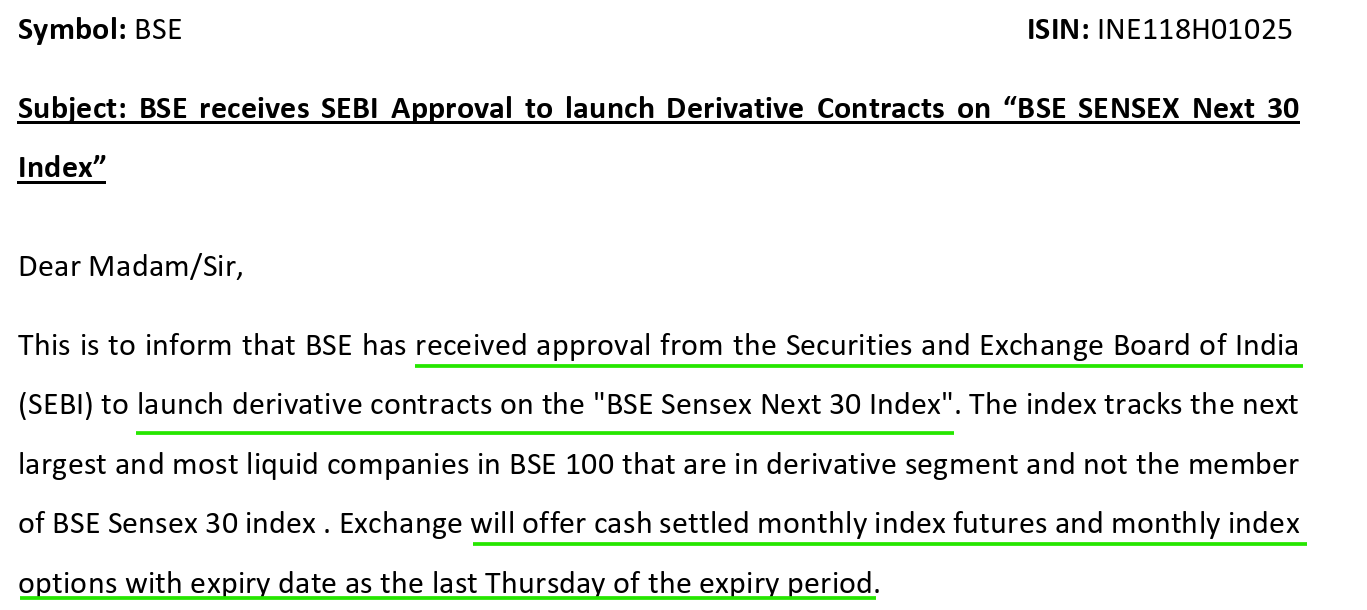

https://nsearchives.nseindia.com/corporate/BSE1_09022026183921_NSEIntimation.pdf

Q3FY26 Result.

Notes from Q3 FY26 concall:

Disclosure - Invested

Fantastic results….also nse sent delegation to sebi today to lower stt….lets see what happens.

This is a Qoq business and growth has normalised and current valuations baking in much higher growth. This quarter is rather a miss if you compare it to the growth inbuilt. The base effect has come into play and with increase in STT, this will become challenging to get further rerating. Already trading at premium to NSE.

It seems STT needs a more nuanced view than anticipated. Do not think representation to the govt will make much of a difference.

SEBI’s decision to stall new exchanges from entering the equity options market unless they first build meaningful cash-market depth effectively limits further fragmentation of liquidity in an already concentrated derivatives ecosystem. By keeping out potential new competitors, the regulator reinforces the incumbents’ advantage, ensuring that order flow and volumes remain focused on established platforms. For BSE, which has been steadily scaling up its derivatives franchise, this is structurally positive: reduced competitive noise improves the odds of sustained market-share gains, better liquidity stickiness, and higher operating leverage in one of the most profitable segments of exchange businesses.

Yday BSE declared the Q3 results.

The results were on expected lines, Earlier in Jan I had expected revenue from derivatives to be around 784Cr in Q3.

Q3 Results PDF, Q3 Presentation, Audio Recording Link - https://www.bseindia.com/downloads1/28323b6b-12c4-4416-ade7-9dc277de2e14.mp3

Going forward the path gets tougher, BSE has made commendable inroads into options segment in derivatives, and I think the low hanging fruit picking is mostly done. I also see a slew of analyst reports with aggressive price targets + the NSE listing floaters. Time to be cautious.

Having said that, BSE needs to work on new areas to find similar growth. ![]()

MSEI officially refutes Reuters article.

