In the end, what matters is which investments make the most money for you. If you have to choose between the top 10 stocks to be considered for your portfolio, you will have to compare them across industries and sectors. The only way to do is by focusing on their cash generation capabilities which Rahul has explained very well

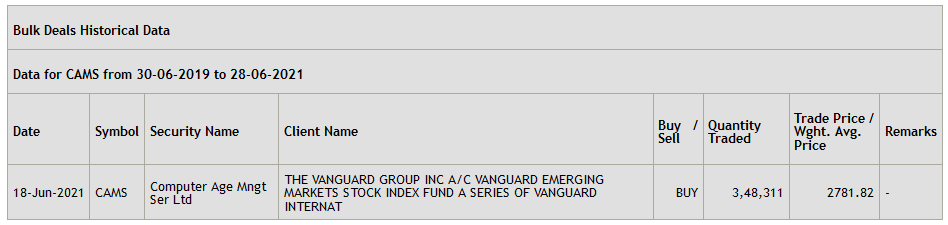

While the stock of CAMS entered the secondary market in October 2020, it could not list on the NSE then as at that time CAMS was being backed by NSE’s subsidiary firm. And through the IPO route, NSE Investment Ltd that held over 37 percent stake in the company, fully pared its stake

1 Like

The most important part in CAMS is element of high barrier to entry. CAMS is the largest player in the AUM business with 70 per cent market share. It is very difficult to any new player or existing players to get into the business and gain market share.

I believe in investing in fundamentally strong monopolies and CAMS is definitely one.

Just sharing my personal view on CAMS.

4 Likes

I have a very basic question. Why does KFintech has more AMC clients than CAMS? Those clients are relatively much smaller compared to CAMS. But it is a case that any new/smaller Mutual Fund AMC prefers KFintech over CAMS?

I believe, MF industry is going to grow a long way in India, and a lot of other new/foreign MF companies are going to setup business here in the long run.

5 Likes

Annual results are out. Revenue growth remains muted but there has been a healthy increase in PAT due to a decrease in opex.

The last question in the concall hit the nail on the head. The person asked what’s the excitement of owning a business that’s making close to 30% PAT margins but can’t figure out an alternate way to accelerate topline growth? Currently, the business is akin to a utility business dependent on the volume growth of the MF industry for its topline (MF revenues are 90%). The management answered by saying that the mutual fund industry grows in phases of high growth followed by a period of consolidation and preceding the lull since 2018, the industry grew at a CAGR of high teens since 2014. Not sure whether this means they expect the growth to pick up again in the next few years.

They also admitted that their forays into other revenue streams have been unsuccessful so far. After that the call recording on Trendlyne went silent (the management spoke for another minute or so). Did anyone manage to hear this?

This business ticks a lot of the right boxes but considering the muted topline growth and no indication of other significant revenue streams or optionality playing out, I feel that current valuations are unsustainable. At the right valuations, this business provides a lot of MoS because the MF volume has a long runway of growth lying ahead and the RTA industry is oligopolistic with CAMS in the dominant position.

Curious to hear the opinion of other investors?

11 Likes

Sorry, but I thought the question was quite inappropriate and rude. The management is running a serious business, they’re not here to give excitement to others. If the analyst is looking for excitement, he can invest elsewhere, no one told him to invest in this. The list of exciting businesses where investors came to grief is long.

5 Likes

Some good insights on CAMS operations and business models.

1 Like

@novneet_nov

My personal view - If you read the “About Us” section of both the companies than you will observe that CAMS has more focus towards their existing customer and to gain market share within the country. But that is not the case with Kfintech, their focus is towards getting rapid expansion to different countries. They are focusing on adding more number of clients and CAMS is focusing on getting quality companies only.

1 Like

Is CAMS revenue subject to the cyclicality of the stock market or Interest rates ? Just that AUM of the amc’s goes down so they pay less?

Revenues are directly linked to AUM, But AUM of MF industry has its link to cyclicality of the stock market/interest rates.

So overall they are interconnected

so we can conclude that during bear markets or low inflation periods revenues of CAMS will be impacted? and opposite is true during bull markets or high inflation periods because of higher interest rates debt fund AUM’s go up?

