Most of their outlets are rented. This makes them very vulnerable to lease rentals. They face competition from Barista, Bru etc and the competition will only grow. The valuation of the company is high. If you like it, you will almost certainly get it at a lower price. This is the sort of company to look at in a beaten down market, where it can be priced much lower. It can be a good long term growing brand.

I do not agree with someone in this thread who sees the political links of the company as negative. It is impossible for Indian companies to grow to this extent without dealing with politicians. The political link is in fact a positive.

You are wrong here. Political connections are red flags one should be cautious about. One needs to be sure about how they have created value in the past and what is the gameplan for the future. Some point of time they WILL face adverse political situation and work against value creation. Tell me one politically connected enterprise among consumer businesses which has consistently created value?

Nope. Political connections are useful in getting loans, getting loans written off, getting tenders, cutting red tape, buying land for expansion, the list is endless.

There is a video going viral since yesterday where a CCD Jaipur employee slapped a customer for pointing out insects in their fridge. It is serious negative PR for the brand among their prime target market.

Yes, saw the Cockroach Coffee Day video, it’s so unfortunate that happened. That lady staff has in turn filed an FIR against the customer citing reasons of women harassment. We live in strange times.

I was exploring the expenses, I find the breakup is like this:

Cost Of Goods Sold = 21.5%

Power & Fuel Cost =1.23%

Employee Cost = 11.11%

Manufacturing Exp = 4.38%

General & Admin Exp = 44.61%

Selling & Distn. Exp = 0%

Miscellaneous Exp = 1.53%

Can someone explain what comes under General & Admin expense, why is it so high, I was expecting it to be lower than Employee Cost.

Secondly I was under the impression rent would be a big part of their expense. where is rent included?

Highlights of Q4 FY18 and FY18 results

Financial Highlights

Q4 FY18

o Gross Revenue grew by 26 % to 12,970 million compare to last year same quarter

o EBITDA grew by 16 % to 2,134 million compare to last year same quarter

o PAT grew by 95 % to 252 million compare to last year same quarter

FY 2017-18

o Gross Revenue grew by 22 % to 43,305 million compare to last year

o EBITDA grew by 21 % to 8,253 million compare to last year

o PAT grew by 127 % to 1,063 million compare to last year

CDGL business for FY18

o Retail coffee gross revenue grew by 7 5 to Rs 4,005 million compare to last year

o Retail EBITDA grew by 8 % to 748 million compare to last year

o PAT grew by 18 % to 81 million compare to last year

For the year ended FY2017-18, company Retail Coffee gross revenues are up 12% to Rs. 15,907 million and Retail EBITDA is at 2.,906 million, up 14% YoY

As at March 2018 end, Company Cafe network stands at 1, 722 spread across 245 cities in India.

Company added a gross of 43 cafes during Q4FY18 and 135 cafes during FY18. Company Q4FY18, ASPD grew to Rs 15,635 (11.9% growth vs. Q4FY17) and SSG growth came in at 8.2%. This quarter has been the 2Sth consecutive quarter of positive SSSG for company. The percentage of cafe transactions through digital stands at above 46% during Q4FY18

The mobile app downloads have crossed 4.4 million as at March 2018.

Total Vending machines installation as on March 2018 stood at almost 47,750 machines , having added a gross of over 2,400 machines during Q4FY18 and almost 8,000 during FY18

Key Initiatives

Strengthening the Round-the-clock-menu offerings at company cafes and expanding the reach thereof

Offering consistent value proposition

Building, deeper consumer connect through targeted marketing campaigns

Subsidiary Performance

Sical Logistics

o Secured two multi-year contracts with significant contract value

o Revenue grew by 40 % to 4,200 million

o EBITDA stood at 490 million

o Company IT park at Bangalore let out office space portfolio of 3.46 million sq ft which generate steady rental income of 410 million

Q&A

In Q4 ASPD machine sales has gone up then why there is a fall in Q4 Revenue compare to Q3 ?

o From 14th November tax rate has come down to 5 % from 14 % yearly so this went with top line. In Q4 retail growth is 12.5 % and 14 % yearly compare to 7 % last year

What about capital employee between retail and trading business ?

o Around 80 % is in retail

What is company install capacity in vending machine ?

o Company assemble the vending machine and 15,000 machines can be assembled in a year

Is there is any scarcity of machine ?

o No there is no scarcity of machines but company take control of machines because company take very less deposit and also give one machine for free to distributors . So company is very careful in generating revenue .

