I think this is very sensible, responsible and ethical. https://www.bseindia.com/xml-data/corpfiling/AttachLive/c56d71d4-bc86-40c0-8250-51561fc2edca.pdf

Housing finance business is a marathon, everyone getting through this safely is a greater good.

On the business side, how will defaults affect, and what is the extent of defaults? Looks like the company has adequate liquidity.

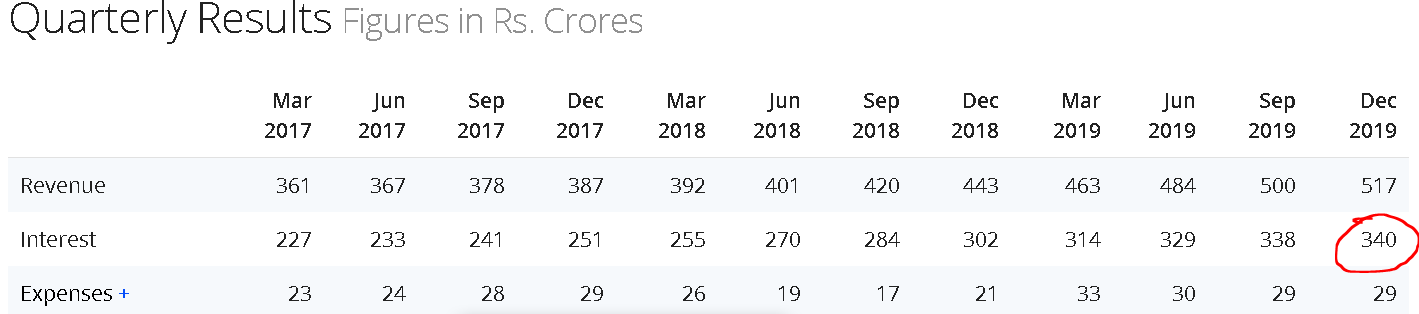

Quarterly interest burden is around 340-345 cr.

I think they will have regular principal payment, how do we get those nos to make sure they will get through this?

If they do a good job, they can emerge stronger, considering whats going on with, PNB housing, Indiabulls Housing, Dewan Housing, Repco.

Would anyone be able to make some estimation of how their payments are lined up and can they manage with current liquidity of Rs3500Cr and collections?

Hi @ayushmit Mittal, do you still have position in Canfin Homes?

I listened to CEO speaking to Bloomberg and CNBC, he felt very comfortable about their liquidity and collections but was skeptical about the defaults in the short term had cautionary note.

With the current business environment and some HFCs already having their own issues (PNB housing, Indiabulls Housing, Repco, Dewan) also Gruh (which I thought as a stronger player and a competitor of similar size and model) under the control of Bandhan, do you see a landscape where this could emerge as a stronger player in the future and increase market share?

They have a good history in underwriting thats fairly low risk and conservative but can they build on it and scale up? Your thought would be appreciated if you hold or track.

In general, CanFin caters for salaried sector. They dont take risks. So, if you want a steady loan house you could look at it. But personally don’t think this sector itself is good to be in for next 6-24 months.

There are lot of job cuts & job loss happening. I really doubt people will have that hunger to get into debt if they have an inkling of fear on their job prospects.

We know housing sector is going to get impacted due to COVID breakout, obviously Canfin homes too. I am trying to ascertain and refer an research report on housing demand vs market share of housing finance companies for the next 3-5 years. Pls share if anyone of you have done this or any publicly available reports. May be if we have any aligned report on canfin homes, that would be an additional help. thank you.

Loan book: Increased by 13% with an Outstanding of Rs.20708 crore on 31/03/2020 as against 18381 crore on 31/03/2019.

Revenue: The total income of the Company increased by 14% from Rs 463 Cr to Rs 529 Cr(YOY). An increase of 17% was seen in the total income when compared to YTD with an increase from Rs 1731 Cr to Rs 2030 crs

PAT has Increased from Rs 67 cr to Rs 91 Cr YOY @ 36%. PAT for FY 2019-20 stood at Rs 376 Cr as against Rs 297 cc for the previous year, an increase of 27%.

