Everybody must have seen the audit report update on C2C, thank god if you can even exit this

3 Likes

For reference of the forum:

https://nsearchives.nseindia.com/corporate/dhavals_10022025233040_C2CLimitedReviewReport.pdf

This might need some hours to decode the level of cooking done. Heavily cooked books.

Disc: Never invested.

6 Likes

Reading this thread was horrifying. I hope more investors read this and be more cautious in their optimism. Let us learn from the past. I never invested in this as I never found it compelling. But when we do invest, we have a tendency to assume that our thesis is correct despite all evidence against it. Sunk cost fallacy and all.

Hope those who are stuck can get out, specially if this forms a big portion of holdings.

6 Likes

Who would have thought that there can be fudging of books in todays time when the regulations are in place. There has been a lapse from merchant banker. One would assume that when there is an RHP it goes through certain levels of check. There were errors in the RHP and were corrected but one would like to believe that these happened due to inexperience.

I for one was looking at the business prospects over 5 + yrs and chose to ignore clerical erros but was not prepared for cooking up of books. This is a good lesson for all inevstors, including me. Most would have assumed that since big names are on board there needs to be some substance in the company, atleast not expect them to make up numbers. The management has also chosen not to respond to this report.

Hats off to the person who pursued this case.

6 Likes

I had explored this company quite a bit reading up this thread & their presentations, going through their bombastic calls etc. I was totally put off by the insane receivable levels and the (non-existent) cash flows, so thankfully stayed away! Colloquially speaking, ‘baal baal bach gaye’!

It’s a 133 pager and should make entertaining (for those who have not invested) reading but if someone needs a summary here’s one from Notebook LM:

- Mismatch in RHP vs. Books of Accounts:

- Significant discrepancies were found between the Red Herring Prospectus (RHP) and the company’s books, specifically in related party disclosures.

- Loans payable to C2C Innovations Private Limited were significantly understated in the RHP (INR 13.29 lakhs vs. INR 1,329.02 lakhs in the books).

- Payments (advances) made to KTI Intelligent Systems Private Limited were also understated in the RHP (INR 118.83 lakhs vs. INR 369.40 lakhs in the books).

- Differences existed in the reported loans received and repaid from PVR Multimedia Private Limited.

- There were differences in advances received back from Realtime Techsolutions Private Limited.

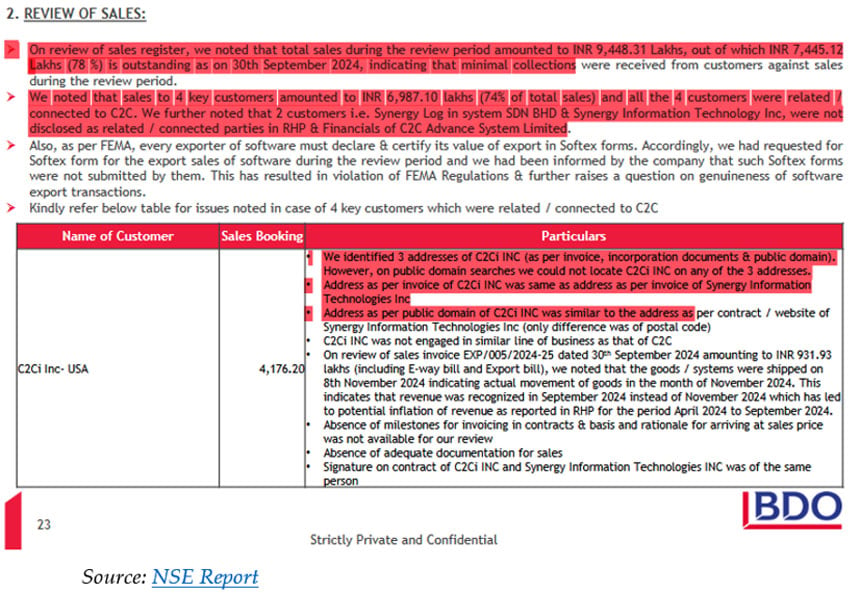

- Questionable Sales Transactions:

- A large portion of sales (78%) remained outstanding as of September 30, 2024, suggesting minimal collections.

