Confident of improving both OPM and PAT margins by 100-150 basis points in FY 2017

The Byke Hospitality held conference call on 23rd May 2016 to discuss results for the period ended March 2016.

The call was addressed by Vikash Agarwal.

-

For the quarter ended March 2016, sales grew 19% to Rs 68.01 crore. OPM jumped 180 bps to 23.8% which took OP up 29% to Rs 16.16 crore.

-

Hotel revenue grew 18.5% to Rs 37.91 crore and stood at around 56% of total income.

-

Chartering revenues grew 21%to Rs 30.10 crore and accounted around 44% of total sales.

-

After providing for depreciation (up 52% to Rs 4.61 crore), PBT grew 23% to Rs 11.22 crore. Taxation jumped 100% to Rs 3.86 crore as tax incidence grew from 21.1% to 34.4%. Thus finally net profit grew 2% to Rs 7.36 crore.

-

For FY 2016, sales grew 28% to Rs 231.52 crore. OPM jumped 220 bps to 22.7% which took OP up 41% to Rs 52.62 crore.

-

For the FY Hotel revenue grew 25% to Rs 114.29 crore (49% of sales) and Chartering revenues grew 31% to Rs 117.23 crore (51% of sales).

-

After providing for depreciation (up 14% to Rs 11.60 crore), PBT jumped 56% to Rs 39.66 crore. Taxation jumped 157% to Rs 13.73 crore as tax incidence grew from 21.0% to 34.6%. Thus finally net profit grew 29% to Rs 25.94 crore.

-

Room portfolio under owned and leased (O&L) segment totals 677 rooms.

-

During the quarter, in the room chartering business, the number of room nights sold increased from 1.02 lakh to 1.29 lakh y-o-y.

-

Thane Property (Byke Suraj Plaza) Commenced Operations in FY16.

-

The Byke Suraj Plaza is strategically located at high density area.

-

Property taken on long term lease of 15 years

-

It has 122 Rooms, 4 Banquet Halls, 3 Conference Rooms,1 Restaurant and 1 Bar Lounge

-

This property will target high density residential population of Thane, Navi Mumbai and nearby locations specifically for events including weddings, birthdays, and corporate events.

-

This property will contribute significantly to increase in all revenue streams (room rent, food & beverage/ other revenues).

-

The Byke Vijoya, Puri commenced operations in April, 2016. thisproperty will contribute in FY 2017.

-

Byke Vijoya has been taken on long term lease of 15 years. It has 54 Rooms, 4 Conference Rooms, 1 Multi-Cuisine Restaurant.

-

Puri is an upcoming location for destination weddings and other such events in East India.

-

This property will target leisure and religious tourists.

-

The company has identified 8 locations for the next phase of growth. these locations are Dalhousie, Chandigarh, Jodhpu, Udaipur, Lonavala, Mahabaleshwar, Darjeeling and Gangtok. This will further expand its pan India reach.

-

The company hopes to add an inventory of 450-500 rooms through these locations in the next two years.

-

The company will target tourist locations across India in line with current presence.

-

Its Chartering business is seeing continued expansion of network. This will expand reach to customers to get the booking across India.

-

Occupancy of its Lease Business in March 2016 quarter stood at 75.0% against 79.0% in March 2015 quarter.

-

ARR of its Lease Business in March 2016 quarter stood at Rs 4323 against Rs 4463 in March 2015 quarter.

-

Number of rooms of its Lease Business in March 2016 quarter stood at 623 against 519 in March 2015 quarter.

-

For FY 2016 ARR of its Lease Business stood at Rs 3909 against Rs 3783 in March 2015 quarter.

-

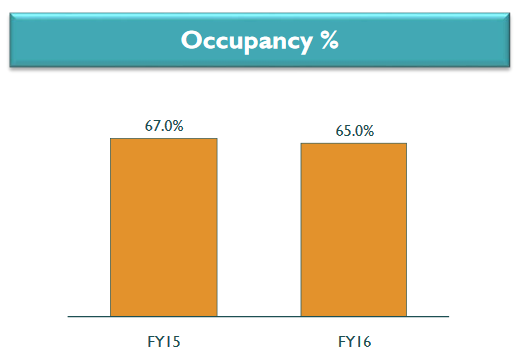

For FY 2016 occupancy of its Lease Business stood at 65.0% against 67.0% in March 2015 quarter.

