We’re very aggressive because we want to serve new clients and hold on to existing customers

Salaried vs non-salaried has changed from 73:27 to 83:17 in Q4 FY21. Girish Kousgi says this is due to the pentup demand

Sees challenges in collection in this quarter

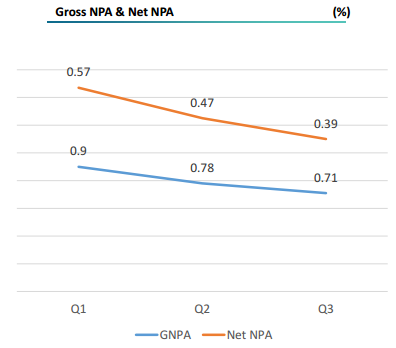

GNPA in Q3 was 0.68 (pro-forma was 0.99 which is now reduced to 0.91)

Our customer profile is such that there might be delays but no defaults

Sees no challenges in disbursement

Average ticket size in Q4 is up from 18 lakhs to 20 lakhs; have changed the strategy for salaried customers where we are now giving loans upto to one crore which wasn’t the case before. No change in strategy for non-salaried segment

Hii folks,

[short Introduction] This is my first post on value pickr. First of all, I thanks all the collaborators and moderators for creating such a beautiful platform and enlighting us with their thorough knowledge in markets. I was bit underconfident to post on value pickr due to fear of criticism, In that thought never push myself to contribute but now I feel I can only learn when I post and get feedback for the same. I will try to contribute as much as I can. I am just a learner and been into markets since 6 years. I was been more into trading in my initial days but since 2 years I am sincere about investing and it parameters.

I have written a short analysis on Canfin homes, please give a read. Please add any data points I should look into to have a crystal clear view and remove my biases for the same.

In the current market where lots of stocks are grossly expensive on traditional parameters, Canfin Homes is one company which is priced reasonably.

With NPA worries (almost) behind us and Canfin Homes’ GNPA just at 0.90% in Q1FY22, which has reduced from 0.99% in Q3FY21, downside risk is limited in my opinion.

I believe the company can start showing growth from this Q2FY22 onwards. Confidence comes from the fact that they disbursed 2000 crores of loans in Q4FY21 when COVID impact was minimal.

Notes from last two conf calls is available below -

Conf Call Q4FY21:

In new disbursements, salaried portion went up to 83% and 17% was SENP. This is because of the recovery time for SENP from COVID with respect to business loss would be slightly longer.

DSA sourcing would be in that ratio only 50-50, maybe, plus, or minus 3-4%. There are three-four things; one is if you see the portfolio performance of DSA source and non-DSA source, there is no difference for us that is because our DSA model is different as far as DSA model would work only with respect to lead generation or just closing the file.

Once the file is closed, we take over the entire case and we own the customer, we own the entire process right from the processing right till disbursement whereas if you typically see how it happens in the markets the DSA would source, complete the enrolment process, would be part of the entire processing, sanction process then documentation, till disbursements.

So our model is different to that extent even our payout to DSAs is much lower than what the market pays and therefore we are not really too worried about DSA proportion either increasing or decreasing as long as we are able to do numbers and portfolio being intact.

Karnataka would be in the range of about 20% or 21%. Total South India contributes about 70%.

Whatever CP raise is not for funding but for the cost leverage, the same is supported by the undrawn documented financial lines available with us.

The cost of funds for raising debentures was either quite high. Till last year we had an option of not raising but however from this year onwards we have to raise 25% of the incremental borrowing so from this year we will raise.

Why we could not raise last two years is that purely because of cost so this year we have to raise even though it will come at a slightly higher cost.

Now as far as CP I want to stress CP is raised only if you have a backup of undrawn limits so CP is used only for cost reduction purpose, not for lending. We do not raise CP and lend because we are very high on liquidity.

As of now we are covered for the next seven to eight months and at any given point in time we will have 7 to 8 months of liquidity. During COVID time we had one year or now we are at about 7 to 8 months we are very high on liquidity and therefore since we have huge undrawn limits, we try to reduce the cost by raising CPs.

The yield on all advances is 9.49%. NIM is 3.69%. Incremental cost of funds in Q4 is 4.5% and incremental yield is 7.32%.

We used to be in the range of Rs 250 crores Balance Transfer out. There was only Balance Transfer out during COVID time that number for Q4 is 90 crores. So two things have happened if you have to compare that with the business, what you have generated, if it will be approximately 90 on 2000. Earlier it used to be 250, so BT out has substantially come down. It has helped us to retain our customers and also grow our disbursements.