- Sales to four key customers constituted 74% of total sales, and these customers were related or connected to C2C.

- Two customers, Synergy Log in system SDN BHD & Synergy Information Technology Inc, were not disclosed as related parties in the RHP or financial statements.

- The company did not submit SOFTEX forms for software export sales, violating FEMA regulations and casting doubt on the genuineness of these transactions.

- The review questions the existence, operations, and genuineness of contracts/sales transactions with C2Ci INC & Synergy Information Technologies Inc. It also calls into question a related order book value of INR 1685.15 lakhs.

- The review suggests potential revenue inflation because revenue was recognized in September 2024 instead of November 2024.

- Inadequate documentation for sales, absence of billing milestones in contracts.

- Mismatched Purchases and Employee Benefits Compared to Sales:

- Purchases of INR 2,403.89 lakhs were made for sales of only INR 1,931.53 lakhs, raising concerns about the legitimacy of these transactions.

- Employee costs were unusually low compared to sales, further questioning the genuineness of reported sales. The review states that employee cost as compared to the total revenue from operations of such companies was around 50% to 65%, indicating unusually low employee cost of C2C.

- Concerns Regarding Advances to Vendors:

- Lack of supporting documents for advances made to Kunal International FZ-LLC, and the vendor’s involvement in an unrelated business, raise concerns about the legitimacy and recoverability of the advance.

- Advance payments were made to Accord Software & System Pvt Ltd and Arihant Info Solutions, but invoices were billed to Realtime Techsolutions Private Limited, with no other supporting documents available.

- An advance of INR 50.97 lakhs to Pythian for software development has been outstanding for over three years, with inadequate supporting documentation.

- Questionable Consultancy Fees and Purchases from RFB Latex Limited:

- The reasons and justification for procuring DGFT scrips from RFB Latex Ltd are unclear, and details of their utilization are missing.

- The company expensed the DGFT scrips instead of showing them as assets.

- Payments were made to directors of RFB Latex Ltd (Ratra family) in the form of consultancy fees amounting to INR 125 Lakhs during March-May 2024.

- Inadequate Documentation for Related Party Transactions:

- No agreements were entered into for loans and advance transactions with related parties.

- Blanket approvals were taken for related party transactions without specific amounts or terms and conditions.

- Realtime Techsolutions Private Limited, with a significant outstanding receivable, has defaulted on bank loans and failed to file its audited financial statements.

- Order Book Issues

- The numbers in the RHP do not match the books.

- There is missing documentation for amounts considered in the client-wise order book against customer OSI Maritime.

- An unconfirmed order amounting to INR 756.96 lakhs was included in the total order book.

- Inaccurate Related Party Disclosures

- The RHP incorrectly identifies the promoter of C2C Innovation Private Limited.

- Synergy Log in system SDN BHD and Synergy Information Technology Inc were not disclosed as related/connected parties.

- Other Issues

- The company was engaged in an unrelated line of business.

- There was a financial default of RTTS not disclosed in RHP.

- There was no evidence of outward movement of goods during sales made to customers for balance purchases amounting to INR 2,210.74 lakhs.

- Inventory records were not maintained in Tally.

In short, it’s a shitshow.

9 Likes

Special thanks to @Nabendu for writing his concerns. Some people must have saved their money because of him. That’s what makes valuepickr forum special. You can always have the opposite thesis.

I was concerned about the related party transactions. But I never thought their books would be cooked. BDO India LLP has done a commendable job. They have gone to extreme lengths to find Google Maps locations, signatures, LinkedIn profiles, etc. Maybe NSE should make these types of audits mandatory for every IPO.

NSE had asked C2C to make this report public (along with their comments) but they never did. Finally, NSE pushed this review report from their end to the exchanges.

8 Likes

Came across the c2cdbsystems, where the COO and CTO of c2c advanced systems were part of leadership team . What is the relation of this entity

http://www.c2cdbsystems.com/about-us.html#leadership_scroll

The products and services, domain knowledge etc. of the company looks fine hearing their interviews and conference presence and researching through this industry.