Net Interest Income: Nil has increased from Rs 138 Cr to Rs 186 Cr YOY a growth rate of 35%. For the Year the NII has increased by 24% from Rs 544 Cr to Rs 675 Cr.

NIM has improved from 3.29% to 3.52%

Asset quality: The GNPAs of the Company has been contained at 0.76% as compared to 0.80% in Q3.

Impact on Liquidity and debt servicing:

Company’s liquidity position is good and has sufficient un-availed sanctioned limits lined

up from Banks and has not opted for moratorium offered by its lending institutions

Notes on Covid impact: On operations: The Company is fully operational from April 20th with necessary precautions for the safety of employees and customers.

On Capital & Financial Resources: The Company is well capitalised and there is no impact on the Company’s capital and financial resources.

On Moratorium: Collection of EMIs in about 28% of the accounts have been postponed due to moratorium offered to borrowers as per RBI guidelines

On Profitability: From 24th March till third week of May, lending was impacted. However, impact on

revenues has been minimum.

On Liquidity and debt servicing: The Company has enough liquidity and sufficient unavailed

sanctioned limits from banks and financial institutions to meet all obligations and business growth

Does anyone has any idea why is Canfin homes delaying its board meeting for Q1 results again and again…atleast 3 changes…surprising for a company of canfin type company to do this

Lower fee income implies that loan disbursal was quite less in this quarter as expected

High provisions are surprising for me given the company caters largely to salaried segment.

What I would be looking for?

Liquidity position of the company. With ROE excess of 20% and loan growth to be 14-15%, I don’t want company to raise more capital given the valuations are also not excessive,

Management commentary on sources of NPAs along with loans under moratorium.

Disc. Not invested but keenly waiting for management commentary to invest.

AGM Notes:

(Missed MD’s address but listened Q&A as I joined the call little late)

Focus on 4 pillars: Liquidity, asset quality, growth and profitability

Disbursements guidance: will try to get close to last year number

Provided higher provision in Q4 FY20 and Q1 more than RBI mandate for future ready

Lower business per employee/branch: Increased manpower in last 2 years anticipating growth and new branches so business per employee and branch gone down little bit, will improve once the demand picks up

Covid handling: Entire team worked from home till April end and managed most of things like follow ups and offering moratorium etc.

Started business in last week of May and June wherever opportunities available

Planning to maintain same mix of housing vs non housing

Will try to maintain or increase market share once demand picks up

Mostly focussed on affordable housing and tier 3-4 cities, so not much tie-ups with big builders

Demand is coming back slowly and expecting over next 2-3 quarters will get back to normal

Disclosure: Invested - Do not recommend buy or sell. Not an investment advisor and Investors are advised to do their own due diligence.

Started with operating 50% of the branches in April, almost all branches were open by May end

Demand level is currently 65% of earlier levels

Internal target is to disburse 5k crs and reach 23k crs loan book in FY21 but can not give this as guidance as not sure how the situation will pan out

C/I reduction is due to Covid and it will come back to normal range soon

NIM: Will be difficult to maintain NIM 3.7% but will try to keep it above 3% and spread ~2.4%

98% of the process is automated, cash collection is only for delinquent accounts otherwise fully electronic mode

NPA:

Expecting NPA to increase in Q3 and Q4 but will be lower than industry, GNPA to come back to Q3 FY20 levels in 4 quarters (by Q1 FY22)

Provisioning considered all the customers in moratorium although only 14% didn’t pay any EMIs in 6 months, rest paid partially

Provisioning will be less in the coming quarters as the current provisioning is more than the expected worst case scenario

SMA 2 200+ crs in Q4 but had significant recovery in May/June/July so confident of having better NPAs than industry

Have lowest delinquency pool % in the industry

Customers under morat has both salaried and SENP, overall ~0.5% customers had job loss, pay cut for 4-5% of the customers but most of them at manageable levels like 10-20% cut. So expecting flow from regular to delinquency pool will be lower

SENP delinquency is slightly higher vs Salaried but loans are given based on declared income only not just based on assets

Loan book:

Usually 75% of the book is <3 years old for most HFCs

All loans are floating rates only

25% of housing loans are for flats, 75% for individual houses, repair etc

Normally 20% customers churn out in a year due to lower interest rate outside but focussing on retention more in the last few quarters. Also similar % customer come in from other HFCs. So net effect is marginal

