Looks like we all are convinced it will go up but not sure about

when ?

how ?

and how much ?

That’s a good thing because it points towards at least one thing there will be a return of capital . but same we cannot strongly put for the Crisis hit lenders like DHFL, Yes Bank, etc.

A Crisis-hit Credit rating agency is a much more fertile hunting ground than a Crisis-hit bank or nbfc.

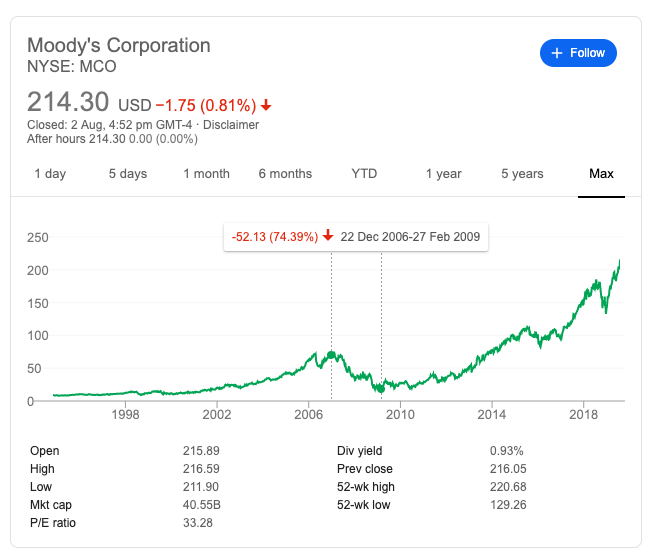

As we have a direct comparison of Lehman Brothers Vs Moody’s.

Is there a chance it may not come back because who knows what are regulators going to do? but they will not kill just CARE for what happened in IL&FS as till 2017 CARE, ICRA and CRISIL were rating them then BRICK WORKS replaced CRISIL in 2018.

For some reason, I find people more Biased towards CARE the feeling comes as if they are the most tinted but contrary to everyone’s belief I found more direct allegations towards BRICK works guys and ICRA in Grant Thornton report (https://economictimes.indiatimes.com/industry/services/consultancy-/-audit/ilfs-case-ratings-were-allegedly-doctored-by-agencies-says-grant-thornton/articleshow/70285947.cms?from=mdr).

I can say of big three CARE is clearly the least competent one but that doesn’t mean they are the most tinted one.

Whereas if you study all the big Frauds happened in history you might end up finding a correlation between Fraud with Most competent ones.

and from regulators point of view killing them all doesn’t sound like a great idea. I find it hard also to think about the scenario that we will take a very different path than the rest of the world and plan to live without rating agencies.

I think at max there will be some change in regulation, like what happened in U.S after the Crisis. The change was simple - they introduced The Dodd-Frank Act increased the liability for issuing inaccurate ratings.

I think the real Joy moment for everyone going to be when SFIO finds out individuals who took bribe from IL&FS and jail them. This will send the fear inside the spine of all the people doing wrong in CRA businesses & this fear will be good for the system rather than a stupid regulation issuers or investors pay etc.

There is a lot of debate over issuers or investors pay - You can read this nice article gives good perspective why things are the way they are http://theconversation.com/credit-ratings-old-risks-and-new-challenges-for-financial-markets-118081

Now, coming back to questions of being precisely right about -

when ?

how ?

and how much ?

Who knows, I don’t think we can find the bottom. In this business, it’s okay to be roughly right than precisely wrong.

