Debt is ok - check ur position sizing while investing.

Tailwinds do matter in busineses like these. Ground reality is businesses which don’t have a lot of funding is a debt route which makes sense - Brands like amazon would need to see upfront investment to give orders such as above. If the promoter pledging bothers you, we can track if they decrease this over time when they generate cash overtime.

Also, its a good practice to see such disclosures from small companies. Otherwise many companies share price would have blown up before the annoucements like amazon.

Management spoke about technical collaboration for the BLDC Motor after they had developed a range of BLDC Drivers.

Recently they announced the collaboration too with Taehwa Enterprises

And this is an example of management guidance and capabilities - along with the “Walk the talk” behaviour we tend to associate with good businesses.

Apart from just business it does and its future prospects. I came across that company runs an institute to train new employees on an internship basis, and provide internship certificates so that they can pursue their carrier in a similar industry anywhere.

How often, or even do you see a 200 Cr. market cap company do that? And imagine the potential talent pool they are generating for themselves, the loyal to be employees they are generating for themselves, it could be immense.

They had a very good history pre-2008 period and the same management is running the business currently. They have done it before by being the largest company in India to make TV sets for companies like Bajaj, Thomson, BPL, etc. This management since 2013 is trying to turn around and with LED product development, they seem to have found the right category to grow. The management knows from their past experience to make this category a game changer.

Regards,

Invested a small portion of the portfolio.

