Stock Story - Capital Trust

Capital Trust is a NBFC registered with RBI engaged in providing loans to SME sector in India. Average lending rate revolves around 36% and the average borrowing rate comes to around 16-18%. Company has its main markets in Uttarakhand and western areas of Uttar Pradesh. This segment of lending does not have the capping regulations as are applicable in case of MFIs by RBI. We do not even see such capping limits to come in near future, simple reason being SME segment being a comparatively risky sector where typical loan amount ranges from 2 lacs to 6 lacs, wherein the loan amounts in MFI sector are very less (around 15000) and are sourced through JLG model (which poses less risk for lending firms). Hence, the current ROA of the business which is 9% will be sustainable in future.

27th January -

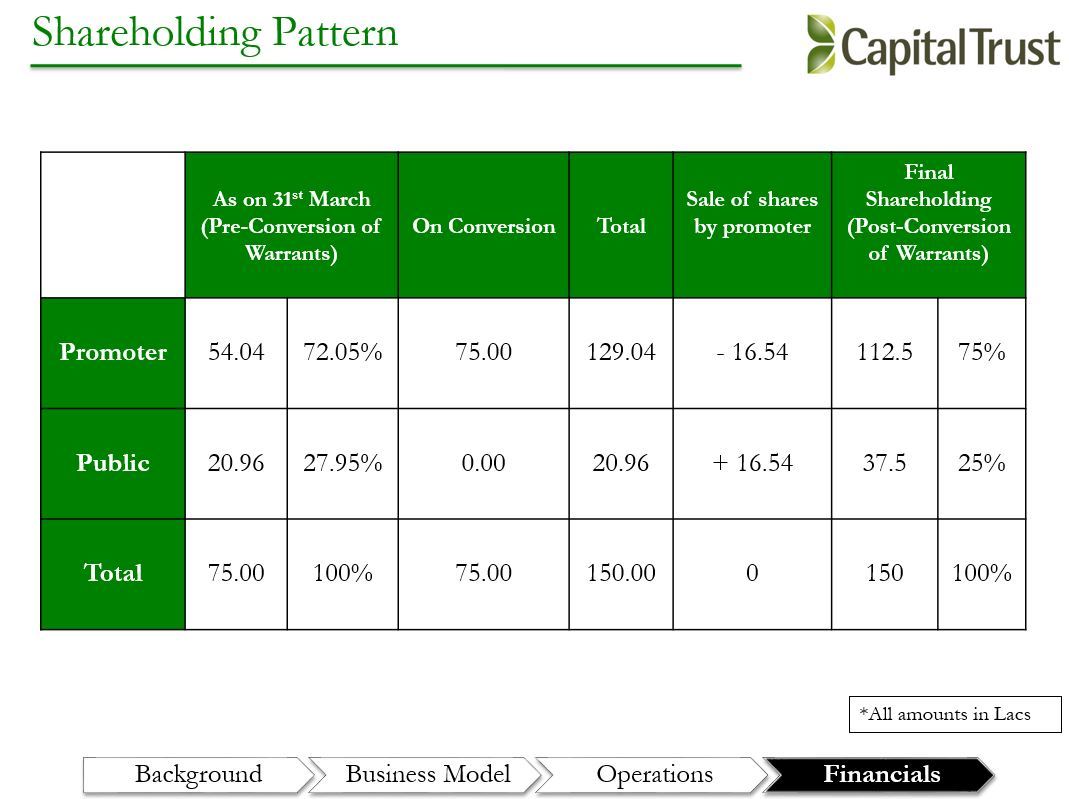

Mr. Yogen Khosla applied for 75 lacs warrants in the company. Total number of shares in the company at that time were also 75 lacs. So, 100% dilution.

22nd May -

Board of directors approves allotment of 75 lacs warrants to him at 117rs (price is based on SEBI formula). CMP on 22nd May was 200rs. Please do not compare between 200 and 117 and come to the conclusion that there is a corporate governance issue. The price of 117 is based on SEBI formula. Promoter was lucky that the stock moved up. Stock could have moved down also. Also, we should note that the FY 15 results were declared between this time (January and May) and the company posted excellent result. Stock should have ran up due to the fundamental growth.

27th July -

10 lacs warrants converted to equity shares at 117rs. Till now promoter held 52.90 lacs shares out of the total shares of 75 lacs giving him 70.53% ownership. After 10 lacs shares more his holding increases to 74%. As per SEBI any purchase of shares (either by dilution or by issuing new equity shares) of more than 5% of the total equity capital will have to be executed by open offer. 10lacs on 75 lacs is 13.33%. Promoter holds now 52.90+10 = 62.90 lacs shares out of the total capital of 85lacs. Promoter forgets to make the open offer. Coming back to this later.

In September -

Promoter sold 3.02 lac shares via block deal (I guess). This was to comply with the SEBI guidelines of maintaining promoter holding 75% or less than that. He had to sell these shares (even though his holding was below 75%) so that he can convert warrants at a later date. Now Promoter holding is 70.44% ((62.90-3.02)/85*100).

28th March -

Company converts another tranche of warrants of 32.90 lacs shares at 117rs. Also, 30.75 lacs shares issued to non promoters at 217rs. Total Equity shares on this date is 85lacs+ 30.75+ 32.90 = 148.65 lacs shares. Out of this promoter holds 92.78 lacs shares. Promoter Holding is 62.41%.

29th March -

Coming back to the open offer not done at the time of 1st warrant conversion of 10lacs shares. Management decided to convert another tranche of warrants on 28th March so that both the warrants come in the same financial year and as per SEBI guidelines promoters will have to only make one open offer. In this case, since the price of the stock is well above 263 rs (the open offer price), the open offer shall stand canceled. Promoter holding remains same.

