Campus Activewear Ltd - The company manufactures and distributes a variety of footwear like Running Shoes, Walking Shoes, Casual Shoes, Floaters, Slippers, Flip Flops, and Sandals, available in multiple colors, and styles, and at affordable prices. !7% India Market share as of 2021. Mens Centric brand 88% sales came from men’s segment. 4.6% from women and 8% from kids

Management

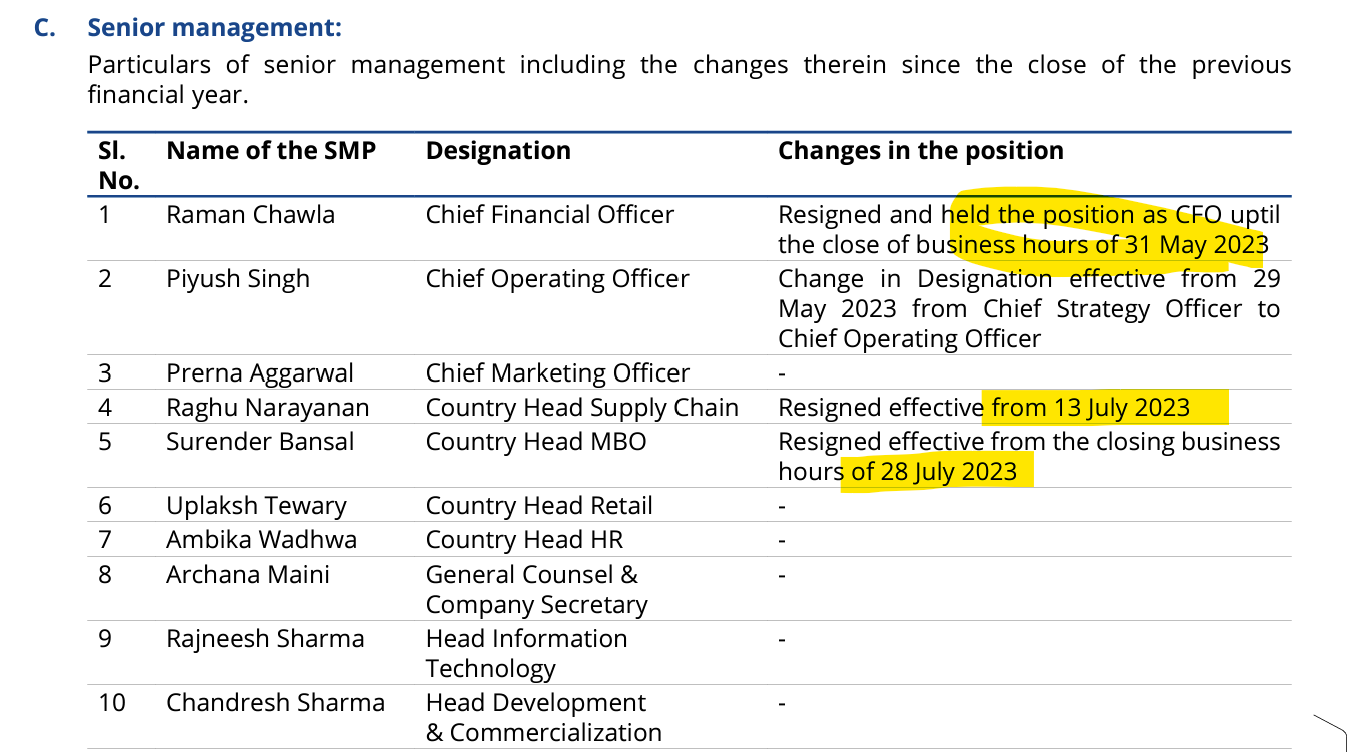

Hari Krishan Agarwal Chairman and Managing Director

Nikhil Aggarwal Whole-Time Director and CEO

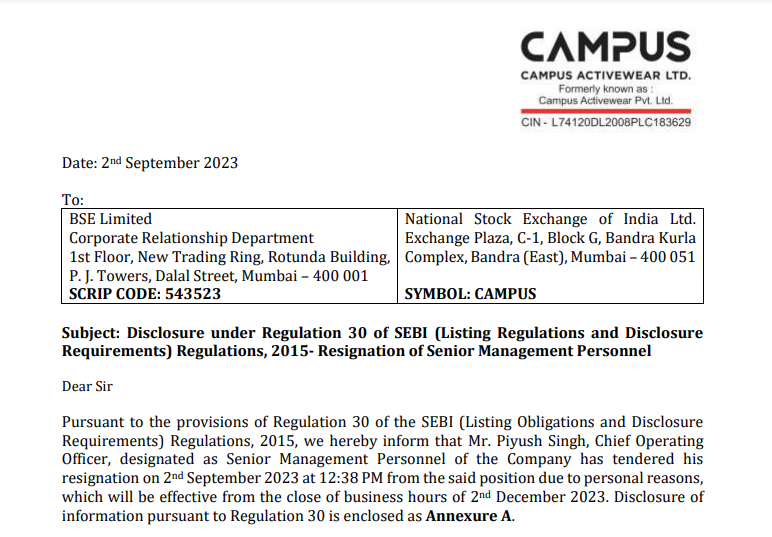

Archana Maini is the Company Secretary

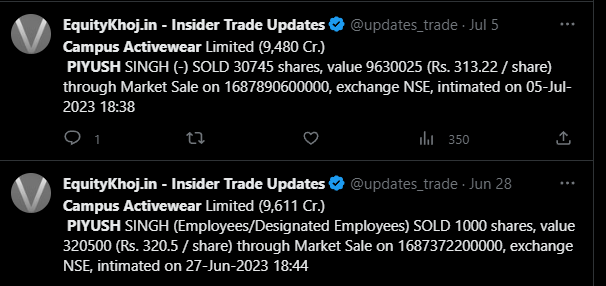

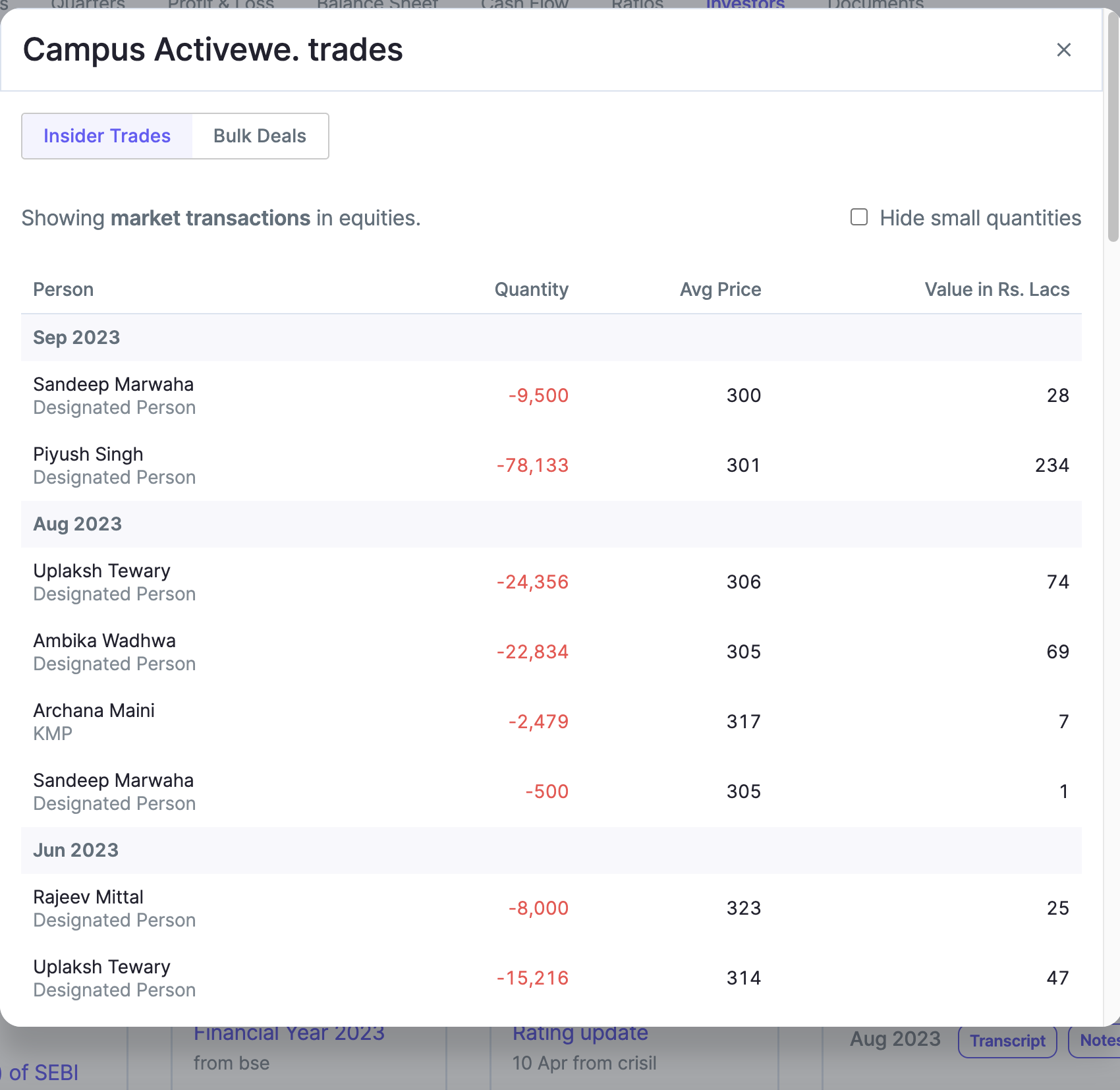

Raman Chawla – CFO

Employees – 784

Competitors - Bata (Power), Liberty (Force10), Relaxo (Sparx) and Mirza International (Red Tape Athleisure and Bond Street)

Big Picture Narrative - Per Capita Income increase, need for different types of shoes based on occasions, fashion statement, the rise of women in the workforce, kids segment, people going for more casual shoes in day-to-day wear