They are trying to refute the allegations and asking for 4 weeks time to reply to all the observations. Hope they can come out with some reasonable explanations…

but within 4 weeks the price damage would have been already done.

let’s see how soon they can respond.

Disclaimer: invested

1 Like

Hi Guys,

While this is not a post on the C2C , it is more of a reminder for all of us to not get into stories posted on ValuePickr without researching from your side on the story. Its easy to trap gullible retail investors , so all the posts need to be taken with a pinch a salt.

This post is not to stir up a controversy but a reminder that you should not fall into the trap of someone else conviction .

18 Likes

https://nsearchives.nseindia.com/corporate/C2CAS_10062025174311_C2C_ADVANCED_SYSTEMS__MOU.pdf

C2C Advanced Systems signs MoU with Adani Defence to co-develop advanced defence software solutions targeting $20B market.

Memorandum of Understanding (MoU) with Adani Defence Systems and Technologies Limited: #C2C Advanced Systems Limited has signed an MoU with Adani Defence Systems and Technologies Limited, a leading Indian defence company specializing in unmanned systems, drones, counter-drone solutions, missiles, small arms, ammunition, aircraft services, and defence electronics. Strategic Objectives: The partnership aims to develop and deploy advanced command and control (C4I) solutions, computer vision, digital twin systems, multisource data fusion platforms, and AI/ML-powered analytics. Focus on addressing the needs of key stakeholders, including the Indian Armed Forces, Ministry of Defence, Ministry of Home Affairs, and global defence/surveillance entities. Leverage C2C’s proprietary MAGI-C4ISR platform for enhanced command, control, and situational awareness in asymmetric warfare. Key Systems and Solutions: C2C has developed specialized systems for Navy, Army, Air Force, Autonomous, and Space domains, including: Radar data distribution and displays Electro-optical systems Electronic warfare subsystems Sonar subsystems Tactical data links Direction of Artillery Fire systems Navigation support systems Integration of these systems using the MAGI-C4ISR platform to deliver superior mission-critical solutions. Market Opportunities: Target markets include: India’s $20 billion annual military procurement, with 30% attributed to electronics and software integration. 130 legacy ships and 130 additional ships under construction by 2030. Army systems, ISR (Intelligence, Surveillance, Reconnaissance) systems for air superiority, and space-based ISR integration. Geographic focus extends to the Middle East and Southeast Asia. Collaboration Framework: Adani Defence will act as the prime contractor, while C2C will serve as the technology solution provider and subcontractor. A detailed implementation plan has been developed for marketing, selling, and establishing local AI/ML, data fusion, and software solution capabilities exclusively for customers. The collaboration extends to international markets. Existing Relationship: C2C has previously delivered projects to Adani Defence, directly or indirectly, and is actively developing software for anti-drone operations. Impact and Outlook: The MoU is a significant milestone, expected to drive value creation, enhance C2C’s market position, and support long-term growth in India and global defence markets. The partnership underscores C2C’s ambition to lead India’s defence technology landscape.

2 Likes

C2C Advanced Systems Ltd Sahasrar Capital.pdf (992.1 KB)

Shared with the permission of author.

3 Likes

Gentle Reminder…

CFO Resignation Murtaza Ali Soomar- > New CFO acheivements

Heading S/4 HANA Implementations. CFOs are business users they do not head S/4 HANA Impementation Projects

https://nsearchives.nseindia.com/corporate/C2CAS_31052025011520_BM_outcome_V3.pdf

Remember the events .. Do not fall under the narratives ..

4 Likes

Was there any investor concall during last month Results announcement. Please share if there is any recent management call recording available. That is also quite helpful to understand management perspective onr esults and futrue plans. I couldnt find it anywhere

C2C Advanced Systems — Six major events have happened in last 2 months.

-

Delivered awesome Results with 115 Cr Rev and 29 Cr PAT.

