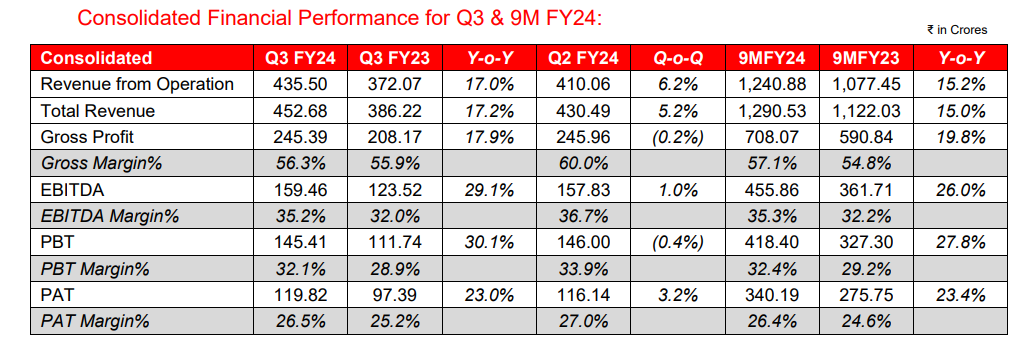

Q3FY24:

• Gross Margin for Q3 FY24 is 56.3% vs 55.9% in Q3 FY23. Operating Ebitda margins are 33% vs 29% yoy aided by new product launches across existing and new markets

• Caplin Steriles Ltd (“CSL”) 9M FY24 Operating Revenue of ₹210 Crores, a 40.3% Y-o-Y growth.

• Receivable days are at 107 days (103 qoq). Inventories (including in-transit inventory) are at ₹374 Crores (337 qoq).

Emerging Markets:

• Company targets first revenues from its own Oncology site in Q4 FY24. Company already owns 100+ product approvals across 5 markets in Central America, in Oncology segment.

• Company receives Colombia’s INVIMA approval for Caplin Steriles site. Newer markets of Mexico, Chile and Colombia expected to aid revenue growth in the coming quarters, through this approval.

• Amaris Clinical, CRO wing of Caplin Point, completes BE studies for 9 products, with a further 3 products planned for the coming Qtr.

• Company will install unique Dual-Chamber Syringe line at CP-1 facility in the coming months. The line will produce Dual-Chamber Pre-Filled Syringe products for LatAm, a segment with limited competition.

US & Regulated Markets:

• Company receives its first Otic product approval from FDA, product will be launched in Q4 FY24.

• Company files first Injectable Suspension ANDA, and also its first Plastic Vial ANDA with US FDA

• • Company has 13 ANDAs under review, with 3-4 approvals expected within coming months. Products under review are combination of Injectables in Vials, Ready-To-Use Bags and Ophthalmic products.

• Caplin Steriles USA Inc applies for 50-states licenses in US. Approval process likely to take 6-8 months, post which company will launch its own label in the US.

• Line 6 (Robotic Pre-Filled Syringes Line) undergoing qualifications and expected to be operational in 3-4 months.

• CAPEX: Almost Every capex is delayed by 1-2 quarters.

• 4 ophthalmic products approval will come in the next few months.

CONCALL:

• MEXICO: We have already filed 24 products in Mexico and received the registration of five in the recent past. We are sure of increasing our filing to at least 60 to 70 before the end of 2024.

• We have already started outsourcing dossiers from some reputed companies from China.

We have been exporting quality products directly from China to Latin America especially to the smaller markets. Now we are moving to the next level of business in the form of outsourcing from China companies for the regulated market. Here we are using our advantages and experience of catering to the markets such as U.S. which helps us to associate with bigger companies in China for our second innings in the larger markets of Latin America.

• BIOLOGICAL PRODUCTS: We also understand that there are some big companies in India which import Insulin and other biological products from China in bulk and do the fill and finish before they export to the regulated markets after conducting the necessary clinical trials. We do have plans to identify some good companies to do the same as we also have the necessary wherewithal with us in the form of CRO which has been approved by USFDA where we can conduct the clinical trials before we market the products. This will be an asset light model where we do not have to invest huge money to manufacture the biological products from the scratch

We are verifying the technical feasibility and commercial viability of fill and finish of biological products which includes Insulin.

These are things even the big companies initially used to import and test the orders and go for their own manufacturing. Of course, they are all companies which have deep pockets. We also will be in a position to do it after we test the waters by importing of Insulin and other things for which we have the necessary warehouse and then the surplus cash today.

• We are also getting into business of manufacturing double chamber PFS for the Central American markets shortly. The machinery will be installed either in March or April and the registration may take six to nine months before we hit the market. Here the volume of business may not be high, but the profitability will be very good as there is only one competitor, that too is a multinational company.

• We will also be starting one more warehouse in Guatemala border which is closer to Mexico and many of our customers feel that it is very difficult and expensive for them to come to the capital of Guatemala.

• We will continue to focus on the bottom of the pyramid and also the bottom of the business pyramid where the traffic for competition is always lesser.

