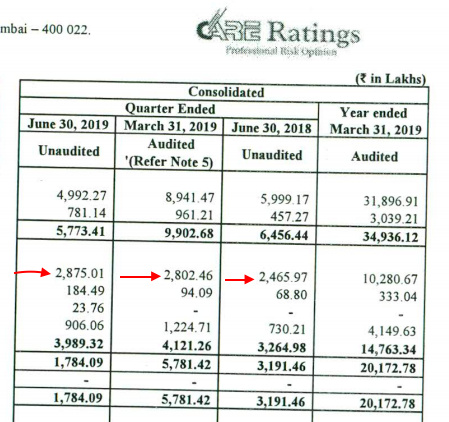

No, I didn’t claim that. All I said was look the revenues of some of these players are going to decline. Significantly. And I said look at the operating leverage. And I said that in such a business model when revenues drop, earnings drop very significantly. And I said this is an important factor in valuation. You have to treat those extra earnings as not durable. How much were extra? We will find out. Wait a few quarters. Already the number of instruments rated by CARE in Q1 of FY20 dropped by 32% as compared to the number in Q1 in FY19.

I think it’s too early to tell how bad this could become. The regulatory actions have just started. The taint has just started to take effect. And I said that this is not the time to get tempted by the idea of “scandal investing.” When you invest in scandals, it makes a lot of sense to wait for things to get really really bad so the downside risk is limited. Here, it has just started.

Nowhere did I imply that rating companies are going to die. They won’t. Or that their stocks won’t become attractive again. They will.

I just feel that it’s too premature to even know if they have become attractive. In these situations it’s easy to get anchored to percentage drop in stock price or the P/E multiple. I was warning against those dangers. Earnings will take a hit. They already are. No one knows just how back they could become. Correction: I don’t know how bad they could get, so it’s risky for ME. And it should be risky for anyone who agrees with me about not being able to predict the level of base earning power. It’s the base earning power which should be the staring point for valuation. You should start from there and then think how that would grow from that base level to even have an idea of what’s the stock worth. And at this time, I just don’t have the information to make that judgment.

Another important point. Look, these type of situations can have multiple trajectories. One trajectory is that things will bounce back and this is a great buying opportunity. I am not denying that possibility. I am merely saying that I know that’s not a certainty. I am asking you to at least consider the other possibility - the other trajectory - which is that things will get a lot lot worse before they get better. If you say well this is the bottom and that the second trajectory is impossible, and if you were right about that, then of course the stock is a buy.

But if you even consider the possibility of a very significant decimation of earning power then you must also consider the consequences of that possibility - on valuation and the likely stock price.

The fun part is that you will get to see only one of those trajectories.

And so when you make judgments under conditions of uncertainty you can’t assign probabilities as in “oh there is a 80% chance of trajectory 1 and only a 20% chance of trajectory 2 and the expected return is so and so which is so good so I will buy.” In such situations, when the ranges of outcome are so wide, using the expected return framework is akin to wading through a lake which is on average is 4 feet deep, even though the range of depth is between 2 feet and 8 feet.

In such situations you have to ask “what’s the worst case scenario?” and not give in to the temptation of thinking this is a mean reversion thing or this a wonderful over-reaction to a scandal. If the worst case scenario is bad, really bad, then you have ask these questions:

Do I have to do this at all?

Is the worst case scenario acceptable to me?

Can it cause ruin?

Can I not deal with it with a low position size in the portfolio?

Why do it now?

Why not wait to see how things unravel?

Why not wait till the downside risk is lower?

Why not wait till I get the confidence of a very low downside and then build a bigger position?

If I buy a small position, and I turn out to be right, what will it do for my portfolio?

And if it won’t do much then why do it at all?

Is it worth doing at all at this stage?

Is this for making money or just the thrill of being right in what is basically a speculative situation?

Why not wait until I can buy a bigger position when the downside risk is very low which is what investing is supposed to mean in the Grahamian sense?