Why does depreciation increase in Q4 ?

o Company had write off 2.5 Cr of old assets

What is the café size in smaller store and refurbishment ?

o Every year company refurbish 150 stores and total store count to 1722 . Old shop rent has increase due to acceleration in rent of 15 % YOY of a 400 sq ft shops . Company can get 1000 sq ft shops at same rent nearby . So company is doing these changes in 200 Cafes which are without washroom and rest 1500 are in prime locations so cannot change that.

o Replacing Café which are in mall that has low footfall due to better malls

o In Corporate office also sometime corporate office shift so Café will shift accordingly

o In some cities the trade area change so shop shift according to trade area

What are the food and Beverage revenue mix for Q4 ?

o Q4 comprise of 34 % food , 61 % beverages and 5 % merchandise

What is the company target for FY 2020 ?

o 20,0000 ASPD by FY 2020

What number of stores company adding in FY19 ?

o Opening of 130-135 stores in FY19 and closed 95 stores last year

o Company had also started a 3500 sq ft Café in Park Street

What is the current net Debt level of company ?

o 320 Cr and there is no plan to reduce it because company want to grow at 15 % . Company will take long term debts if opportunity arise .

What would be each Café cost ?

o Average 40 lakh including 2.5 lakh deposit

What is the cost of machine ?

o Machine cost is 1,10,000 and 15-20K spend on branding and trading .

o Company have more then 18,000 to 20,000 customers od machine

o Company get the customers and then distribute the machine to distributors . Company allow a mark up on the price for distributors .

o 95% of business comes from distributors

Why does company Debt had become double in Coffee trading business ?

o 187 Cr added for CAPEX requirement that were issued through ECB

What was the company cash balance for the year ?

o 393 Cr

Why company had raised ECB when business is generating sufficient cash flow ?

o There will be opportunity to expand so company had taken ECB for it

Does company had hedge the dollar exposure ?

o No

Why there is huge difference between average sales per day and sales from same store growth ?

o Because of Impact of tax rate from 18 % to 5 %

o Relative Price Competency – Compare to peers company price is lowest

o Increasing in Day part consumption by rolling deserts and increase in footfall

What is the reason behind in jump in receivables ?

o Because of vending business growing and it is not cash business

How industry is growing in machines ?

o Total industry has now 3,00,000 machines all together to whole industry in that company get 50,000 machines

What is the role of distributor in machines ?

o Distributor collect money for the company and if there is default then that is distributor problem

What about delivery business from Cafe ?

o Company had crossed 8 cities and doing it in 345 cafe . It contribute 8-9 % of total Café revenue

o Food is significantly higher in delivery business

o In next 3-4 year at least 20 % of revenue will came from delivery business

Kindly provide detail on acquisition of Pharma Logistics ?

o Company name is PATCAM . It will take 3 years to acquire the whole

o Company had just entered in the pharma logistic market . Company generate 140 Cr from Pharma logistics , retail logistics , food logistics last year. In FY19 it will grow substantially .

o Sical is planning for bulk logistics

o Total compensation for acquisition will be 10 Cr rupees which will be payable in 3 years .

o Company also planning for a cold storage logistics . Company have cold transportation for pharma and non-pharma products

What was the amount of two big order that company got in Q4 ?

o Company got total three orders

• One will start after 18 months that will generate 10,000 Cr of revenue for company for a period of 20 years partnership with Damodar valet corporation ltd with 51 : 49 % partnership

Is there high volatility in coffee prices ?

o No it is very stable

What is the incremental sale after introduction of Day menu Cafe ?

o It had just started in 250 stores . It is introduced to specific stores where clientele demand is there and it result in increase of 4-5 % of sale from the Café

When will company reach rental income of 200 Cr ?

o In next 15 months company will maintain the same run rate of growth so most probably by FY20 company will reach 200 Cr of rental income

How to increase products in brand name ?

o Company is the second biggest brand in food category . It can be expanded well . Company is also well expanding in Tetra pack milk . Company had also introduce some shakes and fruits flaours . All these will lead to 15-17 % growth of revenue going forward

What is the model of rent ?

