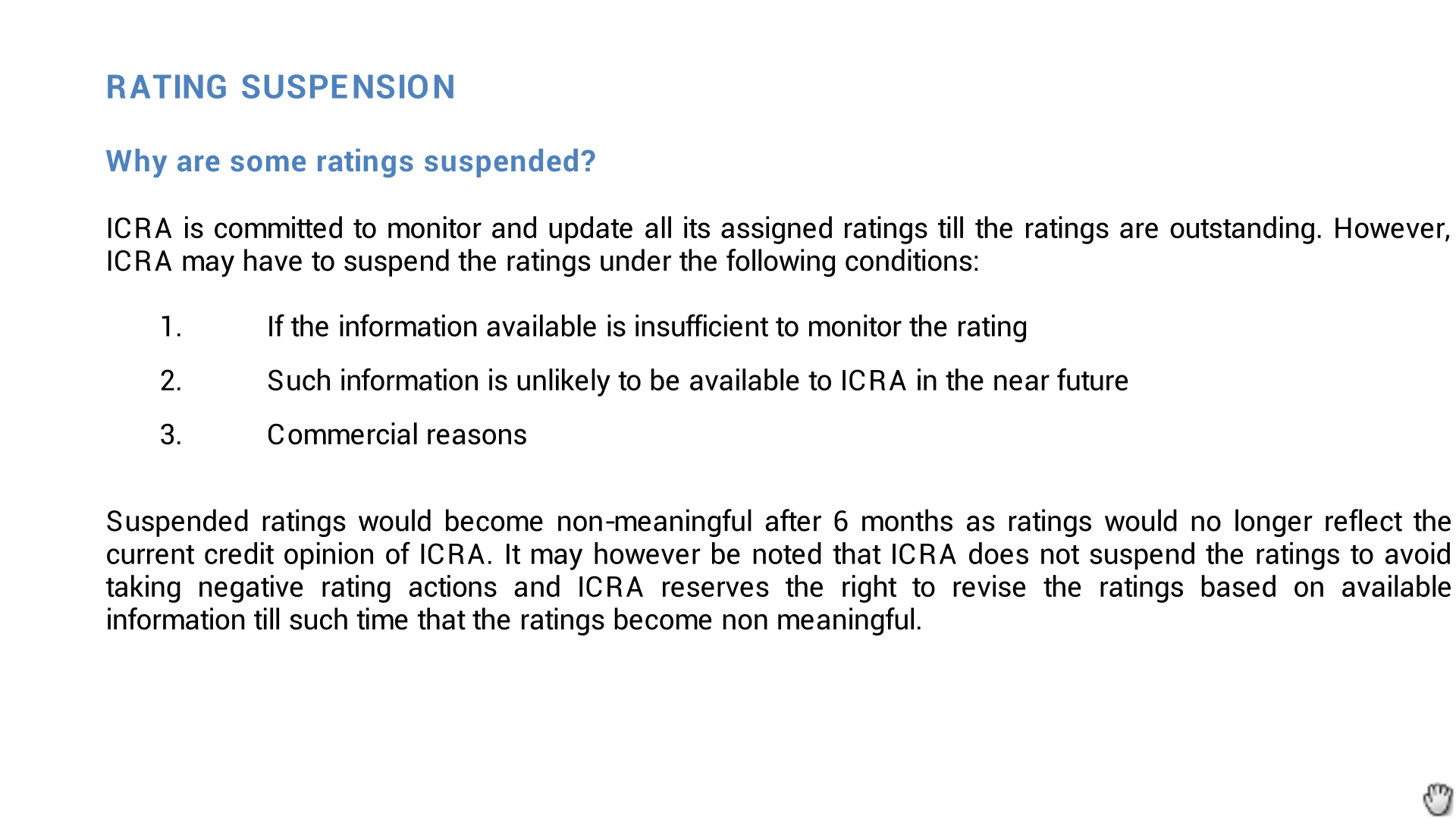

- why icra has suspended rating.

loan is just 17 cr. - thane to open soon.

3 .their aronda project is on hold as approach road not available.they have not invested much in it.land is cheap and no construction. - can any body tell roce they are able to achieve on chartering buisness.

5.they have a team which monitors chartering buisness closely so as to subsquently lease a hotel at a place which they find growing well. - i think giving only veg food is a unique thing. especiallythis is attraction for marriage because of religious reasons especially of north indians and marathis,gujjus.they dont want to go where in kitchen non veg is even cooked.

1 Like

In bykes case the reason provided is insufficient information from the company.