-

30crs exports to USA in May month. This shows strong growth in H1 FY26 and FY26 (100%+ growth)

-

Tie-up with Adani Defence on high growth markets - drones/anti-drones, CMS etc

-

Co has significantly expanded its leadership team from 4 to 15 people hence expanding management bandwidth majorly. Some highly experienced and senior defence experts have been added to specifically scout for big defence orders. EPFO website shows significant increase in employee count which indicates company is eyeing for high growth.

-

Co approved Fund Raise up to 143.4 Crores’s through equity and warrants to Fund houses and Individual Investors.

-

Defence Contract Order from Canadian and Broader Western Defence Markets, for delivery of its proprietary Decision Support System (DSS) platform for deployment on a naval frigate. The project involves licensing and deployment of the DSS platform integrating diverse naval sensors and communication modules, worth 42 Crores’s to be completed within 3 months, this is huge for the company.

Source: https://nsearchives.nseindia.com/corporate/C2CAS_07072025190359_JULY_Order_C2C_ADVANCED_.pdf

**In nutshell, there are exciting developments happening in the company and sector. Company received first major defence Order post listing. Defence has long gestation period but once orders start coming then they come big.

8 Likes

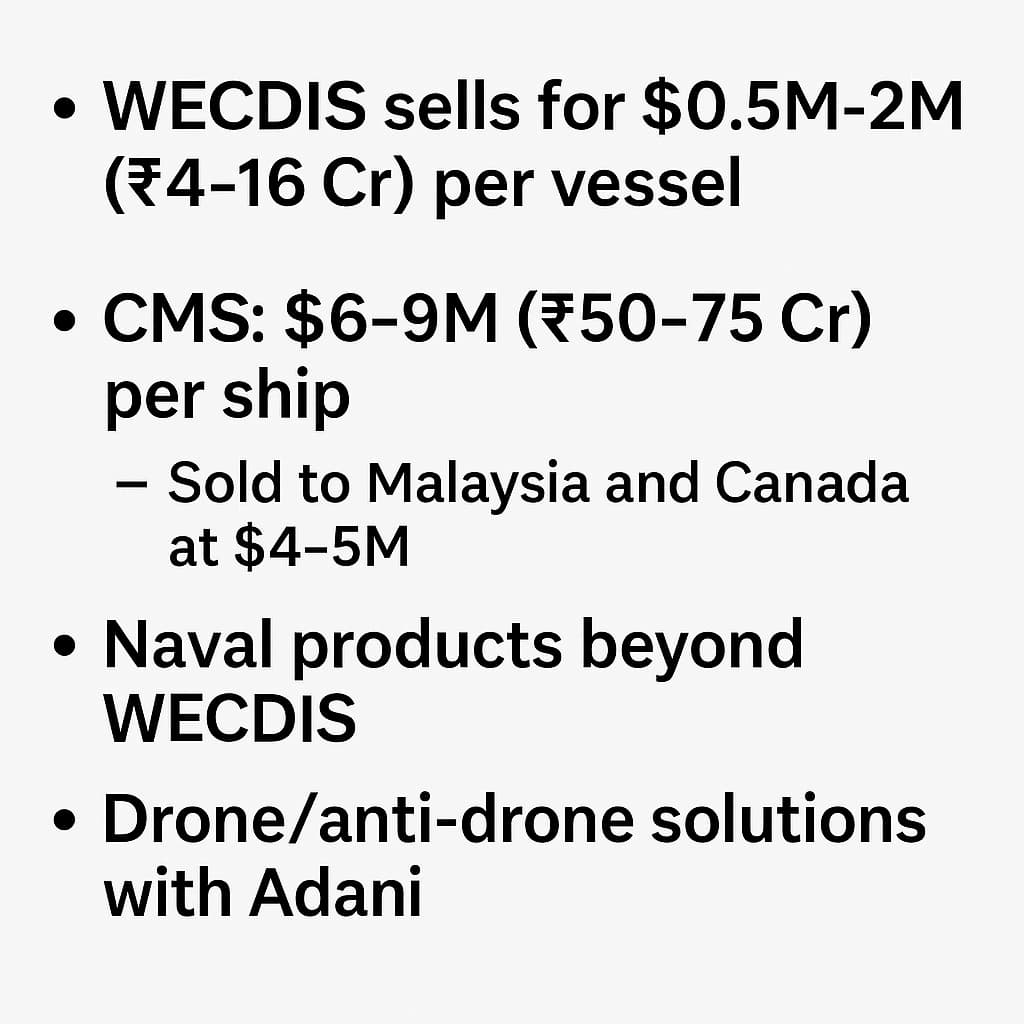

Investors are waking up to C2C Advanced Systems’ true potential in naval tech that per unit of WECDIS is $0.5M to 2M per vessel which is 4 to 16 Crs. I think being a new player they may sell it at discount vs global players.