Total SKU - 6388

Campus Average Selling Price 600/700

Metro Brands - 1200/1400

Raw Material - raw materials such as leather, rexine (registered trademark of an artificial leather-like fabric), inter-lining, PVC sole, rubber, net, cotton, etc. China and other Asia Pacific countries are the largest exporters of raw materials required for producing footwear. RM cost 55% as of 2021

Inventory - We usually keep two to four months of inventory of raw materials at our facilities. The ability to store raw materials at our facilities enables us to withstand disruptions in supply as well as volatility in the price of raw material. We plan our inventory levels based on existing inventory levels, inbound delivery timelines and expected order pipelines.57% of assets as of 2021

Receivable at 34 % of total assets as of 2021, they give 90 days credit to distributors.

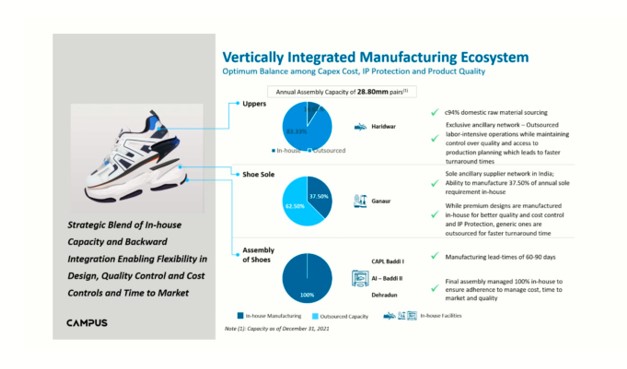

Campus has more than 85% raw material sourcing from the domestic market, which provides it with significant supply chain efficiencies while maintaining quality standards through 100% in-house assembly

Being in Latest Fashion trends is extremely important for this Business-

We have adopted a fashion-forward approach to new product launches to ensure that we have a faster design conceptualization to product commercialization cycle. We are typically able to launch our products within 120 to 180 days from the date of product conceptualization…

New launches take 120-180 days from design to Retail. It allows them to do two season launches in a year. 48-member design team. Designing for a season begins nearly six to eight months prior to the upcoming season. The sketches are sent to heads of departments and key decision makers. Thereafter, our prototype team makes prototypes of our products using samples in various colors.