And so on…

There are no right answers here. But there is a process which helps us thing through these type of situations. And I just shared a glimpse of mine.

And of course this doesn’t mean that mine is the best. All it means that mine is the best FOR ME. And it is right for me FOR NOW.

And this too could change. God, I know how much I have changed. When I tweeted about the importance of not getting tempted by the idea of “scandal investing” too soon, I was really thinking of an earlier version of ME.

Thank you so much for your wonderful insight .This really forced me to sit down and think .

A few months back a similar kind of incident happened in Facebook . It was hit hard with lot of scandals , people were really angry and concerned about the privacy , there were a few delete

FB campaign going on . Share priced dropped to 125$ from 170 - 180 $ . I had a position at 175 , i was scared and bought a small quantity around 130$ even though i was fairly confident that people will not stop using it particularly from developing countries( I regret not buying a higher quantity at lower price , even though i was really bullish on FB) . How much we Indians care about privacy . A few months later they are back in business with force and share price came to 200$.

I am not in any way suggesting Care is going to rice like FB.

All your points are very valid. But following are the questions which puzzles me

if India wants to progress isn’t bond rating a must , can India ignore bond rating for next 5-10 years ? Even if people hate CARE do they have a choice , because of the dual rated rule ?. Because of these how much will it dent their profit .

I don’t think this situation is comparable to FB. Or to Buffett’s famous Amex trade which you didn’t mention but it does come to mind when people think of scandals.

Why are they not comparable?

Because in FB and Amex, customers didn’t care. They remained loyal…

Apart from the on-going scandals, I’ve always felt that Ratings in general are currently rule-driven and not need-driven. If there was no statutory compulsion for companies to get their Debt rated, they’ll drop CRAs like a hot potato.

But… if and when complex Debt instruments like CDO^2 and so on are introduced and widely used in India, the need-based business of CRAs will sky-rocket. I don’t know when we’ll get there. However, that’s certainly a massive thing coming for CRAs in India. For reference, look at the history of CRAs in the USA.

Disc: I work in CRISIL, although not in the Ratings division.

i had invested tail coated Mohish pabarai and then increased holding to 5 % as stock fell. The logic was simple , you could get bond after tax at 7 % and bottom of credit cycle and also looking at future growth of credit market in terms of complexity of instruments in future.

Bond market in India needs to grow ( in US as they say non of top 500 companies go to Banks ) and then Large money coming to Mutual funds in Debt needs to be inevested. Plus RBI wants to develop this market .

So here are some points to think about CARE

Does it has pristine Quality : No and never against Crisil but comparable with ICRA and Fitch . ICRA is also tainted in current scandal but lets say CARE is poorer than others .

Do the payers (issuer and Lender ) wants Pres tine Quality in credit rating agencies : Absolutely not . why ?

think power of incentives - Issuer (Customer)- wants highest rating and would like a flexible credit rating agency ( CARE is only Indian company and others MNCs ). Lender - Banks /MF/PF /Insurance - All knowledgeable players know exactly how to rate borrower ( even some one who attends your one class can make out ). They dont need any thing from rating agency to make judgement on whether to invest or not. They have lot of money coming from debt and need to generate higher returns than FD after their fees . So they have to run for yield. As they cannot invest in in junk so this group is also happy if rating agencies give these junk companies a notch higher ratings (aa aaa aa-- are invented for this else we could have A (money will be returned) and D (Junk)).

Banks also need to get their book rated so that they can show lower risk to investors and RBI. Again they want some one who is flexible.

Players dont want to spend too much money on these and is only regulatory requirement which they have to use for their own benefit

Hence ratings fees are very competitive and for large customers it is not tied to amount of debt that they rate ( so large DEBT rated does not correspond to large revenue ).

Lets look at volumes of good vs bad : Companies in good is going to be very small

At Present and near future when there is mandate to have dual ratings any sensible player will have one MNC and other cheap rating agency and they can show rating which is best two

unless there is change in rating fees model , high probability that things will be same in 1 or 2 years.