o 21 % of sales will be the maximum rent

What does company take from customers per machine ?

o 25,000 rs as deposit and no deposit from big customers

Why there is a jump in CWIP from 55 Cr to 81 Cr ?

o 41 Cr is because of roasting plant and rest if for Café which are under maintenance

Coffee Day Enterprise Ltd

Highlights of Q1 FY19 results

Financials

Revenue grew by 17 % to 11,006 Mn yoy

EBITDA grew by 8 % to 2019 Mn yoy

PAT grew by 15 % to 117 Mn yoy

Retail Business

Gross revenue grew by 14.1 % to 4832 Mn excluding the GST impact

Retail EBITDA grew by 13 % to 786 Mn yoy

PAT grew by 7 % to 105 Mn yoy

Key Highlights

Coffee day network stands at 1742 across 246 cities in India. Company added 30 Café during the quarter

Company ASPD grew by 15.6 % to 15739 Mn yoy excluding the GST impact.

SST came at 10.4 % that record for 26 quarter continuous growth.

Percentage of coffee transaction through Digital stands at 48 % during the quarter.

Total Vending Machines stands at 49,397 machines and added 2,576 machines during the quarter.

Company enter into a agreement with UBER for distribution of food and beverages which will enable company to increase retail sales.

Launching a complete new Menu starting at Rs 29 . It offer 24 delight treats to meet youth requirement. Companies engaging customers by giving festival schemes.

Subsidiary Sical Logistics

Revenue grew by 30 % to 3,692 Mn yoy

EBITDA stood at 409 Mn for the quarter

Received all the approvals for modification of kamraj airport . Company will start generating revenues from next 8-12 months.

Office space expansion is expected to grow in key markets like Bangalore where planning 3.4 Mn square feet which will give rental income of 306 Mn for the quarter .

Over next 8-12 months metro trains will expected to connect rural places which will boost the demand due to faster connectivity in Bangalore.Expected revenue of 200 Cr from Timeline in next 12-15 months

Q&A

Kindly brief on 29 rs Menu that company is going to launch and why now why it was not their earlier ?

o Two things come out in a Research which done by company

Lack of product in CCD for entry level

Emphasis on various kind of Combos which is not value for money

o So this is one of the reason company launch this type of Menu which include 24 products with prices starting at 29 Rs. This Menu will Cater to different day parts and this will have options to Create combo for people. Which could be food and beverages and dessert so this will equivalent company with other QSR and response was good in trial basis, In 4-5 months company will rollover it to all over shops . For example a Cappuccino with a Maska-Bun which price is 29 Rs. So these are available in combo and standalone also and 49 rs is starting price for Combo.

How much company has grown in current quarter ?

o Company is growing 10.5 % YOY.

o At least 10-15 % of growth will come from delivery in next 2-3 years

What is keeping company back to explore ?

o Earlier it was a macro issue but now there is so much of competition but now with 1700 outlet it is hard compete as much as possible is there in the market so to compete the other brads would not be easy. Working on new customer acquisition and that will be company strategy going forward.

What are number of stores company is going to open in Fy19 ?

o 130 -135 stores out of them company had open 30 stores in Q1. Company is also relocating old places in which company had open 10 stores in the quarter.

What is company SSSG?

o 10.4 % and from last 24 quarter company is running positive.

What is company debt level and where company is using the debt money ?

o Holding company debt is 925 Cr and the group debt is 3500 Cr and coffee day global is only 116 Cr and in last quarter it was 27 Cr.

o Increase in debt is use for CAPEX deployment and also looking for some opportunity that company will disclose in next quarter.

What is the target for total blending machines for the FY19 and what is the reason for closure of 1000 machines in the quarter ?

o For the full year 8000 Blending machines will be added by company .

o Company base has now gone to 49,300 machines so there will be lot of rotation because company is dealing with lot of corporates .

What is the gross debt on parent level and coffee day global ?

o 5000 Cr on parent level and 400 Cr on coffee day global level.

What has led to increase in interest cost of 45 % ?

o Company large debt is in ECB and there was sharp depreciation in the rupee dollar parity across 3 Cr go to the depreciation for the quarter.

What percentage of sales is coming through Online aggregator ?

o In all cities company have some Café where delivery happen and in those cafes 7 % sales is coming from delivery business and city wise it will be 3 % and it will raise to 10-15 % going further.

