Long Thread: Long term Weekly and Monthly Setups, good companies, excellent fundamentals, value buys, turnarounds. NOT buy/sell recos. Strictly for Educational purposes.

Jindal poly is the biggest producer of BOPP Films in India. Its new line came on stream in Jan 2021. Company has reported very good margins and profits in last couple of quarters. BOPP films sector is enjoying one of its best cycles with good improvement in BOPP prices.

Technically, stock price broke out post its previous all time high of 695 posted in 2010 recently and went up to post a swing high of 939. After that it faced selling pressure and corrected and seems to be taking support just above previous resistances (change of polarity principle… previous resistances become supports once they are taken out and stock subsequently corrects)

Other BOPP films player Cosmo films is showing good strength in recent trading sessions. disc: bought jindal poly as a techno funda bet looking at chart pattern and feedback on BOPP prices.

Nifty approaching very interesting 2 weeks ahead. Above 14950, it would break the near term resistance and also survive within support line drawn from March 2020 lows.

Fundamentally most of the Nifty heavy weights have declared results on expected lines and state election results are also behind us without large surprises.

GST collections for March received in April have been excellent.

All eyes would be on the covid cases data which if start improving (Mumbai and Pune data already improving) would be the key trigger for the next rally in my opinion.

Sri Kalahasthi Pipes, Monthly - Broke out of monthly close trendline last month but still at resistance levels around 200. Business announced flat EBITDA numbers YoY today (with ~20% topline growth and ~20% bottomline decline). There isn’t much in the price since its trading at around ~4x times EV/EBITDA and a discount to book value (about 2/3rd of book value). Market Cap currently is at 900 Cr.

This discount probably made sense as of last year when it had a large portion of its assets in Account Receivables (541 Cr as of March '20 but down to 225 Cr as of March '21 as of recent balance sheet). The CFO reported is a whopping 549 Cr as a consequence of the working capital changes which isn’t bad for something trading at 900 Cr Market cap. With 520 Cr cash on the books (cash + bank balances + current investments), it perhaps shouldn’t trade at a big discount to book value anymore. The company has paid consistent dividend of about 30 Cr last 3 years and so is trading at about 3.5% div yield.

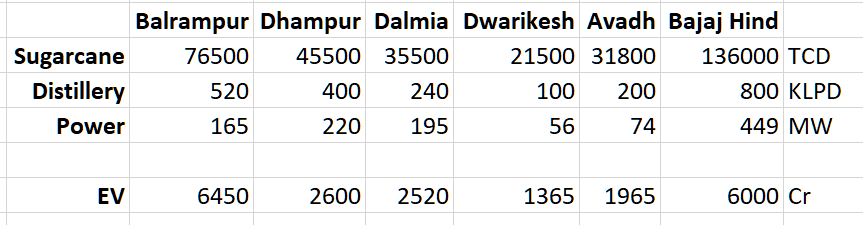

Bajaj Hindustan, Monthly - If Sugar is a bad sector, this is probably the worst stock in the sector. It has the highest debt levels and has taken a massive beating by the market for years. Promoter holding is only 15% and the entire thing is pledged. Most of the public holding is with banks which probably lent it money at some point and are now holding the bag (40% SHP with banks & financial institutions and can be assumed to be sort-of promoter holding). So needless to say, this is very high risk-high reward trade (so position sizing should be appropriate, if at all it looks interesting). It has broken out of a 6 year downtrend few months back and is now showing some life along with the rest of the sector. Today has seen lifetime high volumes and a reasonable 40% delivery (which is good for the volumes)

Valuation is what is even making this trade worth taking for me. From a replacement cost perspective, compared to its peers, it is trading somewhere around 30-50% discount. But this is normal when survival itself is in question and one look at the PnL will tell you this is a horrible business to own.

The PnL has taken a big hit from Interest cost + Depreciation ever since they have undertaken that large capex in FY11-FY12 and has suffered for almost 10 years now for that sin.