PR-ENGLISH-10-FEB-2026-CLARIFICATION…-CLARIFICATION…pdf (782.8 KB)

I posted a tweet on the STT issue. Not sure what the Metropolitan Stock Exchange of India Limited (MSE) has to do with it. I did not understand. Why the tag?

it was mistake on my end.![]()

the doument I shared was from the MSEI website refuting claims bout SEBI stalling MSE’s entry in options market.

Big Blow for FnO Volumes Going Forward. EPS will get downgraded. Jefferies estimates that the new RBI norms may impact 10-12% of options trading volume, which could lead to roughly a 10% hit to BSE’s earnings.

query - how and when can exchange increase charges?

Yes, they can and do increase or revise charges on products like cash and derivatives. I remember When BSE brought back Expiries on Sensex and Bankex; they offered fewer transaction charges on it than NSE to make it lucrative.

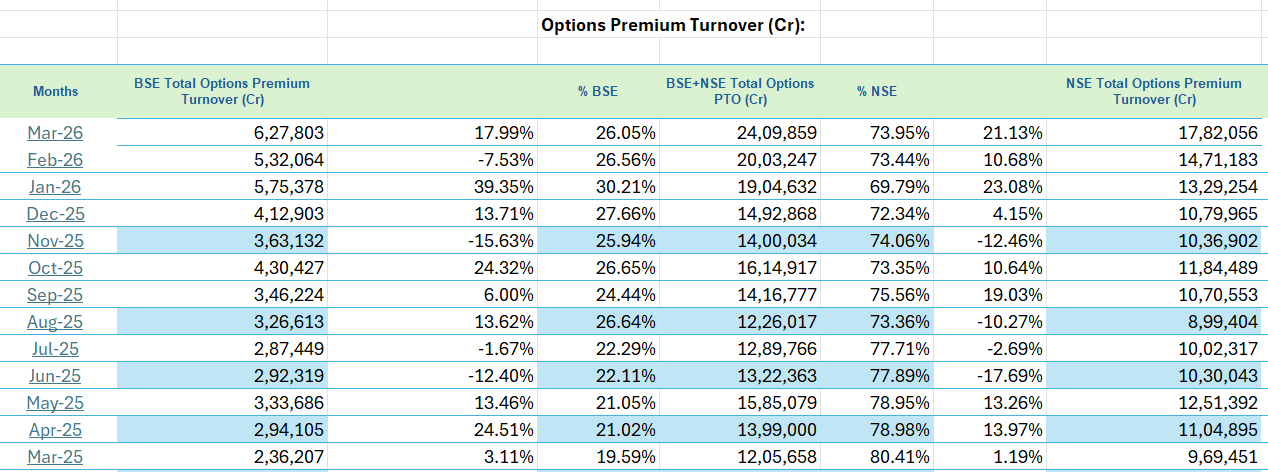

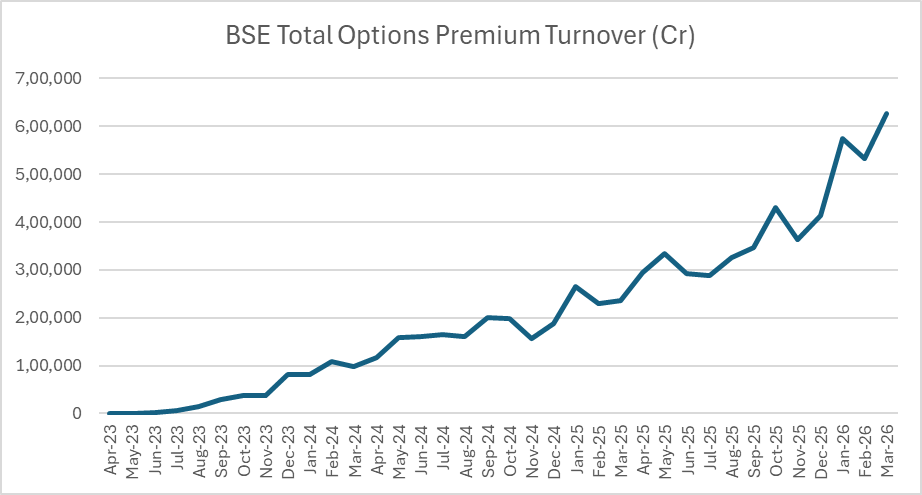

Intermediate update : Jan + Feb PTO is ~30+% higher than previous qtr. For these two months revenue from derivatives is ~719Cr (internal calculation) compared to Q2 784Cr revenue. High probability revenue might cross 1000Cr if similar daily PTO is maintained.