Story to come in -

7th June -

Open offer closes and the result will be the same.

Before November -

Promoter will have to convert the last tranche of warrants of 34.7 lac shares . Again this will trigger open offer since promoter will be acquiring another 23.34% of the total equity shares in the company. Total equity shares will stand at 148.65+34.7 = 183.35 lac shares. Of this promoter holding would be 92.78+34.7 = 127.48 lac shares. Promoter’s holding will be 69.52%.

During the same period -

Open offer will be made. Now will it be exercised by the existing shareholders again depends on the CMP of the stock at that time.

Conclusion - Dilution is not always bad. Good and Bad depends on the terms of dilution. If the promoter issues warrants at a Price/Book ratio of more than 1, then the dilution is beneficial for the existing shareholders of the company. Promoter issued warrants to themselves at 4.68 price to book which is good for the shareholders. Combined with that the SEBI guidelines also protect the shareholders. If I were standing at the warrants issue date, I would think rather opposite - promoter is going to sell a huge stake in market through block deals (due to this shareholding exceeding 75%) which will bring downward pressure on the stock price. At that time QIP plans were not at all there. If QIP were not there, promoter’s holding would be definitely above 75% which would trigger stock selling by him. It was a probability game. It was fortunate that QIP came and promoter did not have to sell his stake. So, promoter got just lucky here. He is able to convert his warrants at 117 when the market price is 380. There are no corporate governance issues in this entire story. If no one gives you capital in your business, you need to infuse yourself to grow. Dilution is very common and it is not always bad.

Moreover, this is a green flag that light house is one of the QIPs. Light house is known for its due diligence before investing a penny in a business. This guarantees the management quality.

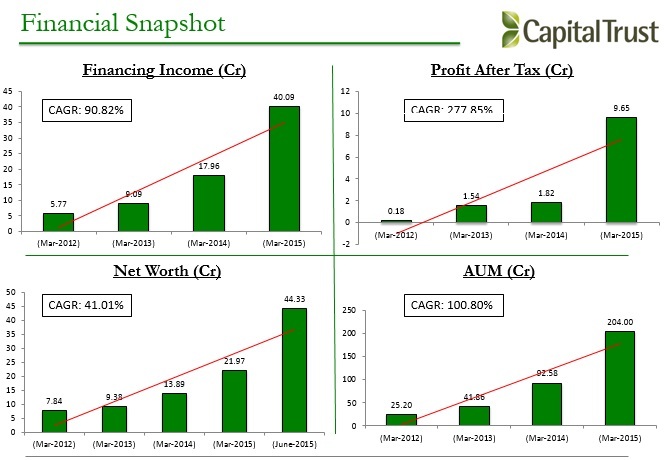

Business is just superb, borrow at 16% and lend at 36% generating a phenomenal ROA of 9%. Which financial sector company generates 9% ROA. Even MFIs generate 5%. Top banks generate 2%.

RBI regulations on interest rate cap for MFIs will not be replicated in this model because of its inherent risk. There is less competition in this segment. Equitas is one such company which is engaged in lending to SME segment also. But they plan to cater to west and south markets only. North is open for capital trust and the market is huge.

We should closely track this company. I take back my previous comments where I expressed my negative views.

Valuations -

Equity shares as on 30th sept, 2015 - 85 lacs.

addition in equity shares - 32.90 lacs (warrant conversion) + 30.75 lacs (QIP).

Total Equity shares - 148.65 lacs shares.

Total Equity Capital - 1486.5 lacs or 14.865 cr.

Preference shares have been paid off (check asset/liability status on 30th sept 2015 as released by the company). 18% fixed cost savings.

Money received against share warrants will be reduced to (190125000 - 92531250) = 97593750 rs. Calc - (32.90 lac shares/ (32.90+ 34.70 lac shares))*100.

Historical Debt - Equity ratio has been 4 +.

Assuming growth rate of 160% (calc based on 9 months results - profit of 14.07 cr for 9 months is 120% growth in reserves); reserves at the end should be close to 17.6 cr + 11.47 cr = 29.07 cr.

Securities premium should be added to the reserves earned on conversion of warrants and issue to QIP. Total premium on warrants will be 32.90 lac shares * 107 = 35.20 cr.

Total premium on QIP will be 30.75 lac shares * 207 = 63.65 cr.

Total premium added will be 98.85 cr.

Total reserves and surplus estimated is 98.85 cr + 17.6 cr + 11.47cr (beginning value) + (30.61-11.47-8.56) = 10.70 cr of premium already included in reserves and surplus on conversion of 10 lac warrants (10 lac shares * 107). Total reserves has to be close to 138.62 cr.

Total book value at the end of the financial year will be 138.62 cr + 14.86 cr + 9.75cr (application money recd.)= 163.23 cr.

Book value per share - 163.23 cr / 1.4865 cr shares = 109.84 per share.

CMP is 380 rs.

Price to book is 3.46 times.

Assuming debt equity of constant 4 +.

A stock with 9% ROA and 50% + ROE with negligible NPAs and excellent business dynamics. Should this stock be purchased at a P/BV of 3.46 times is the question.

Filters -

Good mgmt - Yes, ex-RBI (chairman i guess) on board and no red flag against the mgmt.

Growth - Yes, huge market.

Longevity of growth - Yes, for next 3-4 years at least.

Business quality - Least competition and high return ratios. Operating in UP and Uttarakhand areas is not easy with such low NPAs.

Valuations - Dont know whether they are cheap or expensive. Please someone help here.

Disc - Not yet invested. Just digging and digging and want to be completely sure before investing. But, yes I like this stock now. Please do your own diligence. Also do correct me if there is a mistake anywhere in my calculations and understanding.