Byke hospitality :

Market Cap: 677.49 Crores

Current Price: 168.95

Book Value: 26.15

Stock P/E: 33.81

Dividend Yield: 0.37%

Stock is 10.00 paid up

Return on equity: 20.20%

Return on capital employed: 25.71%

Debt to equity: 0.14

PEG Ratio: 0.44

Interest Coverage: 15.09

Its been coming up on the growth stock screeners for a long time . Always skipped it when the tag ‘Hotels’ come up. Hotels being capital intensive and a long time to break even.

But Byke hospitality,after 2010 with new promoters it has taken a complete asset light model.

WHAT IT DOES :

Its business model is a mixture of three segments 1) Own & operate 2) Lease & operate* 3) Room chartering*

-

Lease old hotels - renovate it within rent free period - break even within a year - lease forming only 8-11% of costs.

-

Room chartering :Bulk books rooms across tourist & holy places across India - sell it at good margins with 90% occupancy.

In the pipeline:

-

Online portal on pipeline. Set for launch on 2017. Possibility of a tie up with vakrangee for points of service shows its planning and seriousness( From Indian bank research report)

Byke’s director Mr Anil Patodia was a independent director at the Vakrengee ,it could materialise. -

To manage govt tourism hotels on a contract basis.

TRIGGERS:

- 25 lease model resorts in next 3years

- 50,000 room chartering in next 3 years

- online portal by 2017.

RECENT ACTIVITY :