How many cities company has covered for online delivery ?

o 8 Cities and in one year company will cover 50 cities.

Which are the products that added by company in the menu and number of store under renovation ?

o Company will renovate 200 Store and 30 stores will be closed out of them. Company has already launched Cakes under Magical Moment themes at 325 Rs each cake round.

Why was profitability increase was lower than revenue increase ?

o Because there was a salary increase in this quarter so there was low margin.

o There are two aspects on it

One is impact of GST , PRE-GST company was getting some tax incentive which company not getting after GST. There was loss of 9 Cr due to input tax credit.

Second is company is committing quite of new projects right now so there is cost related to this project.

Kindly give brief on Delivery program business ?

o Organized players in delivery market like Zomato , Swiggy and Food panda are targeting market size of 40,000 Cr by FY2020. Company is targeting 50 cities in next 1 year.

What is the break down of Net Debt ?

o Cold Co 900 Cr , Sical 2400 Cr , CDGL 100 Cr

What is the net daily average sales ?

o There is a small growth but company will achieve 20,000 Rs daily sales in next 2.5 year from 15,700 rs today.

What was the impact of GST in revenues?

o Company was collecting GST at 18 % and getting many credits from different sources and when it reduce to 5 % company pass on all the benefit to consumer so that has hit 12 % in overall pace last year.

In total debt how much is ECB ?

o 17 Mn Euro and 45 Mn USD , another 25 Mn USD in Sical.

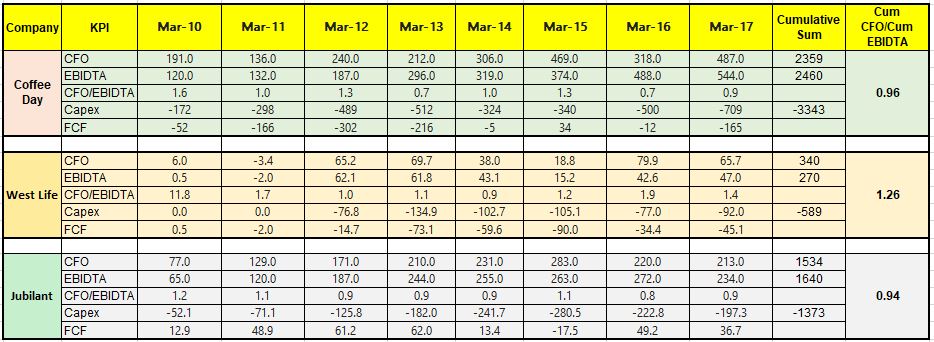

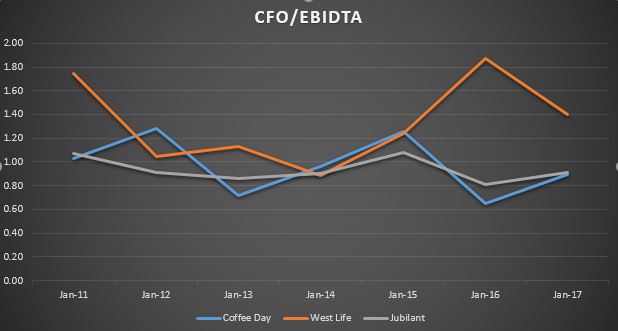

I’ve compared Coffee Day with Westlife Dev & Jubilant Foods. Though it is not completely comparable due to coffee day’s interest in logistics, real estate business, but still I thought of giving it a try.

I’ve used cumulative EBIDTA & CFO to see if Coffee day is showing any deviation. So far I could see that it has been consistent with its peers, though free cash flow to firm is consistently negative for coffee day & Westlife development.

Annual CFO/EBIDTA ratio of Coffee Day is not showing deviation compared to its peers