CAMS

Base business steady; new products to add gradually

-

CAMS posted a steady set of numbers in terms of business growth, which was in line with industry. A similar performance was reflected in its topline growth while cost controls and reduced tax boosted bottomline.

-

For CAMS, average assets under management (AAUM) serviced increased 19.2% YoY, 7.3% QoQ to | 22.3 lakh crore, largely in line with the industry AAUM growth of 18.9% YoY. Equity AAUM increased 18.5% YoY, 12.1% QoQ to | 7.9 lakh crore (calculated) while debt AAUM surged 19.6% YoY to | 14.4 lakh crore. On a sequential basis, equity asset mix increased marginally by 1% to 35%

-

Transaction volume growth rose 5% QoQ to ~8.2 crore vs. flattish growth of 1% in previous quarter. SIP book rose 5% QoQ to ~2.1 crore while number of SIP transactions processed was up 5% QoQ to ~6.1 crore. Increasing traction in various business parameters has enabled CAMS to maintain its dominant position with a market share of 70.1% in MF servicing.

-

Revenue from operation was up 14.3% YoY to | 199.8 crore. This was slower than AAUM serviced growth due to a fall in non-MF revenue. Growth in asset based revenue was 18.5% YoY, in line with AAUM growth. Non-MF revenue declined 15.9% YoY due to winding up of banking and NBFC outsourcing business while account aggregator business is yet to kick off. MF’s share in total revenue is up to 90% now. Steady yields amid marginal increase in equity mix implies static pricing without any meaningful downward revision. Cost were kept under control while EBIDTA margin was largely stable at 45.7% vs. 45.9% QoQ. PAT came in at | 60.1 crore, up 39.6% YoY, partly driven by a lower tax rate regime.

-

The company will continue to invest in technology and security in order to improve process efficiency while it has also strengthened senior management team by adding a Chief Risk Officer and Chief Platform Officer to improve execution capabilities. During the current quarter, the company signed a letter of intent with 15 entities for account aggregators business.

8 Likes

Hello everyone,

I have one question - isn’t smallcase pose threat to CAMS? Idea of smallcase is to provide transparency which lacks in case of mfs according to Zerodha’s Nithin Kamath. Both smallcase and mfs are fee based and rebalancing occurs quarterly in both ( few smallcases has weekly rebalancing too), while smallcase delivers all the stocks into your dmat where as mfs doesn’t. Isn’t this point excites investor to choose smallcase instead of mfs ? If that’s the case, isn’t this directly impacts CAMS business.

2 Likes

We need to understand the landscape of the investor community, their knowledge base and accessibility.

-

Investor landscape : Many (I would even dare to say most) investors look to put in a small quantum of money periodically (monthly). In this aspect both smallcase and MF score a point each.

However, if you consider a institutional (a company) investor/a trust and/or other non-retail investor segment - most of them would prefer a MF route. Consider a large company trying to put its money in a debt instrument - they almost invariably go to a MF. Similarly a trustee company - which allocates money in securities market would go for a MF. -

Knowledge : This is where MF scores heavily w.r.t smallcase. Most of us invest in MF - because we believe that

they are the experts. On an average, MF’s have behaved accordingly (expect few bad eggs). Now we do not have such insights, maneuverability (in terms of handling the portfolio) when it comes to smallcase (as we have to manage smallcase buckets ourselves). Hence as the spread of the investment philosophy expands in the country, most preferred route would be MF’s. -

Accessibility : Here, MF’s did have a drawback 5 years back (with a non-existence IT systems, poorly managed backend IT systems) etc and at the same time smallcase did not exists. However, MF’s have improved greatly they offerings for individual retail investor (in terms of ease of use, simplicity etc) and same goes for smallcase. On a biased note : I would argue that MF’s due to their popularity, seems to score better than smallcase. Not many investors would be aware of smallcase (or their any similar looking twin cousins

)

)

Hence I do feel, MF’s would outgrow or be inline with the growth graph of the investment trend in the country for years to come.

Disc : Have invested in recent market meltdown.

Not a registered security advisor and this post does not suggest for anyone to either buy/sell/hold the investment in the company.