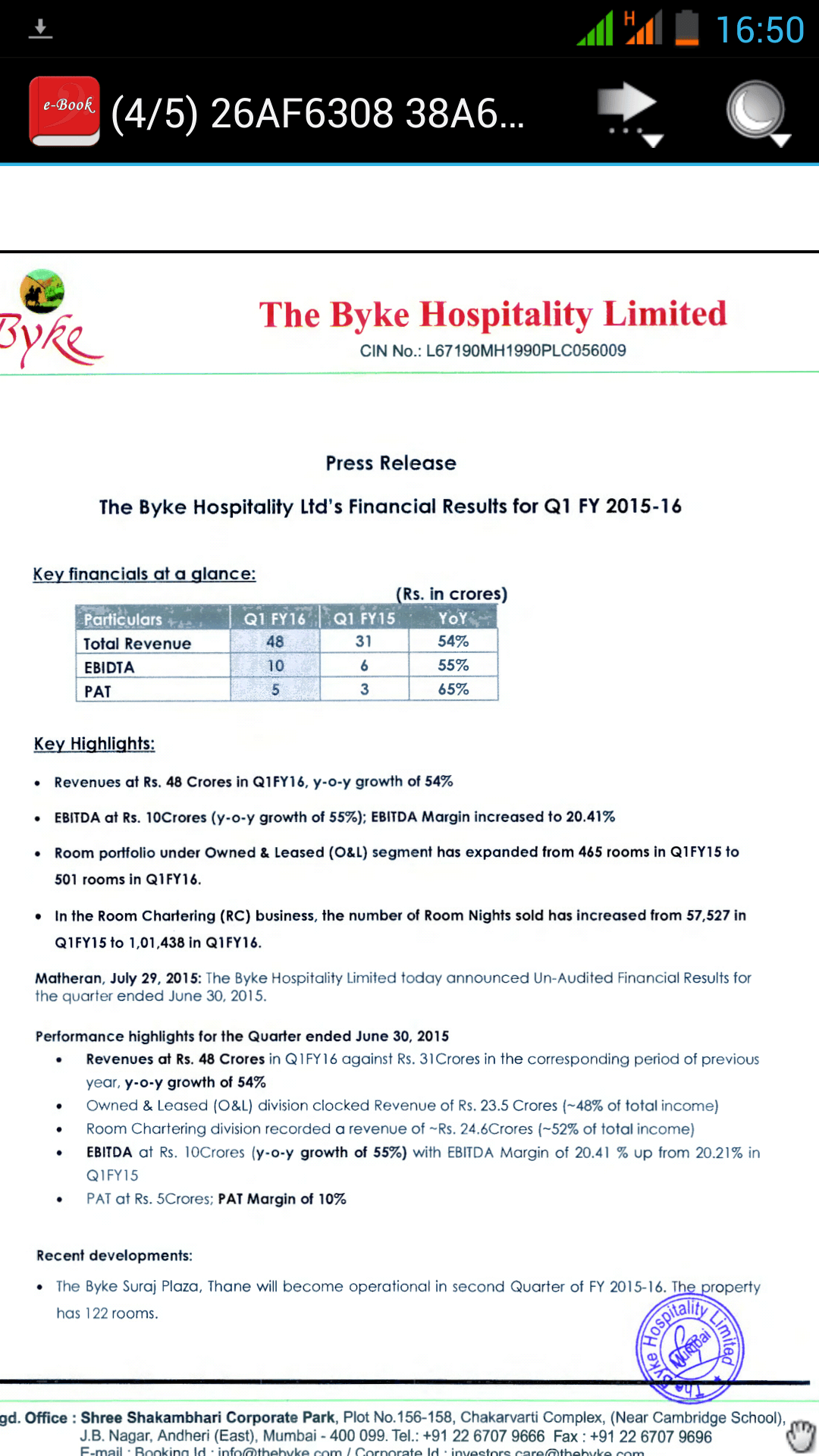

Byke hospitality announced new hotel acquisitions in 2015.

-

Byke suraj plaza at Thane (Mumbai) - 120 room business hotel with three restaurants. This acquisition is on a ‘on lease’ model. Operations to start from this financial year. Other on lease models in Puri, shimla to happen in 2015-16.

-

Hotel in Isle of wight (UK) - Isle of wight is a island at 2 hours distance from London. Its a popular low cost tourist destination in UK. 80% of the hotels in the island are low cost 2 star hotels . Probably byke’s acquisition is of a similar variety. The finer details are yet to come.

RISKS:

Big execution risks.

RED FLAGS:

-

Promoter pledging : In 2013 30% of promoters share were pledged.

But has been gradually reduced to 10% in 2015. -

Other listed companiesof the same group were not successful and have discontinued operations.