One other case when suspensions happen are when the company decides to approach some other rating agency( discontinues existing one by not providing info).

- But the current loan outstanding is only 6 cr .

- Byke is not looking to raise any fresh debt( as per recent reports)

Hope to get some clarification in the coming AR.

The reason for ONLY VEG is not a religious reason.

In one of the concall, CEO stated that they want to focus on domestic tourist and not foreign tourist. The price point at which they their own rooms are in middle range and Foreigners can easily afford it. But if such an impression develops that this hotel is full of foreigners than domestic tourist with family will avoid this hotel.

The only way to curb foreign demand is to stop serving Non-Veg Food!

They are very focused and clearly want to play on Domestic Middle Class Family tourist who can afford 2k-4k room per night.

- yes the company may see the veg issue like this.but a added fallout of this is religious conservative average middle class person sees it as plus point.they are going for being marriage destination and this fact will play a crucial role.

- also i have feel margins are good for veg food as a whole.less chances of things going wrong.

- would request fellow boarders to comment whether this room chartering business can be considered as a moat for company.also in in case working capital requirement increases for same is it a negative even if most of is managed by internal accrual and not debt.

- domestic travel will certainly increase after seventh pay commission.

Regarding the question of moat/entry barriers , Mr Anil patodia in his own words said room chartering business is scalable but has NO entry barriers .

Bykes business model has no comparable peers. But that doesn’t translate to a moat/entry barrier. For that it must provide some form of differentiated service

• But bykes way of finding prospective properties for lease & run hotels through room chartering definitely gives it a edge over other budget hospitality chains.

• If byke achieves its target of 50,000 rooms for room chartering in 3 years,more importantly develop a working relation with hotel owners throughout the country plus cross selling of its own extended portfolio , byke may develop a ‘network’ effect .

1 Like

where is target for 50000 rooms given and by when.

also having agent network of 220 plus across geographies will take time.

dont think make my trips of the world getting into this

Any insights on the rating suspension issue?

When a company hires a rating agency to issue a debt rating, they agree upon the facilities that the company wants to get rated and the time period for which the rating agency should monitor these ratings. Payment happens at the start of the rating activity and also in installments over the lifetime of the contract. When a company does not see value in getting the rating reviewed on a periodic basis, it gets the rating suspended to avoid paying the rating maintenance fees.

Its alright if the rating was suspended because of commercial reasons. Don’t understand if it was the same in Byke’s case. If not there could be some financial irregularities which the company did not want to disclose.

Disclosure: Haven’t invested, awaiting more clarity on the rating suspension.

Edit: Have written to the investor relations team regarding the rating suspension issue. Will post on this thread once I get a response.

The company has announced the opening of 'The Byke - Suraj Plaza" (Thane). Here is the link to the announcement. The hotel will become operational from 5th September. Thane is not a touristy location, so this hotel must be directed towards business travelers or for occasions such as conferences, receptions, weddings etc. The Q1FY16 investor presentation confirms this. Quote from the presentation:

Targets high density residential population of Thane, Navi Mumbai, nearby locations - specifically for events including weddings, birthday parties, etc.

Property to contribute significantly to increase in food& beverage/ other revenues

Q1FY16 updated investor presentation is available on the website. Here is the link. Sharing it since was not shared previously on this thread.

Some interesting points:

- In the leasing business food & beverage revenue (associated with marriages, conferences, birthday parties etc) is greater than room revenue (12.8 Cr v/s 10.8 Cr). This was not the case in Q1FY15 (7.9 Cr v/s 9.6 Cr)

- Chartering revenue is greater than leasing revenue (24.6 Cr chartering revenue v/s 23.5 lease revenue). In Q1FY15 it was 13.8 Cr v/s 17.5 Cr.

- At 70% occupancy, the lease cost is 6-7% of the lease revenue.

- In the section for ‘Chartering Business’ the presentation says that it has a very low capital employed. I am surprised. Don’t understand how this is.

thanks a lot lynchfan.i think we have a multibagger at our hands.need to dig more.talked to one the management person mr bajaj.he said they will maintain minimum 3 star standards.and have a standard template for all their hotels.

I personally feel, this can’t be a killer multibagger but it’s a safe stock with good growth potential.

This stock will milk the cash in the long run and will give great dividends.

Still, I am in a learning phase and will see what happens.

Disclosure : Entered at 175 levels. 15% of my portfolio.

Hardyboy ,is the Mr Bajaj you refer to the CA Ram ratan bajaj ?One of the independent directors at Byke?