Debt/Equity 0.43% . Total debt 174 cr as of 2021

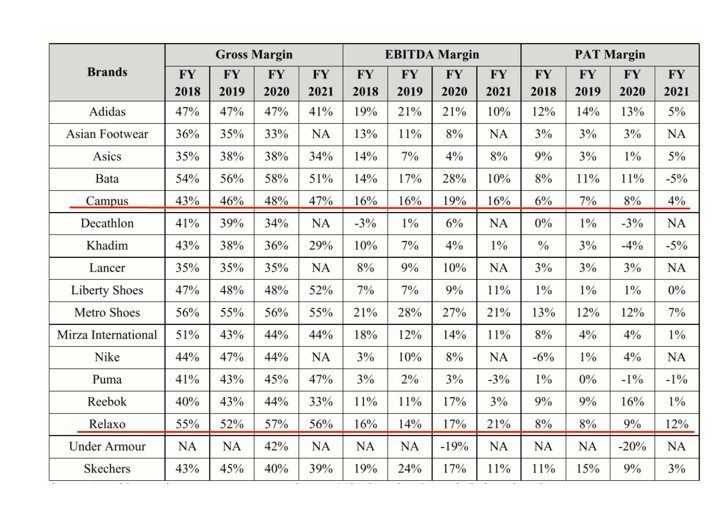

Profitability -

Campus cant convert its higher EBITDA Margin to PAT Margins as compared to Relaxo.

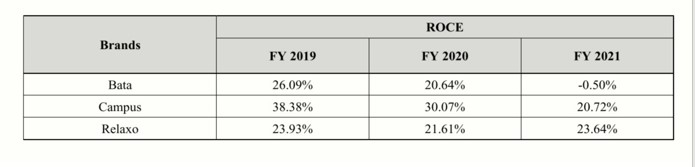

ROCE -

India Market Size & Growth Prospects (Athleisure) - India is mirroring the global trend with respect to sports and athleisure and outpaced the global growth rate of the segment. It is estimated to be ₹ 19,500 crore. It is estimated to be ₹ 19,500 crore (USD 2.6 billion) in FY 2020 and is expected to grow at a rate of approximately 16% by FY 2025, almost doubling in size.

Domestic Footwear Market - The domestic footwear retail market in India estimated at ₹ 72,000 crore in FY 2020 is projected to grow at a CAGR of ~8% to reach ₹ 1,05,000 crore by FY 2025. Footwear industry in India has grown at a CAGR of ~9% over FY2015 to FY20

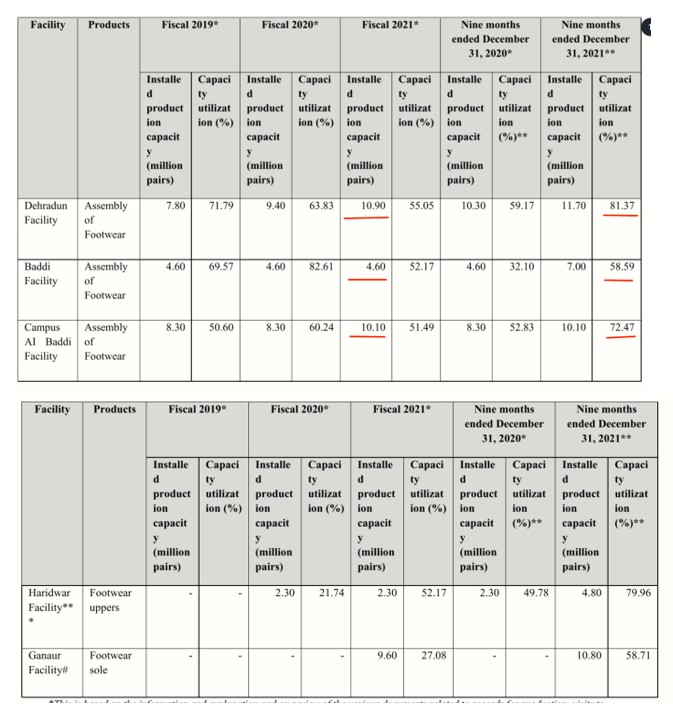

Manufacturing Capabilities - Total 29 million pairs capacity. Haridwar Facility is responsible for manufacturing our uppers, Ganaur Facility is responsible for manufacturing 37.50% of the soles. Dehradun Facility, Baddi Facility and Campus AI Baddi Facility are responsible for assembling all of our products