But, C2C has many more naval products apart from WECDIS. CMS is the biggest product in terms of value which is around $6-9M (50-75crs). C2C has already sold CMS to Malaysia and Canada. The realization was slight lower at $4-5M as these were initial orders (this is 1/3rd price of global players products)

Most investors have still not realised the naval tech/IP capabilities of C2C yet.

And there is huge upside in their drone/anti-drone solutions in partnership with Adani which can be game changer for them.

2 Likes

Is the Canada order for Decision Support System (DSS), the same as a Combat Management System (CMS) which was installed in an old Royal Malaysian Navy ship earlier?

2 Likes

This report looks very concerning. What do you guys think? https://nsearchives.nseindia.com/corporate/C2CAS_04102025193022_Monitoring_Agency_Report_for_the_quarter_ended_March_31_2025.pdf. These are the same issues raised during IPO

1 Like

Anyone know why this company is in a lower circuit since a couple of days?

I think the more important question is how a company with so many red flags from a governance perspective, got its share price jacked up so much.

5 Likes

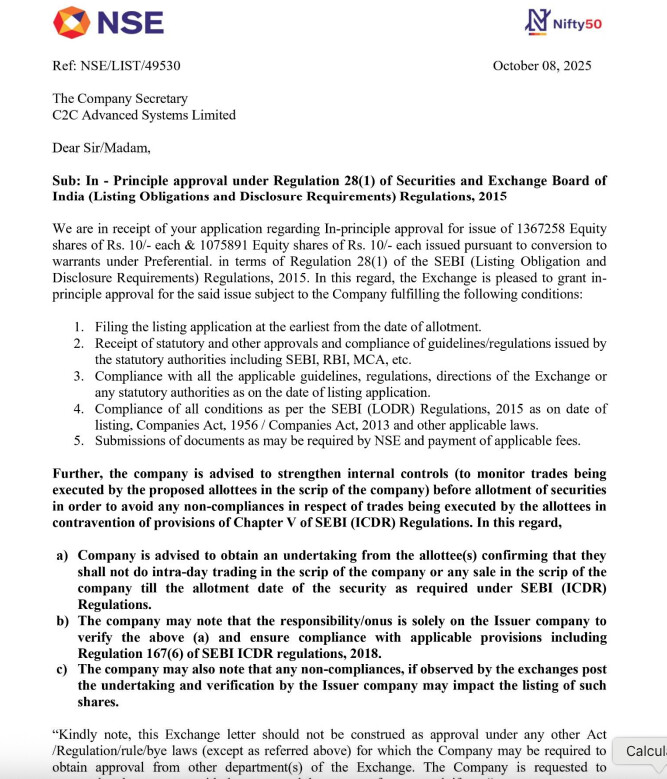

C2C Advanced Systems received in-principle approval from NSE for issuing equity shares via preferential and warrants issue. Now its 100% clear that there are no serious issues in audit resolution otherwise company would have never got the approval. This notification itself proves that audit resolution is on the way and will be done soon. Stock in UC from last two days after NSE approval for Preferential issue, as it clears the way for fund raise.

https://nsearchives.nseindia.com/corporate/C2CAS_08102025151622_C2C_pref_issue_approval_update_F.pdf

1 Like