Jan-Mar 2026 Q4 update:

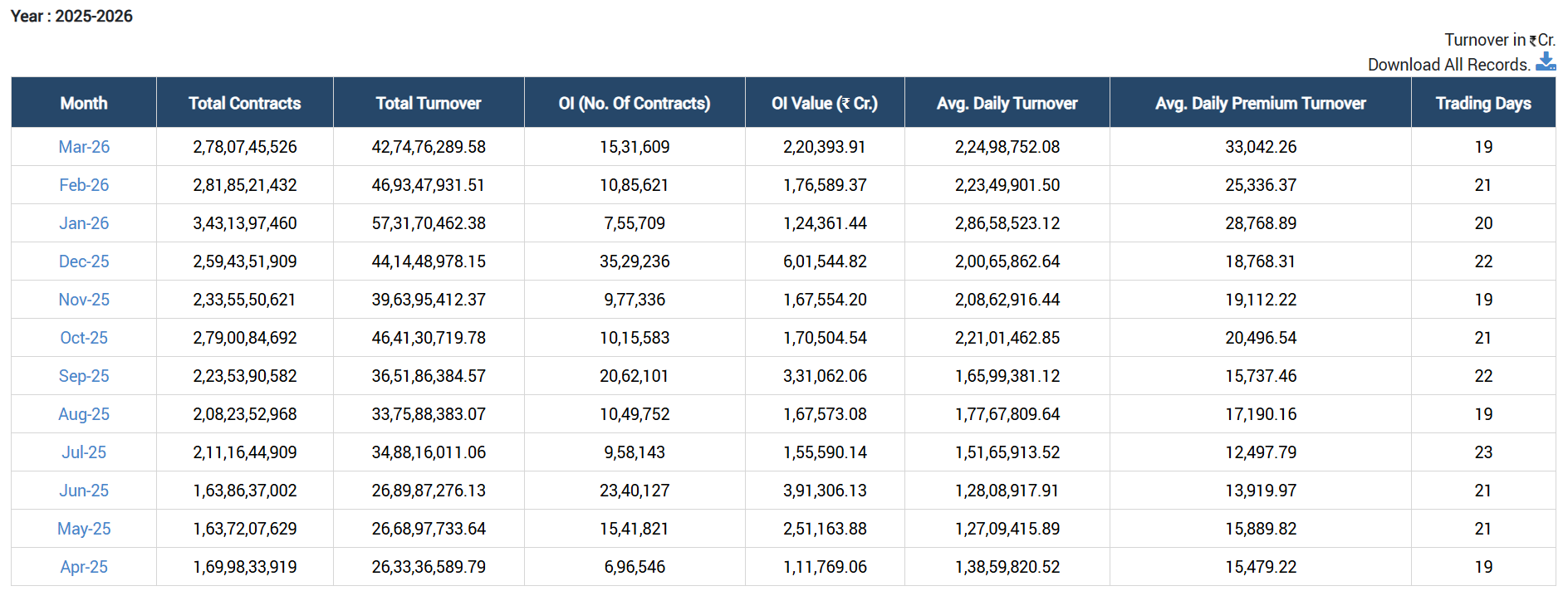

Edit: Average Daily Futures Turnover is hitting ~1000Cr/day mark now. Seems interesting, since Dec 2025 it was mainly in the 100-300/day range, and has steadily moved up to start hitting the ~1000/day mark regularly in last week or so. Also, BSE has been quick to change the Monthly summary to include the “Average Daily Futures Turnover” number, seen as 1,296Cr for first 2 days of April.

Update for Q4:

Derivatives: The average daily premium turnover was approximately 28,917 Crore as compared to 19,450 Crore for Q3 - I expect the revenue from this segment to grow by approximately 40-45% as compared to Q3 to reach between 1050-1150 Crore.

Star Mutual Fund: The mutual fund numbers continued to grow as compared to Q3 with total subscription orders hitting a new all time high of 22.4 Crore as against 20.2 Crore for Q3. I expect the revenue to be approximately 10% higher as compared to Q3 to reach above 75 Crore.

Equity segment: Segment has picked up some traction after a poor Q3. Revenue should grow by roughly 10% as compared to Q3.

IPO Market: Understandably the IPO market underperformed during Q4 due to marco concerns - this quarter about 38 new companies went public as compared to 60 during the previous quarter. The revenue from this segment is likely to dip by about 40% as compared to Q3.

Colocation business is expected to continue showing good progress - they should have reached the goal of 500 racks by March 2026.

Overall, I expect the standalone revenue number to be above Rs. 1500 Crore with net profit exceeding Rs. 750 Crore subject to any one-off’s.

AJ

Disclaimer: Remain invested. Consider my views as biased.

While Q4 seems to have been widely known, can somebody highlight the trend in derivatives post STT hike from April 1?

this has fallen to 749.61 crores/day as of yesterday