Today we are able to probably try and fund to a customer who wants to buy from Cat A builder, which probably was not possible four quarters back.

Pricing strategy is invoked last year about five months. So we did start it in the month of November till March, it is about five months. So if you see the impact actually for the first one year or so for the impact in margin contraction will be largely from the repricing out of the portfolio than incremental business.

So what will happen after one year because if you look at any company, 80% of portfolio would be last three years sourcing, so at a portfolio level, we are at about 22% of the portfolio repriced.

Assuming that we feel that in the next year or so I think it should get back to the situation which was pre-COVID, so if that happens then we will get back to our earlier way of doing business, maybe the gap will not be that much assuming that it may take a little longer time.

Most of the bank loans are linked to MCLR, so whenever the bank changes MCLR, there is an impact on our portfolio with respect to rate either going up or going down, but all the loans are long term.

Some banks use 1 month MCLR, while some use 3 month MCLR. Our effort is to ensure that all the banks move to one month MCLR, but I think some banks have their internal policy and therefore the three months MCLR itself would be quite less which can be comparable with certain bank one month MCLR.

We are actually agnostic with respect to whether it is one month or three months, we are worried about the landing cost. As long as it fits into our cost strategy, we are okay with that.

Our portfolio cost of funds was in the range of 8%, now it is 6.87%. Incremental cost of borrowing is 4.5%. So we have repriced most of the loans.

Our incremental loan rate is now at 6.95% and we have increased the rates in April now to 7.25%. We have roughly increased the rates from April onwards, so if you look at last two quarters it was an offer.

So our rack was different and behind a knock of our limited period and therefore that would have an impact on the margins for one year and then it will get repriced to the rack rate.

We want to grow 20%+. It all depends on COVID second wave. Otherwise our growth plan is intact and as far as margins have already indicated, we will protect 3% and 2.4%.

Our average ticket size has gone up to Rs 20 lakhs from 18 lakhs, because we are now focusing on few other segments which will help us to grow our book much faster without taking any incremental risk.

Some of the customers would come forward to reprice their loans, some of the customers the repricing happen automatically because we have both the options. So just to answer the question this happened over a period of time, it will not happen in a span of two or three months’ time. It will happen over a period of time, but eventually I think most of the portfolios will get repriced. In the meanwhile if the rate goes up then the repricing may not happen or if the rate goes up substantially it can happen on the higher side, because we also reduced the portfolio in a rate of all the customers at a portfolio level.

Our salaried customers from private and government background have average income of Rs 40000 to Rs 42000 per month.

Basically if the difference in rate is upto 0.4% or 0.5% customers would not do BT out, so once the rate crosses point high that is when customers would do.

This growth strategy that has nothing to do with stake sale.

Our GNPA in Q3 was 0.99%. It has come down to 0.91% now.

Salary will be assessed based on documented income. So we take pay slips, we take bank statements, we take IDR. As far as non-salaried is concerned, we go by only declared income.

Conf Call Q3FY21:

With respect to demand, demand is completely back in the affordable space both in builder and non-builder segment.

What happened was immediately after COVID since business was not completely back and there was no opportunity in corporate and SME space, so lots of banks, especially PSU banks started focusing on retail so that put lot of pressure on NBFCs and HFCs which were holding book at a much higher yield. So that was the threat and therefore we changed our strategy, this was about I think three months back. If you have seen historically our pricing strategy, this was about I think three months back.

If you have seen historically our pricing would have been 150 bps higher than the best HFC in the country or any best PSU or other private bank. So now we took this decision of trying to reprice the book which we would have other ways lost to competition.

We will raise capital because today our DER is 7.3 which is low and CAR is 24. So at this point in time I do not think there is a need, but whenever there is a need definitely we will raise capital and keep this under check well within whatever gets prescribed by the RBI once the discussion gets over.

From this quarter onwards we will be able to grow at the normal growth rate so I think in next six to eight quarters time you would see the growth of about 17%-18% on both book and loan disbursements.

Lots of banks come forward to try and offer us new products which would bring down cost.

The potential from existing number of branches is immense. So we can grow our book at least by another 50%, 60% with existing number of branches.

Focus of all these banks will tilt from retail (especially mortgage) to SME and corporates because growing a corporate book or SME book is now much faster and better for a bank compared to mortgage, then you would not have that kind of competition which you have seen today.

So once they reach that position then we will play accordingly on pricing.