Thanks for your efforts on contacting the management. It certainly helps us all.

yes.anything else you want me to ask them.if they walk the talk of increasing charter rooms from 5000 to 50000 in 3 yrs,then we are looking at good returns.

i am sure seventh pay commision will be game changer for local tourism ,especially 2 -3 star hotels.because of ltc policy and generally more cash available.only 7 percent indians roam per year.mostly during vacation people go to relatives place.other than gujjus and bengalis thereis no culture per se for people to see different places other than religious ones.

all state government and central government trying to boost tourism.i think the segment in which byke is there is going to benefit immensely.

i will request you all to do some number crunching.

i think there model is unique.

2 Likes

Thats great hardyboy !!

I have prepared a set of questions. It would be great if you could get answers for a few

-

Does Byke focus on destination weddings & other wedding related services as a sizeable source of revenue? Does Veg only kitchens help them acquire clients for its wedding business? Do you see the wedding business as one of the growth drivers for Bykes future earnings?

-

The reason behind its proposal to acquire a property at isle of wight ,UK ? Will it be leased or owned?

For leisure tourism or MICR/destination weddings? Do you see more such outside india acquisitions in the future? -

Regarding room chartering : You have achieved high occupancy ratios of 94%. But when we try to scale it up to from 5000 to 50,000 rooms , can the high occupancy ratios maintained? Will Byke be able to find buyers for absorbing it? What extra measures would be needed to maintain the occupancy levels and avoid unsold rooms ?

-

Is there a uniform code or standard of service being offered across all of its leased properties ? Is there a ‘process’, a operational structure being put up to standardize the level of service across its leased properties?

-

Regarding the rating suspension.why was it suspended? Was it a commercial reason to stop getting rating services?

-

Who are Byke’s closest competitors ? a) For its lease & operate properties ? b) For its aggregation room chartering business ? Does it see any of them as a considerable threat?

-

Bykes Online strategy : Does Byke plan to enter the online market in future? If yes . Is it working on some differentiated model / strategies to compete with the existing big players?

( My 4th question is a bit vague, but it would be useful to know if they have a system)

Hope I have covered all the major issues. Please add, if I have missed any.

2 Likes

I Agree with you on the seventh pay commission impact and low base (7% ) opportunity. A recent tourism sector report puts overall tourism industry growth at 10-12% for the last 10years and will continue at that pace. Due to oversupply not all hotel companies are able to show that type of growth.

Bykes aggregation business allows it to play throught all tourist destinations in India, certainly a big cushion + growth driver . Something other hotel stocks do not have.

But there is a significant threat from online players to the room aggregation business. Currently the threat is not big^ , but with improved connectivity and better user online experiences in a few years it will be a significant threat. Hope Byke has a good online strategy to combat that and consolidate its offline bookings share.

( Not big^ - Makemytrip is the leading online booking service provider in India with 40% share. But MMT forms only 5% share of the overall India hotel bookings market. So the entire online booking market is 10-12% only for now. 12% after tons of cash burning of Vc , PE money. Add to it cut throat online competition)

make my trip does not buy inventory of hotels.it is just a booking platform,receiving commissions for the booking.margin is less.byke buys inventory in bulk in off season and sells them in peak season through its agents.also it is to be understood that hotels and customers for make my trip and byke are different.small town people still prefer to go through a local agent their own rasik bhai or amit bhai.byke is still to get into properties which attracts the savvy internet customer.they are in lower segement.its like relaxo vs nike

2 Likes

Sir, Is there anyway to get information on these agents distribution network?

How strong is it?

How have they developed such a successful network?

what are the entry barrier for the same?

Because majority of the business is coming from that channel and goood cash is being generated.

I am not doubting anything here but just want to understand how the whole thing work.

I am new to research field and this is one of the first attempts to understand business…

Thanks.

Recent research report dated 9th Sep, 2015 from Angel Broking. Covered the Company beautifully. Please find below the link

http://breport.myiris.com/ABL/KOTSECUR_20150909.pdf

Porter five forces- competition from Oyo and Zo in the present market may impact the chartering business in a big way. Any comments?

Disc: Not invested yet.

OYO rooms has lot of equity backing up and operates in towns as well .OYO rooms definitely effects Byke kind of companies .

2 Likes

Byke , Oyo are significantly small in size compared to the huge but fragmented market size. Several years of growth opportunities are available. There is enough room for lots of players .

Bykes management in a analyst meet said they are confident of fending of competition from online players because of the high manual intervention still necessary in the room aggregation business.

Oyo’s start up story is really inspiring. Its simplistic standardization is refreshing. But going through the reviews you would find what byke means by requirement for ‘manual intervention’.