-

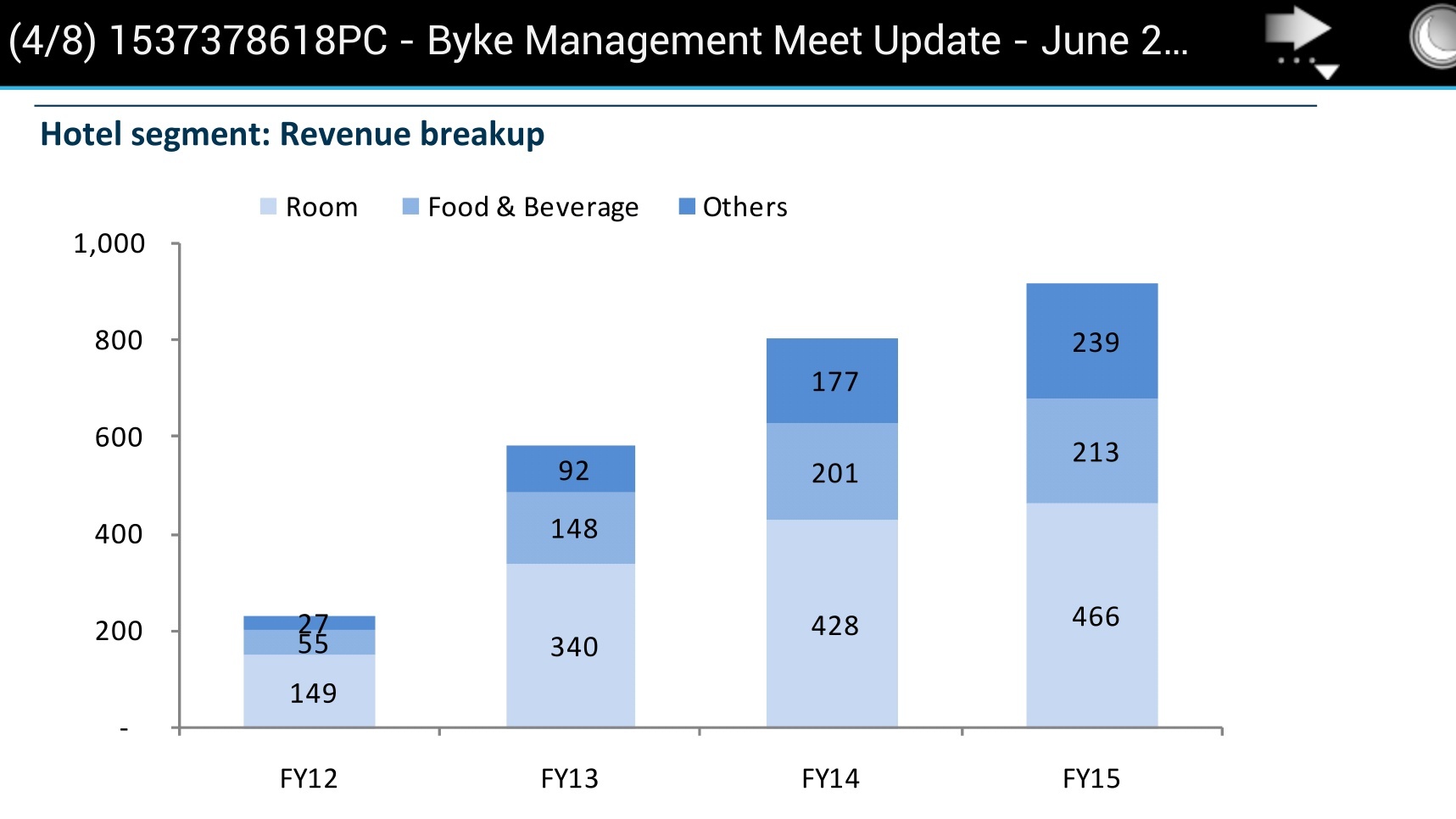

Byke old anchor in Goa with 240 rooms contributes more than 50% of Hotel segment revenues. Any adverse ,black swan event in goa can affect the earnings significantly.

-

Aronda project - Byke had planned a luxury resort offering Naturopathy services targeting foreigners in 2012-13. No info on its expected date of completion is available. Crisil downgraded its rating for this reason. Crisil mentions a 30% cost overrun. This is a complete opposite to its asset light strategy.

-

Isle of wight - Details are not know on how Byke is going to fund the acquisition. Its not a lease model ,so again a contradiction to its asset light claims.

-

Online portal - Byke spoke about it even in 2012, but yet to be functional. In the recent report its been pushed again to 2016-17.

INVESTOR PRESENTATION

The company has a good investor presentation showcasing its ratios. I am not reproducing the ratios here to avoid repetition.

MY VIEW :

• A aggressive management, its past 5 Years is a visible evidence . If management can achieve the stated goals it could be a good run.

• Managements has been doing what it says so far (excluding Aronda, online delay).

• Its goa dependency will reduce in a few year as new hotels are acquired .

• While online portal has been delayed. Byke has been increasing its travel agent count steadily.

• While its other listed companies have failed, none of them lead to any fishy deals( or nothing I could find )

• Inspite of acquisitions it has kept its debt level down. Brings some comfort.

• Pays dividend , however meager.

• Its hardly a undiscovered stock at 35PE, but as a small cap it has lots of room for growth. If it executes its plans, byke can grow at 25%-30% for 3-5 years and stock could do the same.

• Regarding its non - lease acquisitions, probably its impossible to go for only lease strategy in all spots and requires to own a few. Any company info on aronda will be welcome though. The UK acquisition could be a added incentive in introducing membership plans (byke has plans for it)

Scuttlebutt: Nil

Byke Having no presence near my locality I am unable to do any sort of investigation on its services or management. Online reviews are mixed with some complaining that the pool was dirty, offering only veg food etc ( I Dont read much into it. If all online reviews are taken seriously, symphony should have shut shop by now )

Fellow VP members ,senior investors please provide your inputs .

Would love to hear your counter views.

Disclosure - Invested . 3% of portfolio.