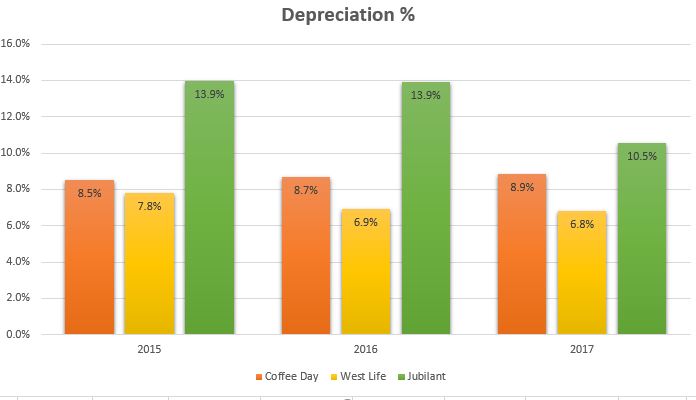

Third, I tried calculating the depreciation rate. Here too I don’t see any volatility in coffee day depreciation, which could have suggested if they are cooking their books. Jubilant shows high depreciation rate compared to coffee day and westlife. Also Jubilant frequently changes the representation of gross block and accumulated depreciation details. I dont understand the reason.

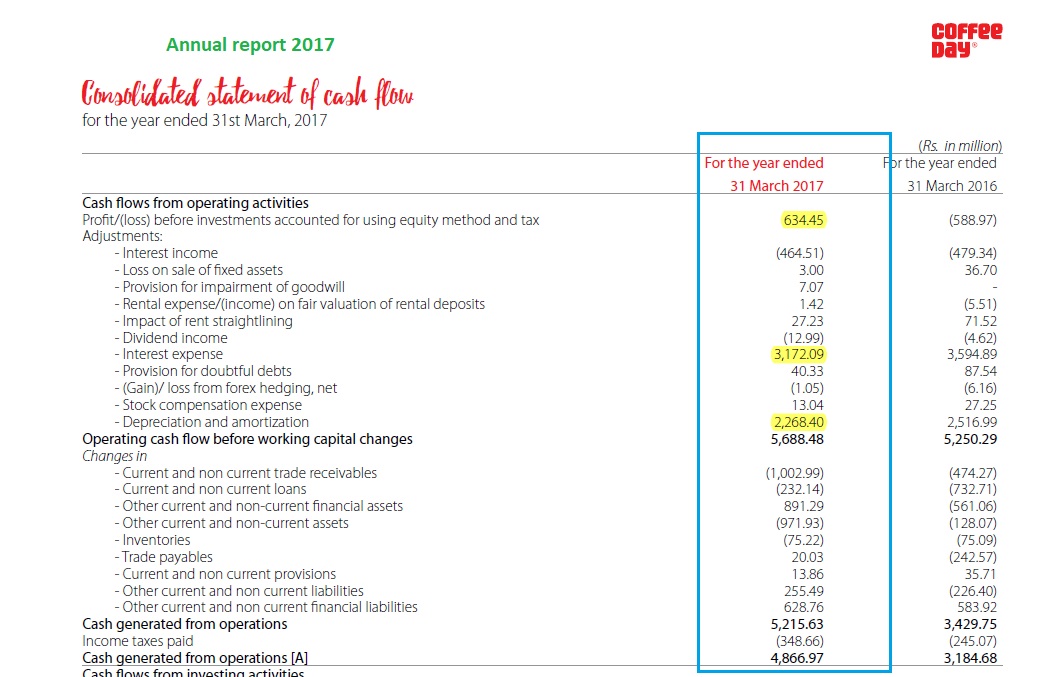

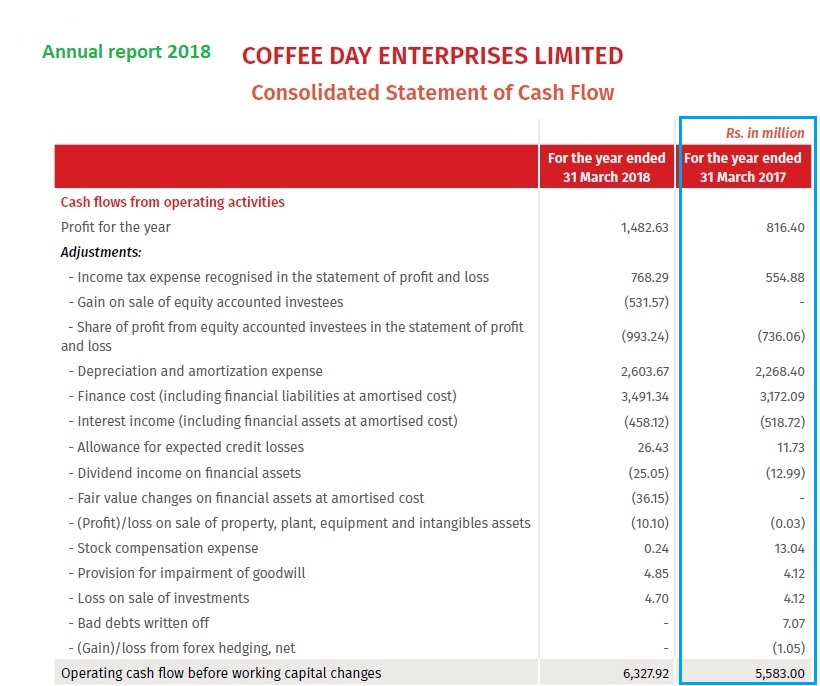

This year there is a change in the representation of Cash flow statement shown by coffee day enterprise. For example the numbers show for FY 2017 in AY-2018 is not matching in AY-2017. Anyone has an idea , why is it so, or is this normal?

I am not invested, but I had my eyes on Coffee Day Enterprises for long because of the success established coffee chains have in the US. But didn’t invest because of the deworsification, debt & pledging.

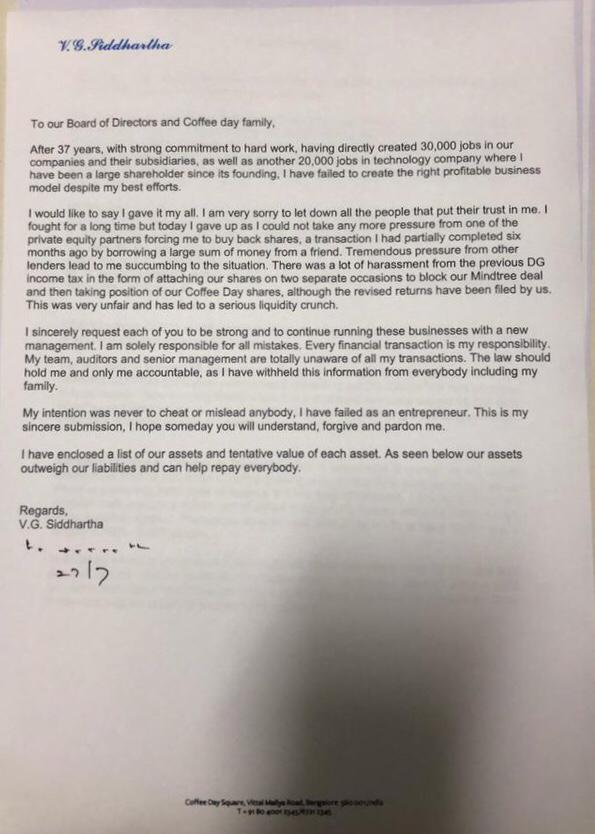

But despite all this, I feel sorry for this man. The sentence “I’ve failed as an entrepreneur” is haunting me. I’ve been one myself and failed at a very early stage despite the best efforts from our team. I can very much understand how bitter it feels when it fails despite wholehearted effort, especially after all these years (CCD was established in 1996).

I’ll pray for his survival. But if the worst happens, will hope some biggie takes CCD chain over & makes it profitable.

Have been reading that last letter from V G Siddhartha repeatedly. I’m pretty sure its not just me but everyone who is an entrepreneur or wants to become one is going to be extremely worried reading it. Have no idea whatever he did was right or not but extremely saddened to see something like this.

This was one of those companies that I felt good about but was never able to make the decision to actually buy their shares. Wondering if the recent news in TOI about Coca Cola’s interest in buying stake in CCD was real or planted.

Very alarming to see the kind of pressure he refers to from PE investor and some income tax officers. Even large businessman like him has to suffer so much. This is changing my perceptions about businesses and debt to a large degree.

I have known people involved in the Coffee industry in Karnataka… Largely employees of Coffee board, Planters etc. It has not been a great industry after late 90s when most of the coffee board employees were sent away with a “golden handshake”. Traditionally coffee has been a tough business to crack. Siddartha brought in a value proposition that seemed to be a “win-win”. It is really disheartening to see a person whom I considered a “visionary” take this path. Some small mistakes compound and eventually take a toll. Also, as per an old interview of Durgesh Shah, the number of shares of Infosys which Siddartha held at a time would be worth more than the marketcap of CCD on the day of Listing.