Outsourced Job Work - Our cost of materials consumed includes job work charges for the manufacturing process, it was 10.62% of the total revenue

Capacity Utilization -

Dehradun & Baddi are at an average CU of 75%, Im not sure if in the footwear industry factories operate at 100% CU, If that isn’t the case then they will need Capex soon. IF they don’t have enough internal accruals, they might have to raise debt or do QIP. The reason I am looking at these two units only because they do 100% assembly in house. A significant portion of Upper and Sole manufacturing is outsourced

Product Pricing -We sell footwear across the entry-level (MRP at or below ₹1,049), semi-premium (MRP between ₹1,050 and ₹ 1,499), and premium (MRP at or above ₹ 1,500).

Revenue contribution from the Premium category 41% in 2021. Average Selling Price 615 as on 2021. (ASP of 615 indicates a Mass market appeal)

Pricing Power - We do not have any specific retail policy and standards for “sales made through distributors”. We do not control the price at which the ultimate retailer sells our products.

IT Capabilities - These tools include systems for enterprise resource planning (ERP), distribution management system (DMS), field force management, point-of-sales (PoS), e-commerce order management (OMS) and a retailers’ engagement application

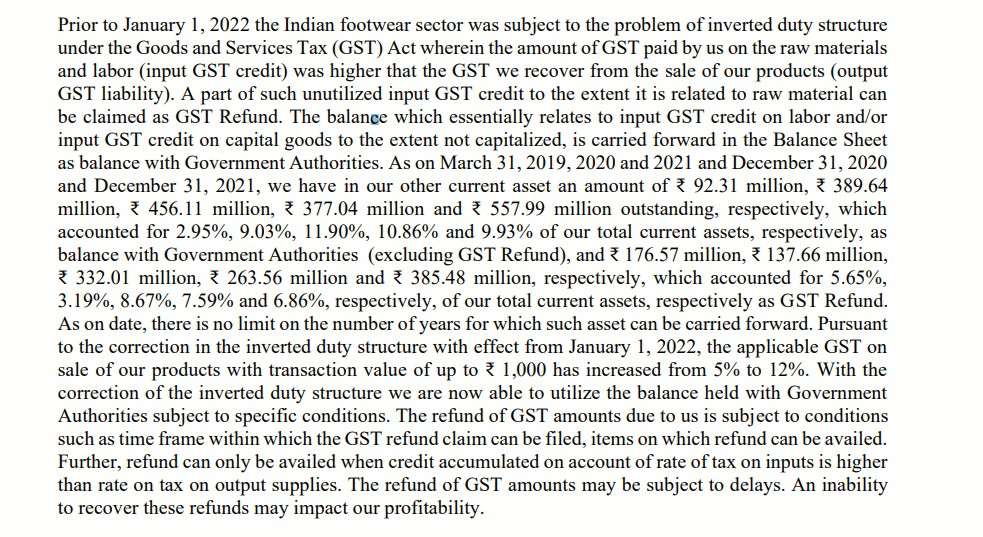

GST Tax Mismatch -

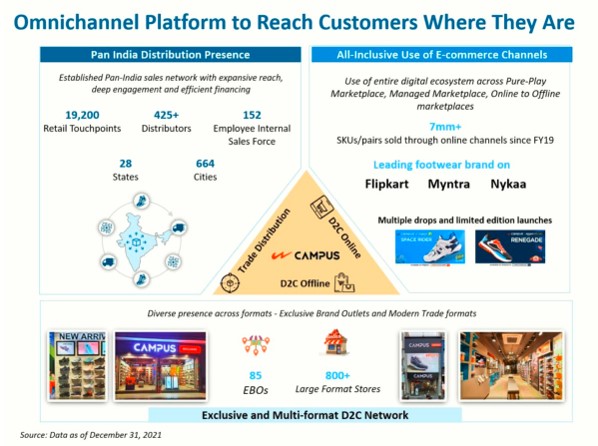

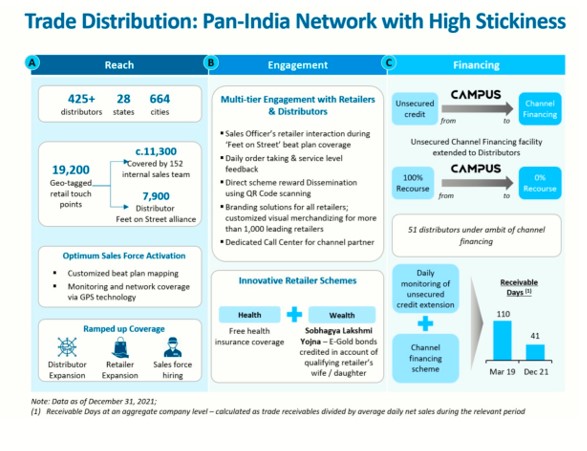

Campus Distribution Details -

Trade Distribution – 75% - Volume sold – 81 %

Direct to Consumer Online- 21% - Volume sold – 16%

Direct to Consumer offline – 3.50 % - Volume sold – 2.5%

Internal Sales Force of 152 employees - they use Sales Force software for Distribution Management System

They also have a Retailers Engagement App

We have over 425 distributors as on December 31, 2021. We are dependent on our trade distribution channel for the majority of our revenues from operations. We have 57 COCOs and 28 Franchisees as on the end of the period of December 31, 2021

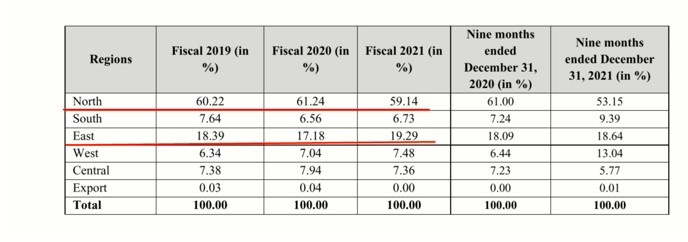

Geography Concentration - 68% of the revenue comes from North India

Business Seasonality - Historically, revenues in the third and fourth quarters have exceeded those in the first and second quarters. The mix of product sales varies considerably from time to time as a result of, among other things, changes in the season