10 Likes

1 Like

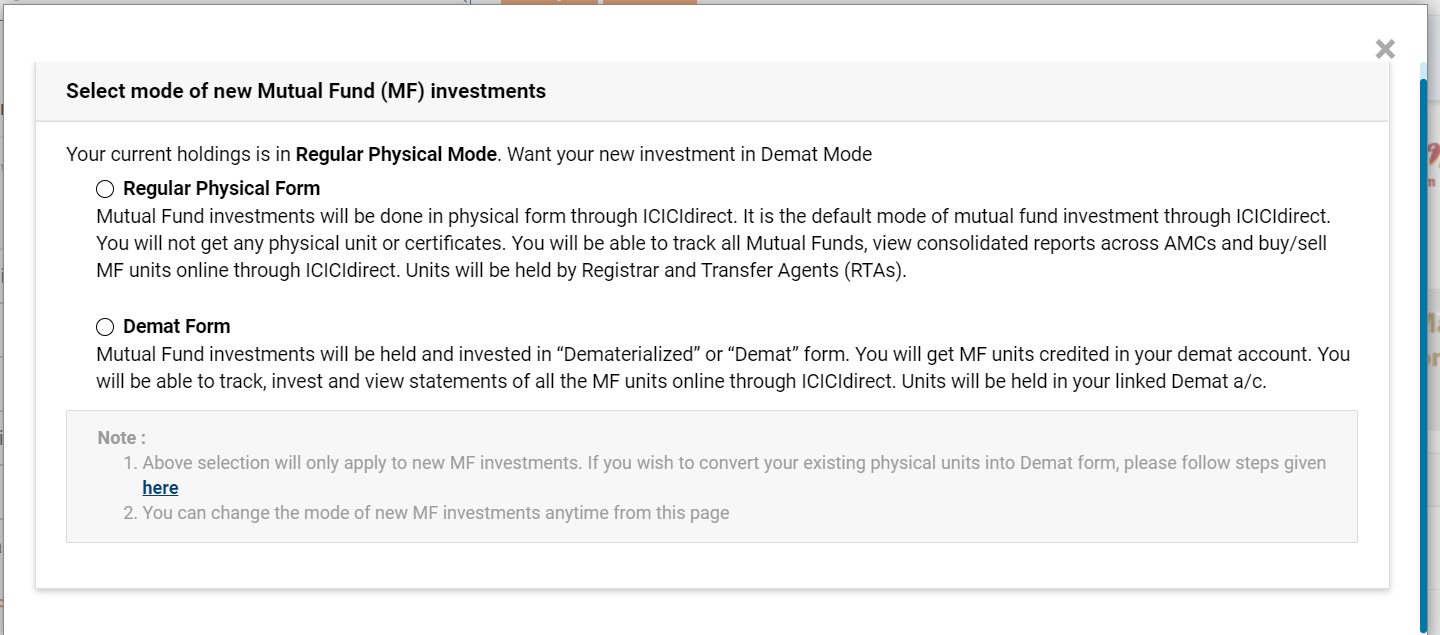

wondering what impact will it have on CAMS revenues when people start getting MF units in Demat form.

the snapshot is form ICICI Direct website.

1 Like

Even for these third party platforms, the back end work is done by CAMS, so where you buy from does not impact the revenue of CAMS.

And it seems this MFs in demat facility has been for a while. MFs mainly cater to the masses considering the lowest ticket size it starts at, and we have regular and direct MFs here, so not everyone will have a demat account. I don’t have the numbers but people who invest in both stocks and MFs are less compared to people who only invest in MFs and MF investors will not open a demat account without any additional benefit for them. Who invest in stocks and MFs may want to have everything in one place, but even for this we have consolidated account statements from NSDL, CDSL, CAMS etc. And then there are DP charges while redeeming units.

Here is one article, that provides some details.

5 Likes

I think this is quite a confusing and misleading change done by ICICI Direct recently. The use of words “physical” and “demat” here is not the same as physical and demat we understand in the context of equity shares. This should not have been done without clearly explaining the costs and benefits of both the options. We say mutual funds are for ordinary individuals who are not financially savvy and then we keep making things more and more complicated.

6 Likes