Coming back to CARE questions are different than what they seems to be , i did attend conference call and asked management questions.

Is fall in revenue based on these ratings gone : Management answer no, they will do almost same revenue as last year . There is slow down in new business ( 50 % ) while 50 % of recurring business will continue.

Bigger problem is increase in expenses which no one is talking about in this thread which is much bigger problem to assumed bottom line or deciding the floor.

CARE OPM is 60 % vs 45 % Industry . This is majorly as CARE salaries are lower 40 % than peers. some one said they use less Analyst and more helpers etc . Now new Interim CEO who is rating person has got this vision to improve their products etc etc and hence he is seeing this opportunity to bridge the salary GAP. As discussed above you dont need NASA scientist to give credit rating and with so much information public and also you get reference from other credit rating agencies , i dont think you need cutting edge talent. we have enough CFAs / Finance people in India.

Salary increase of 22 % was also fine but when i asked can you pass this on and answer was no. I asked can you deliver more ( revenue increase to absorb ) again he said we need to assign minimum people per assignment . so again he could not give convincing answer.It was clear he had no plan but to get all of their salaries increased . As CARE does not have owner , investor felt they are taking us for ride.

So if CARE OPM drops to 45 % and then your Profit on like to like basis is half considering revenue will be same like last year as guided by management . They said revenue has only shifted to Q2.

So basically you cannot invest in CARE as Moated business but think of them as not so good business and look at investment operation (Graham).

Lets look at worse case

Recurring business = 150 Crs

New business = 75 Cr ( assuming 50 % gone )

Total = 225 Crs

EBIDTA of 45 % (assuming Industry std down from current 60 % )

Roughly 100 Cr PBT and 70 Cr PAT

Lets assign 10 times PE multiple . 700 cr Market value + 400 Cr of cash = 1100 Cr EV

Share price = 338

I assume 338 the stock becomes very attractive .

Some positive things can happen.

There were news that Fitch wanted to acquire big stake in CARE . It will need SEBI apporval from anything above 10 % but they can do it or set of investors change the board which is heavy LIC .

Or we convince Prof and he gets Mohinsh and others to take majority stake like Buffet in GIECO to turn CARE around .

Porf think about this idea not a bad one this may be GEICO at less than 700 cr

Prof talked about operating de-leverage playing out here that’s why Margins got hurt. Employee cost is fixed cost in these businesses and the volume of rated instrument governs your asset turnover or capacity utilization. The volume of instrument-rated has gone down resulted in a decline in margins its not a permanent phenomenon.

Can you re-check your data ? QoQ salary increased by 16% and compared to previous Q its 1%.

You have pointed out whole blame to salary for the margin decline whereas reason is this -

There was not much discussion bcoz we all agree with this because we all can see it in the numbers.

I would not value the business this way. we all can come with some number doing something similar but I think professors raised some good questions which one has to think about. as there is an opportunity cost involved if recovery not going to be V- shared and there are lot many things, then what is the upside given the risks, how future going to be, what regulators going to do, whats the quality of rating book (how much will be gone forever in due time) and what will be the long term impact of their tinted behaviour etc.

Q- Any one know how much of revenue from from BLR ? is it around 30% ?

I am saying even before you look at Revenue decline , CARE ratings salaries are less than ICRA and CARE . So Their fixed price itself is wrong if they want to have similar pay in this industry so currently it is 27 % of sales others are in 50 % range.

Revenues according to management will not decline and they will do same as last year.

So Operating leverage is even more ( double ) than assumed even without revenue decline. Revenue decline if it happens will make it worse . We need to probably also discuss if the model of paying very less salary is correct . Thats big question i am trying to analyse

BLR data is given in Annual reports it is large portion .

Please also note the rating revenue is mostly linked to number of instruments than to debt levels etc.