50% of salaried customers are from PSUs

Loans given to SENP customers in states like Rajasthan and Gujarat where repayment culture is good and most of them are self employed

Liquidity/Capital raising/Stake sale:

4k crs unused liquidity from banks

Comfortable with current D/E 8 and would like to keep in 7.5-8 range

NIMs of >3% should be good enough (current NIM of 3.7% is too high and will come down)

NPAs will go up and come back to pre-covid level in 4-5 quarters; Full moratorium was 14%, bounces and part moratorium were another 14%

In affordable housing, disbursements are back to 65% and will be back to 85-90% of peak disbursements by year end (Q4)

In home financing NPAs start showing up after 2-3 years once a company starts disbursing in a new geography. Weighted average loan duration in non-Southern markets is ~3 years for them

Want to expand in smaller cities (better pricing; lower ticket size)

Plan to raise capital in last quarter of FY21

FY21 will be de-growth in disbursements of 10-15%, FY22 will be flat growth and FY23 growth will come back

with about 7.5 years of being invested in this, I am moving on.

I still dont see a midsize home finance company thats disciplined, reliable and focused on market share. The new CEO has been a bit disappointing, I see a rough patch for next couple years.

There is a large addressable market where a good focused company can grow 20% plus for next 15 years. But I think there are other opportunities now, sold it…

I agree with your statement - “There is a large addressable market”.

I am also bullish on Housing Finance sector and have been investing in these firms for last 6 years.

I invested in various HFCs: HDFC, LICHF, CanFin, Indiabulls HF, DHFL. Some of these companies turned out to be fraud, some not high quality.

I am still bullish on the economics of Housing Finance sector and willing to pay higher price for quality (management integrity and operational efficiency)

So I have increased my holding in HDFC and sold off the rest of HFCs from my portfolio.

Current debt equity is 7.3x (in context of RBI discussion paper that leverage be brought down to 7x for NBFCs)

Growth was lower this quarter because Telangana government had closed registration for 2.5 months of the last quarter and Canfin gets 20% business from there. This issue is resolved now

Housing demand is back, don’t see challenge in growth (should have 17-18% growth in disbursements and overall book value going forward from Q4FY21)

NIMs will come down from 4%+ to 3%+ levels because they are currently repricing their loans for a large part of their current customer pool. Want to maintain 3% NIM and 2.4% spread over long term

February disbursements highest in the history of company

Steady state growth should be 17-18%, 70% of incremental disbursements will come from South India (though they are concentrated, they like South India)

Have aggressive growth plan, so will raise capital soon

COVID provisioning was sufficient, should be able to write back some provisions depending on RBI regulations

Highest ever disbursements because company has been very aggressive in pricing of loans to grow loan book + retain existing customers. ~22% of existing portfolio was repriced. As a result, NIMs and spread will ultimately come down to 3% and 2.4%. This is a shorter term strategy for the next 3-4 quarters. Currently, there is lower demand in self-employed loans and Canfin doesn’t want to lose market share. Additionally, cost of funds have come down drastically which allows Canfin to lend at lower rates. There is a renewed aggression for growth and want to grow disbursements at 20% (compared to FY19 disbursements of 5500 cr.)

Average ticket size has gone up from 18 to 20 lakhs in Q4FY21 because of focus on giving loans to customers up to 1cr. They are now targeting a different customer profile (30-40 lakh loans to salaried individuals) where risk is lower, but yield is also lower. As a result, volumes will have to offset margin pressure

Incrementally, salary customers account for 83% of new customers and only 17% are self-employed

Made provisioning of 76cr. and were planning to add back 70cr. this quarter. However, haven’t done that and kept 70cr. as additional provisioning

Commercial paper funding is only when there is excess undrawn fund limits (which are more expensive) and issuing CPs leads to lower costs. CP money is not raised for actual lending operations. Current liquidity is for the next 7-8 months which will be maintained going forward. Overall mix for CP funding is capped by board

Most bank loans are term loans (8-10 years). Incremental cost from bank borrowing is 5.5%