I am more worried about being precisely wrong -

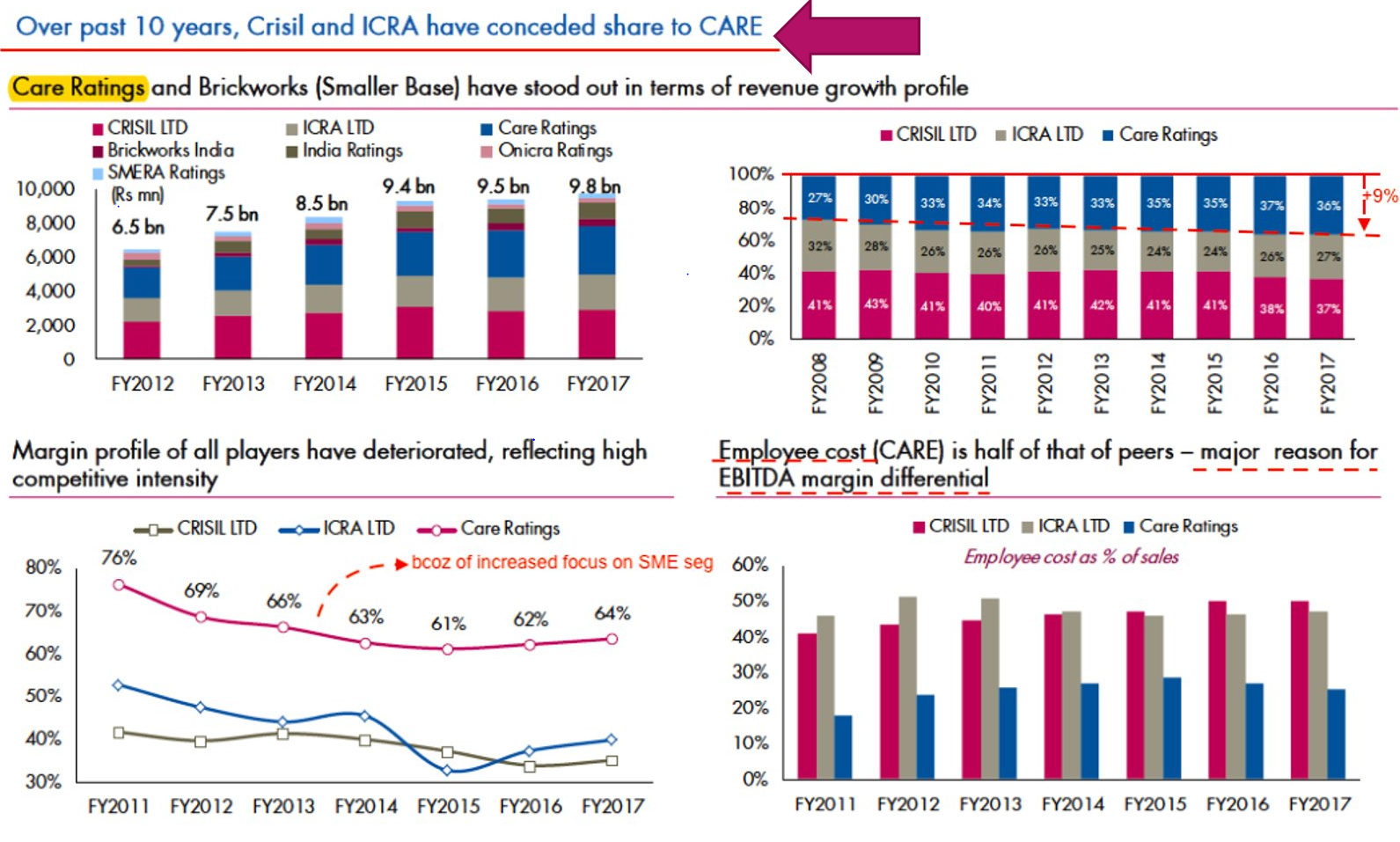

My fear is if you look at u.s the market share is dominated by big two Moody’s and S&P - 85% ( roughly equal ) and Fitch is 15%.

Over time what if that happens with CARE? Will they lose market share from 36% to 15% and lose it to CRISIL & ICRA.

Do we have data how markets share shifted in US over time ? Specifically before and after financial crisis. ( I am looking but can’t find )

I think that’s the only scenario where there will be potential risk of not making money here and i can’t think of any other reason the guys selling at lower circuit everyday potentially be worried about.

I would love to hear from them what’s their worry? anyone here trying to get out of it everyday please let know your worries.

Secondly, i strongly believe this pain going to improve the industry rather than going to kill them, there are lots of evidence pain kill banks and NBFCs not CRAs.

If someone can help here figuring out how marksahare of CRAs other countries moved over time would be very helpful.

Thanks,

Amit