Refund & Exchange - Trade distribution We have a return product policy for all our trade distribution customers. Our trade distribution customers can only return products in case there are any manufacturing defects. In such instance, the distributor will collect all defective products within a period of six to eight months from the date of purchase of goods and inform our sales representative. The distributor will thereafter cut / destroy all defective pairs in front of our sales representative to prevent any misuse. We will thereafter issue a credit note in the name of the distributor

Usually, apparel, shoes etc manufacturers have some amount of provisions for returns in the Balance Sheet, need to find out what is the annual provision percentage to sales. 2022 AR not out yet

Advertising spending is at 6/6.5% to total sales.

Risks -

They have to continuously come up with new designs and keep up with the latest trend in casual shoes. Nike, Adidas, Puma Under Armour have new design launches every season with a variety of color and different soles. The designs have to also appeal to the younger crowd there is a lot riding on the design team.

A good portion of Uppers & Soles manufacturing is outsourced, maintaining the quality and converting the new design ideas from desk to the store will be a key deliverable for them. Maybe in the long run they do everything in-house to mitigate the outsourcing risk. It’s a double-edged sword in my opinion. Page Industries maintained the quality by manufacturing in-house however there are players in that segment who outsource everything.

One can be a victim of their own success, looking at the growth and margins, other parties may enter the business, probably established players who have deep pockets and decades of industry experience. It’s a highly competitive industry.

Reebok & Fila are two examples that lost market share and reebok has been revamped now. Fila, I am not sure, but I haven’t seen many products in the market. Good brands with quality products however lost their charm, it can happen to any brand that is not up to date with the market trends.

i have a tracking position, and will be adding as the story develops. at the onset, i like the company and there is good growth in revenue and profits. it fits well in the consumption theme. the asp of “615” caters to a huge section of the population so long term growth story looks good. They will have to keep coming up with new designs to be relevant in the market. Adidas, Puma, Nike are constantly launching new designs. its a very competitive market. however at a lower price range, probably CAMPUS has an edge, time will tell. Waiting for their 2022 Annual Report

Sources - DRHP & Concalls