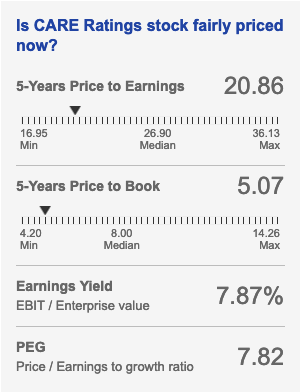

None of them trading at significant discount to their 10 year average PE …

Whats your source for 10 Year average PE?

Value Research

1 Like

Anybody saw the results?

How has rating revenue for FY19 gone down by 7.5% to ₹297 crores even when volume of debt rated has gone up by 20% from ₹16.5 lac crores to ₹20 lac crores?

Here’s a couple of points:

- Buyer power has decreased. It appears that at least a section of buyers of CARE’s services has diminished financial capabilities, namely NBFCs. The report from CARE has a mention.

- Competitors feel the same pressure. CRISIL volume has decreased 1% and profit decreased 7%, although CRISIL has a far diversified business than CARE.

So it appears that the choice for rating agencies has been to take the business at lower margins, or to forsake the business.

2 Likes

Your second point seems more valid and applicable.

I hope this moment of multiple crises for the ratings industry triggers consolidation so that this trend of price erosion is arrested.

1 Like

1 Like

So Mohnish Pabrai the so called LONG TERM INVESTOR is out of CARE rating counter …

REF # Shareholding Mar 2019.

2 Likes

I have said this before … folks need to come out of the mindset that rating agencies are god’s gift to Indian investors. It will take a while to restore confidence. I think many large lenders will have inhouse rating dept. to traingulate with what external Rating agencies are saying. This will reduce their importance further along with ongoing intense scrutiny.

2 Likes

If you go through the regulations in detail you will realize the truth is far away from your conclusion. i think best place to read the regulations is CARE Rating DRHP, lets understand that then discuss.

1 Like

Another negative development. Much needed cleanup has started seems Pabrai Inv.'s exit was perfect in hindsight.

1 Like

I brought a stock and what I saw in the next quarter … that Pabrai Inv. fund brought stake in the same company but he didn’t asked me as he had his logic.

SImilarly any investor buy or sell decision is not driven by what Pabrai does …

Now on the NEWS … These exercises are aimed to make the process even better and more relevant and not to dilute the SIGNIFICANCE of the business.

1 Like

Press Release on Grant Thornton Report.pdf (227.3 KB)

1 Like

Looks like something Mohnish Pabrai knew already

now its more cheaper, anyone has done any valuation on this ?

looking at the result looks like insiders knew its going to be pretty bad ![]()

Markets are amazing good in predicting bad result, or they know it ?

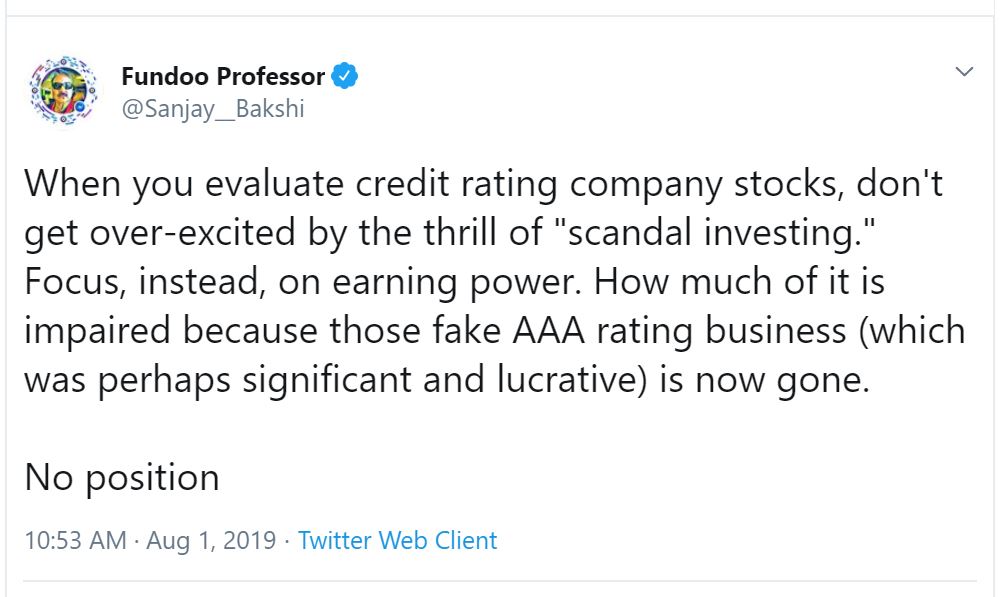

Prof Bakshi talks about the impairment of earnings due to “fake” AAA ratings.

But as far as I know, Moody’s and S&P rated many junk MBS as AAA and they suffered during the crisis. These AAA had loads of default and the subprime crisis was a result of those defaults which spread like contagion.

But these stocks (Moodys and S&P Global) rose extremely well later on. Anything different in CARE?

2 Likes

Profits and Margins are down , i think in a slowing economy that is expected . Besides that is there any red flags ? I am confused what caused the massive sell off

I agree, at the end of the day rating agencies are required, they are not going out of the business and they will recover.

On Care rating conference call. The management tried their level best to address the issue but is seen it is relatively bigger then what they can handle. From the timing of salary hike to delay in completion of surveillance resulting in delaying in revenue booking made result very weak. Also, the genuine issue of bank loan rating which decline almost by 40% in numbers compared to last years and increase Average size of instruments (which I assume has negative impact as most of large issues negotiate Fixed fees irrespective of volume or with cap on annual fees in my opinion, although management did not commented when asked on conference call).

So what May lead to revival of growth in Care

- filling the vaccum at the top level quickly (internal)

- quickly complete investigation with SEBI (external)

- Revival of growth in economy and NBFC (external)

So broadly, the growth in profit in medium term can only come from cost control given that revenue growth driver are not in control. With no promoter and full stock being float, Care rating price would continue to see volatility.

Discl: I continue to hold my position and critically evaluating the situation. The investor shall consider advise of their own investment manager. I am not recommending stock. My view may be biased and given the volatile market, I may take decision very quickly without intimating forum, considering my risk return profile.

5 Likes

Its hitting lower circuit now, Either something we don’t somebody knows. The secret exit at loss by Pabrai gives some clue.

Okay profits were down -50%, Stock correct 50% in two days. what no buyers ? Is it liquidity alone ?