However, the silver-lining if there is any is that the debt and consequently the interest cost has gone down over the last few years. Now the Interest Cost + Depreciation is around 500 Cr. EBITDA levels like FY16 in the previous sugar cycle of 750 Cr hence can this time turn into a 250 Cr profit. And a business that is wallowing in debt and poor perception like this stands to gain the most from a cyclical turnaround than the others.

Tata Steel BSL is a classic recent example which played out well for me when the steel cycle turned (If only it wasn’t going to be merged with Tata Steel, the runup would have been even more dramatic with the turnaround).

I have been following your views which are very logical and educational. On TATA steel BSL, latest quarter PAT annualized implies less than 2x PE. I agree merger with Tata steel will hamper realization of value for BSL. But isn’t the merger a long dragging process. I saw the first notification of merger more than a year ago. And supposing Tata steel gets the merger going and comes up with a record date, I am wondering why is the share price of BSL waiting for that? Please can you share your views.

Thanks for the inputs. Let’s see how it plays out. There could be an opportunity cost here if the sugar cycle doesn’t pick up even if downside may not be much.

Merger ratio is already announced. 15 shares of Tata Steel BSL for 1 share of Tata Steel. So in effect the two are tied together now. When I saw Tata Steel BSL at 102 and Tata Steel at 1100 (Tata Steel effective price 1500+), it didn’t make sense for me to hold any longer so I got out. The interesting thing is I bought at 50 after the merger ratio was announced and actually had no idea about it until someone mentioned it. So poor was my research (It usually is)

Some more breakouts

Parag Milk, Monlthy - Broken out of a 3 year downtrend in current month. Valuation is in favor but business hasn’t done much since listing. May not do much but if it does, at this valuation, there is potential upside

Angel Broking, Daily - Came on the radar yesterday post numbers and any which way I looked at it, the 2x Sales and 3x Pat, along with 10 times earnings stood out. Risk is that this is very much a cyclical business in my opinion (ISec is also valued at just 14 P/E). If there is a re-rating, the upside here could be much higher.

Mangalam Organics, Weekly - Has broken out on the weekly with volumes. Its been trading cheaper than peer Kanchi Karpooram though it has comparable metrics. These are simple commodity businesses but there has been a structural shift in this sector which led to good numbers in the last 3 years. This has traditionally been a very volatile stock so tread with caution.

CITY UNION BANK

Looking to form base, bears were weak on MACD in recent price correction that stopped by the March end.

Next Resistance on monthly charts : 200

Support on monthly charts : 150

Bank has yet not achieved the Pre Covid Prices of March 2020.

@sethufan - Thanks for the good charts. Can you please let everyone know what indicator that is? It appears somewhat similar to RSI and similar conclusions can be perhaps drawn from just RSI - If you find this custom indicator better than RSI, it would help us all if you can teach us how.

I see people have asked this before as well but I can’t seem to find any good explanation in this thread. Please point me to it if you have shared. Without that, the knowledge you are trying to share is mere information that isn’t reproducible and learning from it is impossible (Especially since most of the charts are post-hoc). Thanks in advance.

Good looking cup and handle formation on the Axtel weekly chart which is part of an ongoing flag formation. There are other patterns visible to the naked eye too like a triangular consolidation pattern. The price had taken rest on after breaking out the previous resistance level of 285-290 before rebounding. Pattern targets seem to 440-450. Another important aspect is the fall in volume during the handle formation and just not the shape of the pattern.

Bro, is there a screener or something else through which we such can find volatility contraction patterns. Actually, since last two weeks I am trying to make a screener on chartink to search such patterns But still many best setups are not coming in my scan.@bheeshma@phreakv6 . Please help.

BSE Ltd, Monthly - Though it got out of the long downtrend of 3 years, it has taken 1 year in a rising wedge consolidation which it has broken out of, this month (can be confirmed only by end of month). Fundamentally not a great business though there can have temporary tailwinds since there is increasing churn in smallcaps/microcaps with the retail participation (Most of these are listed only on BSE). Also last few months, brokerages like Zerodha have been defaulting transactions on BSE if you are not too careful. Valuation is in favor if you take into account the cash in the books and the CDSL stake. Not entirely sure how well the Star MF business is doing as I stopped following this for sometime now.