Collection efficiency is 93%. It means out of 100 customers 93 customers pay up and the balance 7 customers will default and subsequently pay up. Some will pay up and some will move buckets.

Average age of our customers is 35 to 37 years.

In case divestment happens there could be increase in cost of funds by 25 bps that we can easily manage in our pricing.

We are in a sweet spot. We may not have the advantage what bank would enjoy but you also do not have the disadvantage of what many HFCs would have on the cost and so we are in a sweet spot. We are able to by available in places in geographies where banks are not there and now there since our yields are going to be much lower than the average HFC yield so we are in a better position to do business in these pockets at a yield much higher than bank yield.

Higher the income, higher the FOIR. Lower the income, lower the FOIR. It starts from 50 and goes up to 65.

The customer profile on the self employed is small traders and somebody who is into manufacturing or services. Their income per month could be in the range of Rs 50000 to Rs 60000.

80% of our disbursements in last three months and some conversions will be at 6.95% yield. Roughly 10% to 11% of portfolio will be at 6.95% yield, lowest rate.

Management stated that Salaried portion of Total Loan Book went up because of the recovery time for self-employed non-professional from COVID with respect to business loss would be slightly longer.

Direct selling agent or DSA sourcing would be in that ratio only 50-50, maybe, plus, or minus 3%-4%.

Management also said that as of March end, Company raise 19% commercial papers as the backup and CP is more for arbitrage with respect to cost and not is for funding.

As per the Management, lockdown in almost every State in the Country will impact the Business and Collection of the Company.

Management also stated that the company has planned to add about 18-20 Branches this year.

Wonderful analysis of Canfin with Management by Digant Haria & Omkara

Some Key Prospects discussed are: 1) What is a housing finance company? 2) Management & organizational structure of Can Fin Homes? 3) What makes Can Fin Homes unique? 4) How is Can Fin Homes different from HDFC ltd and Aavas? 5) Growth outlook of Can Fin Homes?

Quarterly disbursement (2200 cr.) growth is back (10% growth over Q4FY21)

NIMs have started improving from 3.31% in Q1FY22 to 3.4% in Q2FY22 and this should go up going forward. PAT and revenue will also start growing going forward

The results are good. They have started growing again at a reasonable pace now, however at a cost of margin. Their loan book is getting close to 30k Cr, they are able to maintain quality, and transparency. They come very open if you listen to the concall. Many housing finances have busted. But Canfin has managed to maintain quality. They aren’t as aggressive as you hope them to be, they are incrementally building it. The new CEO took a while, but might have figured a long term play book. It would be nice to hear from their recent customers, if there are any in Valuepickr. This might start turning out to be secular long-term play

If you check carefully, only standard provisioning has increased big time and that is bound to happen when you grow fast. I think this elevated standard provisioning will come in each quarter. Will wait for conference call.

Does any of you feel that canfin is max out with very limited upside. They are already at 8x leverage and are doing 16% ROE. This year they showed 20% loan book growth with the help of increasing leverage from 7.4 to 8 yoy. If they want to grow their loan book at much higher percentage than their ROE, except increasing their yield, they can decrease their cost of funds/increase their leverage/improve their operating leverage/improve asset quality.

Decrease in Cost of funds: with current cost at 5.56%, there is no way it can go further down.

Increase in leverage: Already at 8.04, may be they can reach 9, beyond that if one unexpected environment happens, company will be in very bad state.

improve their operating leverage: cost to income already goes below 20%, not much to extract here.

improve asset quality: again GNPA 0.64, cannot expect more.

From my view company is already doing great in all metrics, so they cannot extract anything from here to improve their ROE and now when you consider this dividend also, does company can grow more than 15% on sustainable basis if they did not change borrower profile.

Growth with capital raise is always possible, but that growth does not reflect to existing shareholders. My point, is this the peak potential of canfin in it current form

As a thumb rule if a financial institution is growing more than it’s ROE then it needs to raise equity in order to borrow more at the same debt to equity ratio.

In Q4FY22 their latest ROE was 16% on annualized basis. So given they keep the debt to equity same they can grow at 16%. If they raise the debt to equity they can grow more. So 15-16% we should hope for.

Listened to the concall transcript. They are guiding for a growth of 18-20% for FY23. They are comfortable at a Debt to equity ratio of 8.5. So for existing shareholders if they increase the DER to 8.5 and at a ROE of 16% with the robust demand environment 18-20% growth is quite achievable.

They are also authorised to raise 1000 cr equity. They will raise in tranches.