• API FACILITY AND ITS DELAY: It is also true that we have been delaying the general API facility in Vizag as we are looking for some niche products other than our own injectable API for captive consumption. Finally, we have appointed an API expert who has filed 10 DMF for some niche products and he has joined with his team recently. We will now focus on the completion of Vizag API at the earliest.

General API we wanted to complete it for the captive consumption. Later we have found out that there is an opportunity for us to add some more and that too we were looking for a niche product which of course we have found a person as I told you before so now that it will be speeded up and it is true it was delayed that is the reason, I mentioned in course of my speech also. Coming to Onco API we thought of doing it in the existing facility and we have been told by our head of project that we could do it there but later we felt it will not be that viable in the sense this is a product API you need more land. When you expand at a later date, we will not be in a position to accommodate the API there so now what we have done is we have bought land in the form of 18.5 acres in an industrial estate at Thervoy Kandigai that is why we have decided to start it and we are going to start it now and we will be able to complete it in the next nine to ten months’ time from now.

• “Now let me come to the important area of my focus for the last two to two and a half year of managing the CSL Facility to make it very unique. My stay in the factory initially and the subsequent stay closer to the factory made me to understand the importance of perfection for integrity, quality and safety in addition to improvements in productivity. I personally went to the shop floor areas many times in the day and night to find out some disobedient minds whom I removed them later. I went to start this factory next to my village only to help the poor not to become a poor. I also learnt that bottom-up approach which helps the company to reduce the deviations and OAS which are very important for any pharmaceutical company and needless to say it is pertinent to a USFDA facility.” – C.C Partheeban

• CAPLIN STERILES: We have around 14 products that are under active review with FDA and we expect most of these to be approved within the next 12 months. Some of these are ophthalmic products which we have a line that is largely underutilized at the facility so we will be aiming at launching these products as close to the approval date as possible. We will also shortly be working on a pipeline of prefill syringe products as well so you can imagine that we are trying to cover a broad spectrum of products that are used in hospital and clinical settings. This will certainly be augmented when some of our Oncology injectables start to feature in the coming years onwards.

We have also filed several products in Mexico, Canada, South Africa, Australia, etc., and we can start to see some non-US based revenue within the coming 18 months so overall we are making good progress on the US side and with prices stabilizing and also injectable shortages continuing, we feel that our razor-sharp focus on digitalization and quality and supply continuity at Caplin Steriles will certainly augment the company’s progress in the years going forward.

• US FRONT END: In the next eight months, we will have licenses to distribute our products on our own label in all 50 states in the US. We hope to launch around six to seven products in the initial period within the first year itself and as Chairman was saying we are going to be attending more and more expos in the US trying to identify the underinsured and uninsured population which we believe is anywhere between 30% to 35% at this point and these pretty much belong to the tier two and tier three cities and also tier two and tier three buyers of the US which is what our focus has always been on including in Latin America. This also will not have any impact on our current business partnerships in the US which is more of a B2B model because our partners are much larger in size and they are much more focused towards the GPO related business.

• 55-56% will be normalized gross margins.

• Red Sea issues will not have any major impact to us – Shifted to CIF from FOB Basis – pooling all goods together and then moving them by road through Guatemala warehouse

• LATIN AMERICA GROWTH: Actually, the growth has been about close to 11% in the conventional business. I am sorry to differ with you that we have saturated in Central America and Latin America but again definitely we will do well once we enter into the bigger geographies of South America like Mexico, Brazil, Chile, Colombia and all but these countries as you know well it takes time to complete the registrations and then these are countries where you will not be in a position to do big business with 10 to 12 products. We have to have different buckets in one big basket which is going to happen say one year or two years from now. That is the time we will do again extraordinarily good business the way you ask

In the next two to three years, we will have all the facilities and then second maximum registrations will be completed in majority of the countries in the next three to five years

One more thing in the form of LATAM, I am sure in five to six years from now we will be the number one company. In all humility I can claim that we can do it. The reason being in the smaller geographies where all these six countries put together the population is less than Tamil Nadu. We are doing close to Rs. 1,000 Crores. Once we get into the bigger geographies as I told you in the years to come, we will be the best of the best business and we are sure of becoming number one also in these countries. These are the few things I would like to convey to prove that we are a force to reckon with in the years to come.

• Caplin sterile capacity expansion: Now with line five that has come into place we actually have expanded the capacity by more than double so we are actually good till about I would say next four to five years at least.

• Now like with all of these approvals coming through we are starting to get more and more visible in the US which is why I think it is at very good time for us to launch our own label in the US and one of the three largest distributors in the US has already tied up with us on about five products now and we are in active discussions to create a private label for them for another four to five products also so it is again in the nascent stages and we see that there is a certain level of disruption that is happening in the US also with certain companies and then making deals directly with manufacturers and stuff so we think that there is going to be more opportunities in that direction and we do not want to confine ourselves to the GPO space or the CMO space or anything like that. We want to be open to all ideas and so far, so good we will be patiently cautious about what we want to do in the US.