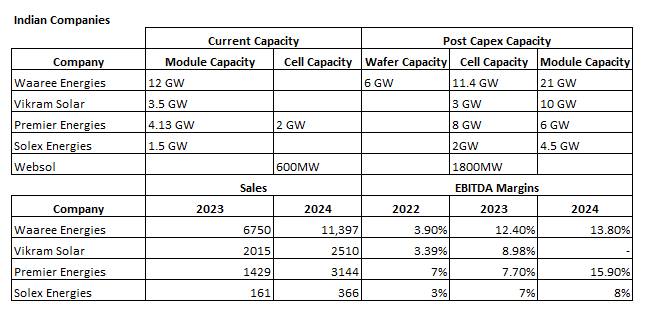

Waaree Energies is one of India’s largest solar module players with 21 GW capacity and 11.4 GW cell capacity. Its EBITDA margin has also improved

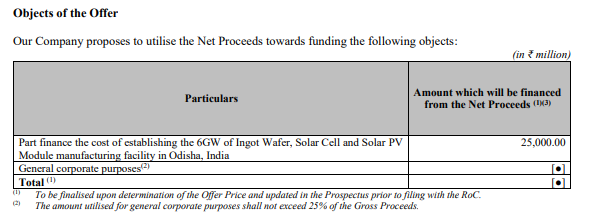

Waaree Energies is setting up a 6 GW integrated facility for ingot wafers, solar cells, and modules in Odisha. The company is benefiting from Industrial Policy Resolution 2022 in Odisha, which includes capital subsidies, power tariff reimbursements, and tax exemptions

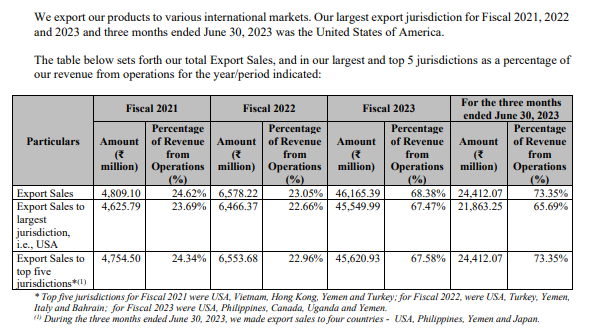

Waaree may benefit from global shifts in solar module supply chains, particularly due to trade tensions between China and major markets like the US and EU. The demand for Indian solar modules is increasing, especially in the US and Europe. As of 2023, exports accounted for 70% of revenues

Huge Order Book

Their order book as of November 30, 2023, was 20.16 GW for Solar PV modules

The company also plans to venture into the green hydrogen market by setting up a gigawatt-scale electrolyser manufacturing facility, targeting sectors such as refineries, fertilizers, and chemicals

Waaree has been awarded ₹19,232.40 million under PLI for its 6 GW integrated facility. The Indian government has set a target of achieving 280 GW of solar power by 2030. Waaree Energies can capitalize on the growing domestic demand

Disclosure: Invested. The above information is for educational purposes and should not be considered as a recommendation. Please conduct your own due diligence before making any decisions

Heard prices in grey market have touched 2950-3000. Preferably they should do a stock split or bonus to keep the value down so that retail participation can increase with more volumes. Its gonna be a blockbuster until current geo potitics and govt policies remain unchanged.

On a different topic for the Vikram Solar investors, price in the secondary market is above 400, i feel its fully priced considering their financials. Do you see this going up further basis IPO approvals? What are your thoughts? Did anyone recently sell Vikram Solar or planning to sell? Selling in secondary markets is time and price challenged. Any platform and hold/sell recommendations basis data and facts would be welcomed.

Also to the NSE investor community, price in the secondary market is between 1800-2k post bonus. With the SEBI amendment on volumes, revenue and profitability would take a considerable hit in the very near future. Is this a time to book profits or partially book profits and catch it lower before or after IPO? Any thoughts would be welcomed.

I don’t think you will get NSE below 1800-2000 after IPO.

Plus when you will sell shares they will hardly give you better price.

And its good idea to book profit as we all know derivatives revenue will be hit by 25-30% but NSE unlisted share takes 6 months to transfer and next 6 to purchase.

So its better to see it as long term investment. It’s my personal view

Thank you Raj ji for taking time and sharing your perspective. I was caught up in two minds, for small time investors the dilemma is about booking profits and wait for NSE to come down which is a certainty considering SEBI amendments with the only question being timing of doing this Vs evaluating the IPO craze for it and few forward looking statements of how the impact would be recovered in Gift or commodity trades cushioning the fall. From a long term perspective, house would always win ( BSE, NSE, CDSL, NDSL) and are steady compounders.

In NSE, while the revenue/PAT degrowth after new regulations is anyone’s guess. What keeps the price up in the unlisted, is the impeding valuation it will fetch once it lists. The price discovery aspect which will come in listed market kind of cancels out the negatives of the degrowth in nos. I think. Let’s see how it plays out.

Thank you Rajpanda Ji, i was caught up in two minds only because of this dilemma. Numbers wise, i expect a significant fall in volumes, revenues and PAT starting Q3, FY25 itself and more visible starting Q4 FY25. With IPO some time away, IPO valuations might get impacted in the short term. Needless to mention IPO price and listing price could be significantly different since owning is an aspiration for many. Larger point was about, raking in the profits and either pre or post listing, on bad days accumulate lower, time will tell if that happens or not.

Couple of days back (post bonus issue ex-date), I was checking the mcap of NSE it was comming approx. Rs. 5 Lkh Crores (i.e. Current price being quoted for unlisted shares * number of outstanding shares.)

Think, looking at a MCAP point, will help in taking a rational decision on buy/sell/hold of NSE unlisted shares.

Recently i studied about polymatech company which is trading in unlisted market.I am analyzing it’s financial statements it seems good to me right now and it is performing well and also growth is seen from previous financial years.if anyone had done any research on this company can you suggest is it worth to buy at this time and also how the growth potential could be in the future in the indian markets as a first silicon vapor manufacturing company in india.

Hello Voldemort - Is this confirmed news? They have their EGM on Dec 9th, will ask them directly. I was tracking a development where Oyo was being valued at 4.6-5B and raising capital at 51/ piece, didn’t hear much after that. Their current financials have improved and they are well on track for IPO in the next 12-18 months, would be curious to hear more about raising capital at lower valuation/price.

TLDR; POLYMATECH claims to be the first indian company to make semiconductor chips. However, there’s a catch - they mainly make opto-semiconductors. These are different from the regular semiconductor chips you might think of

Polymatech electronics is not exactly a semiconductor company, it is in opto-semiconductor manufacturing which means it makes chips for led lights.

It’s DRHP was returned by SEBI as the merchant banker held shares and didn’t disclose it.

There was also an issue of auditor resignation without proper explanation leading to delay in reporting of results.