Need suggestion to learn.

Deepak nitrite seem to have broken out with big volume. Can we enter with SL at 540 or shall we wait for retracement or confirmation?

Need suggestion to learn.

Deepak nitrite seem to have broken out with big volume. Can we enter with SL at 540 or shall we wait for retracement or confirmation?

Breakout on heavy volumes is a strong confirmation…im entering on monday

That’s a cup and handle Breakout …looks like u can add some at cmp and add some if it retraces

What about hle glasscoat. Looks like further high to be achieved. Not high volumes but everyday making high and then retracing.

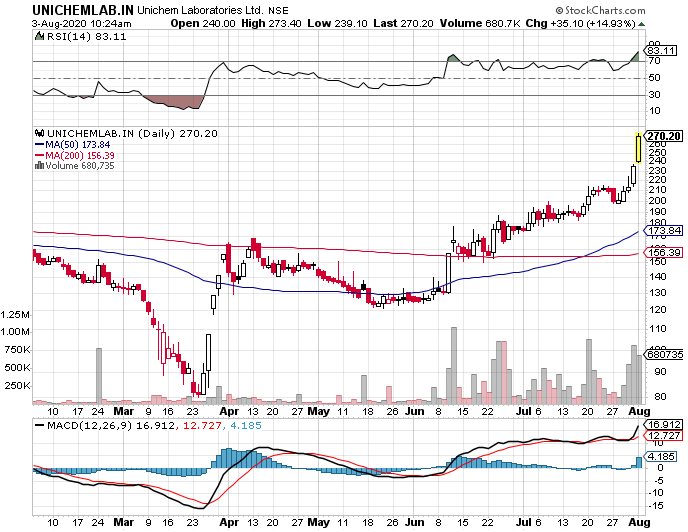

Hi. On what indicators or parameters it’s looking good. I think breakout is still pending. And it has been a Laggard stock since years in Pharma pack. Even when pharma was performing really well during 2015 I think it has reached 80 or so. Unable to cross 100. This time their new plant needs to be operationalized soon which could add to revenues in coming years. Let’s see at least in this pharma bull run it performs well

Hi Alkem has lost weekly support and hence to say correction is over is little bit tricky here. I have given the chart it needs to show strength above red line.

Deepak Nitrite Technicals ! https://in.tradingview.com/chart/DEEPAKNTR/16SYZAE5-Deepak-Nitrate-Long/?amp

InfoBeans breaking out after quarterly results

The Nifty’s P/E is at 30, and the EPS is around 365. With a lot of money moving into gold and silver, and the US Fed refusing to raise bond yield rates, does it look like a correction in the Nifty is coming? Also, the geopolitical scenario is in turmoil, the economic macro indicators aren’t too strong both in India and the US. And corona is just messing up all long-term projections and plans.

I just wanted to put this out there, to invite opinions. I don’t mean to spread doom and gloom, far from it. Do comment,

Thanks.

Sugar has been in news for some time:

1.Govt notifies 10k tonne of sugar export quota for EU at concessional rates | Business

Some interesting sugar stock charts to track:

Disc: Charts only for study purpose.

It has a resistance in 119-121 range, it gave almost 20% return in 4 days, 50% of profits can be booked

Tata Consumer, Monthly - Sort of a C&H breakout on the monthly. Very good performance by the company in Q1 driven probably by some one-offs in Coffee and Tea stocking worldwide. There could be some near-term margin pressures on tea as well. However the India Foods segment which the company acquired from Tata Chemicals is doing extremely well. The Tata Sampann range is gaining handsomely (growing at 50% in Q1) in a very under-penetrated segments like branded pulses, spices, ready-mixes etc. Out of the 30L Cr market size in the Foods and Beverages in India - only 10% is currently Organised. So the pool size is very large to grow into and the lockdown appears to have given it some impetus as they are gaining market share through e-Commerce.

This could be a bit more structural and the business has grown very well digitally under lockdown as seen by its traction on Amazon Pantry (Bestsellers in most categories) and BigBasket. There is very good margin expansion this quarter which the management thinks can be sustained and bettered as the integration synergies between Foods and FnB businesses kick in over the coming quarters and the company aspires to become a full-blown FMCG company - can see this in lot of references in the ARs and concalls regarding the same and its showing in their inspirational expansion into new categories and brand-building.

Disc: Invested. Looking to add over time.

TVS Srichakra breaking out on Daily Charts

result was stellar infact. whats your take going forward? what is the upside you are expecting? or market is already priced in

Sun TV, Monthly - Breaking out. Numbers have been hit with lower ad spends in the last quarter and also because of last year Q1 having IPL revenues. This year IPL revenues should flow in Q2 and Q3 and so will the ad spends. Their subscription revenues are growing well. Valuations are very attractive at 13x (subdued) earnings and a Div yield of close to 6%.

KNR Cons, Weekly - Breaking out with volumes this week. This is one of the decent players in the infra space. They are into road as well as irrigation projects (Almost 50-50 split). Last quarter numbers were very good with EBITDA growth given the circumstances. Current Order book at almost 3X FY20 Sales and between Q1 and Q2, Order book has almost grown 50% a bulk of it from Irrigation projects. Their WC management is by far the best in the industry and they haven’t even opted for moratorium during these times. I think we are getting into a low interest rate, weak dollar environment which should flood EMs with easy money which should make erstwhile unviable businesses more viable now due to the lower cost of capital - so I am somewhat positive on the Infra and Construction space, especially due to the valuations. This is a theme that can persist for some time and is not specific to KNR alone.

Nocil, Monthly - Anti-dumping duty play. There is a anti-dumping investigation initiated in May against PX-13 dumping (Should make up about 40% of Nocil’s topline). Given the current protectionist environment it is highly likely to play in Nocil’s favor. Attractively valued as well.

Thirumalai Chemicals, Monthly - Similar play as Nocil. Anti-dumping investigation on Phthalic Anhydride dumping from China initiated in May. Very likely given the sentiment to work out in company’s favor.

Disc: Have positions in all of them from sometime this month.