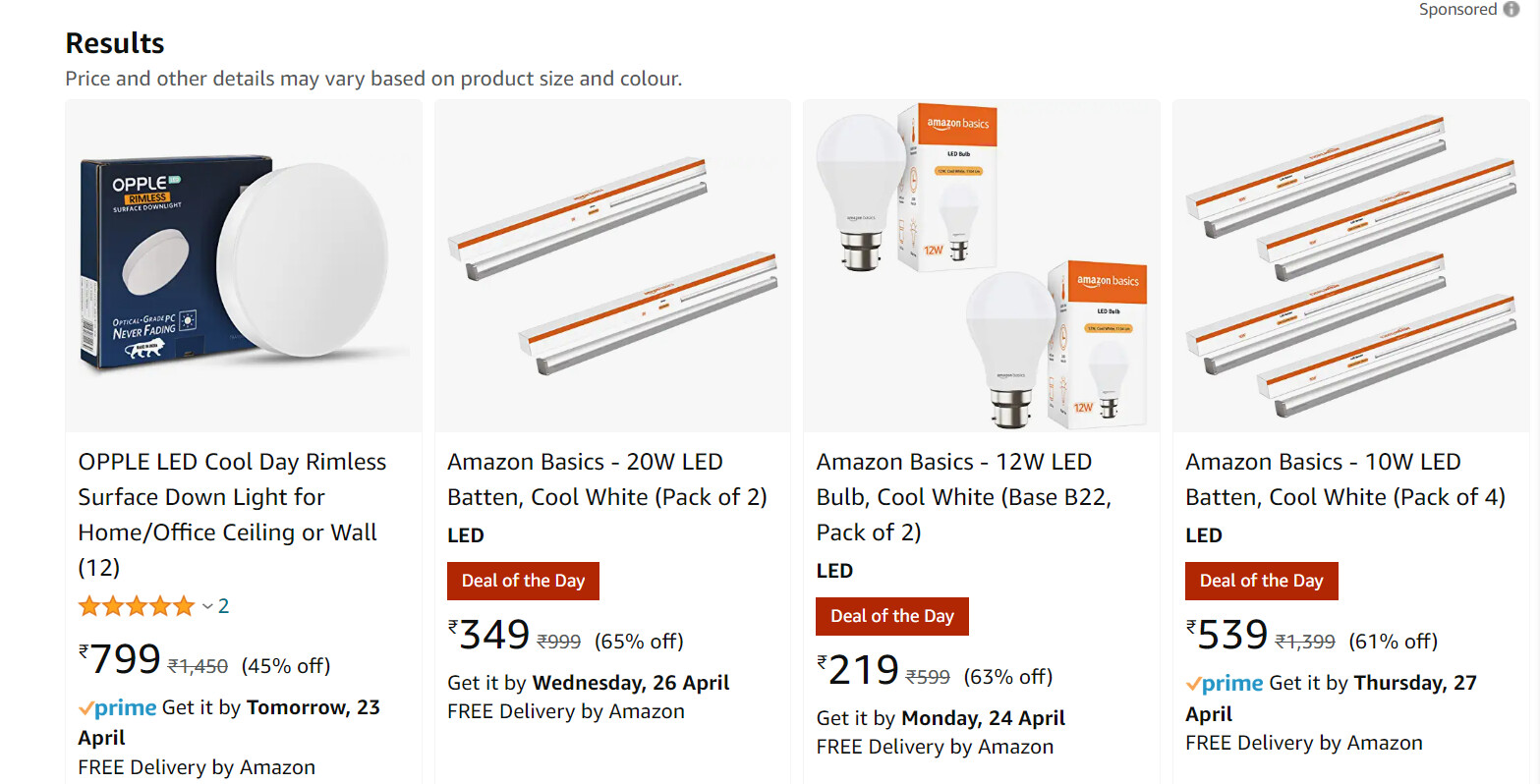

We have got some mixed reviews on Amazon. I am happy sort of that sales of Amazon Basics LED Bulb have started and now we have LED Batten too. There are roughly 10-30 ratings on every listed product on Amazon and according to a stat from my friend (just for his business on Amazon), he says an average of 1/10th person gives a rating and 1/50th give a review.

So, to judge product quality and its acceptability, it will be interesting to track the ratings every month maybe.

So IKIO Lighting IPO just listed. So EMS Space obviously is in limelight this year atleast.

EMS Space

EMS Exports trillion $ market

China contributes 600 billion dollars

India is only 25 billion dollars - Also in this 25 Billion $ mafrket Apple is 5 billion dollars.

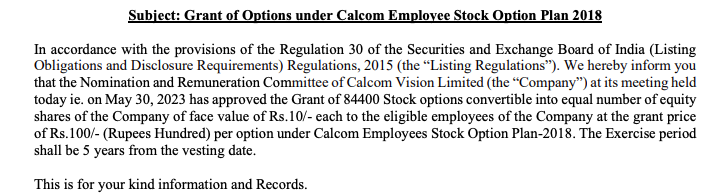

Calcom Vision preferential issue approved**. MIT** has entered again. Preferential price set at Rs 157. MIT has invested again via the preferential. Very positive for Calcom.

at Current number of shares and profit for the FY23 at 30 PE Reasonable Price is ~138

and at 40 PE ~184

it becomes good bet at anything below 130.

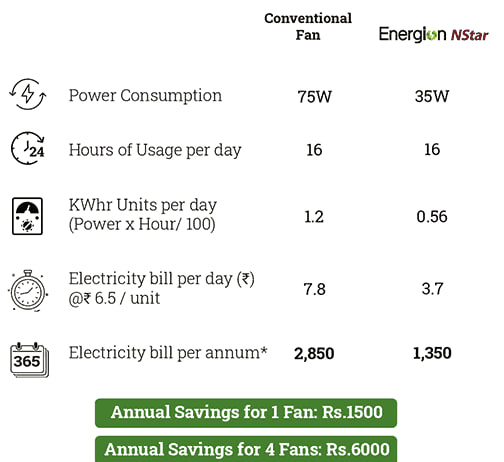

In one of Interview of Dixon owner he mentioned in EMS LED manufacturing has become most matured in India so i expect it won’t be growing that fast while BLDC fans is still a evolving story.

Mostly in stocks like calcom vision. Many a times you will be able to see re rating on basis of certain good quality parameters. One of those parameters is “Terminal value”. With amazon choosing Calcom for LEDs that means the terminal value has increased. Second one of similar parameters could be “Optionalities”, Calcom has LED background as of now. BLDC motor is one optionality that brings in new verticals into the picture ie BLDC Fans. Also, as they gain experience with clients like amazon and M&A for BLDC motors they can bring in operating leverage and operating efficiency. So just evaluating on one parameters might be more injurious. Keep your exits in place by designing the anti thesis. This has helped me with many multibaggers. One can’t exit at top and definitely can’t time bottom in all PF stocks. So stick around - stock price has definitely moved from 138 to 170. Look at the business and not the stock price to decide on bigger decisions like selling.

Hey gautam, as it seems you are tracking it closely, can you put some light why their is huge down side in Margin ?? From material cost to Employee cost everything is looking stable, still huge downside in Gross margin ?

After amazon orders for “Amazon Basics” my thesis is around optinalities wrt Amazon itself. If Calcom does well for Amazon Basics and Amazon willingly goes ahead and bumps up the order the thesis should play out really well.

Also, the next optionalities would be around amazon or other similar e commerce players like flipkart etc would opt in to jump in with such orders. And BLDC plays out is another thesis. The flags are green as of now as they acquired/joined hands for the tech for the same.

Other thesis is the category to expand as this is a major building material space when you can see Real estate boom domestically. Amazon also envisions the same that’s why they started with own brand LEDs etc