-

Occupancy of its Chartering Business in March 2016 quarter stood at 94.0% against 95.0% in March 2015 quarter.

-

ARR of its Chartering Business in March 2016 quarter stood at Rs 2340 against Rs 2430 in in March 2015 quarter.

-

No. of room nights sold of its Chartering Business in March 2016 quarter stood at 1.28 against 1.02 in March 2015 quarter.

-

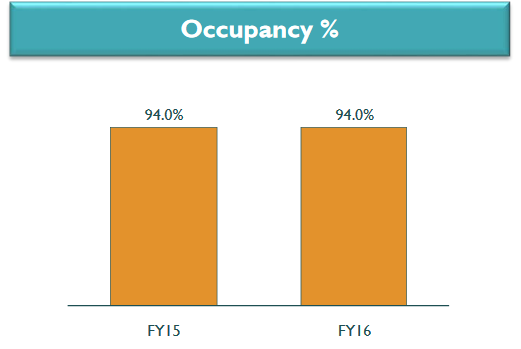

Occupancy of its Chartering Business in FY 2016 stood at 94.0% against 94.0% in FY 2015.

-

ARR of its Chartering Business in March 2016 quarter stood at Rs 2388 against Rs 2401 in FY 2015.

-

No. of room nights sold of its Chartering Business in March 2016 quarter stood at 4.90 against 3.73 in FY 2015.

-

The company had 10 hotel properties operational at tourist destinations in India as on Mar’16 of which 2 are on ownership and 7 are on long term lease. It has total 677 rooms

-

Thane and Puri properties will add 176 rooms.

-

It enjoys niche in vegetarian segment.

-

Its Room Chartering business is spread across 50 plus cities in India.

-

Chartering business has developed relationship with over 150 Hotels owners.

-

The company is well placed to capture Tourism Growth in India

-

The management feels that domestic middle class leisure tourism is set to grow at faster pace.

-

Leased Model offers the company to have low cost & faster rollout of hotel properties.

-

Its Charter model is highly scalable with geography & seasons diversification.

-

It has strong marketing / distribution network of agents

-

Its lease model business has expanded no. of rooms by a CAGR of 31% over FY11-16.

-

It will focus to grow the Lease portfolio aggressively by leasing distressed properties and turning around quickly. The company has successfully turned around many properties. Renovation of the property, one of the key success factors for turn around.

-

Lease business is expected to grow at 20%+ over the next few years.

-

Its Chartering Business through pan-India presence helps in gaining insight on tourist trends, which is the key for selection of hotel properties.

-

Lease model business is highly scalable ahs faster turnaround & consumes low capital cost.

-

Chartering Business has low capital employed and has flexibility to quickly expand depending on tourist trends.

-

Chartering Business is highly scalable and generates strong margins.

-

Net worth stands at Rs 121 crore.

-

Gross debt stands at Rs 11 crore.

-

Cash and bank balance stands at Rs 3 crore as on March 2016.

-

Hotel occupancy in India is 60%. This has crossed 60% pan India for the first time.

-

Tax incidence grew from 21% to 34% because till FY 2015 it had mat credit which was completely exhausted in FY 2015. Going forward it will be around 34%.

-

Shimla property will take time for commencement. It is taking longer due to pending government approval for some renovation.

-

Thane property has occupancy of 55% in March 2016 quarter.

-

The company is targeting operational 25 hotels by 2020 and 50 operational by 2025. By operational, it means that the company will have to sign all agreements by 2019 for 2020 target.

-

Going forward all the quarters will be even for the company as it is spreading itself across India. However, Q2 is generally lean quarter for the company and the industry.

-

The company is almost debt free. It has short term debt of Rs 6 crore and long term debt of Rs 2 crore. The company will become debt free by 2017. It does not need debt keeping in mind its expansion and cash generation.

-

Lonavala and Mahabaleshwar is top segment for wedding functions.

-

EBITDA is at 23% and the company sees improvement of 100 to 150 basis points for FY 2017. PAT margins will also likely improve by 100 to 150 basis points in FY 2017.

-

The company buys inventories in 3 months advance.

-

Depreciation was due to capex of previous year and change in depreciation policy which was adjusted in March 2016 quarter.

-

Shimla and 4 properties out of 8 will get commissioned in FY 2017.