There has been some speculation on traders shifting away from NSE, etc. I was wondering the accuracy of these reports, and did a mid month check on BSE volumes over the weekend. Since BSE had 1 expiry more than NSE last weekend, decided to wait till Tue EOD to complete the check. As of Tue night, 13 trading days have completed with 3 expiries on each exchange.

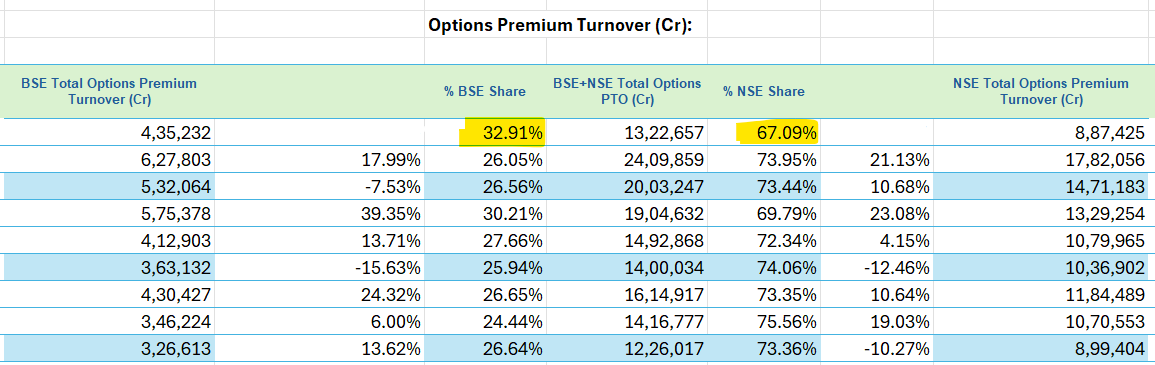

PTO market Share:

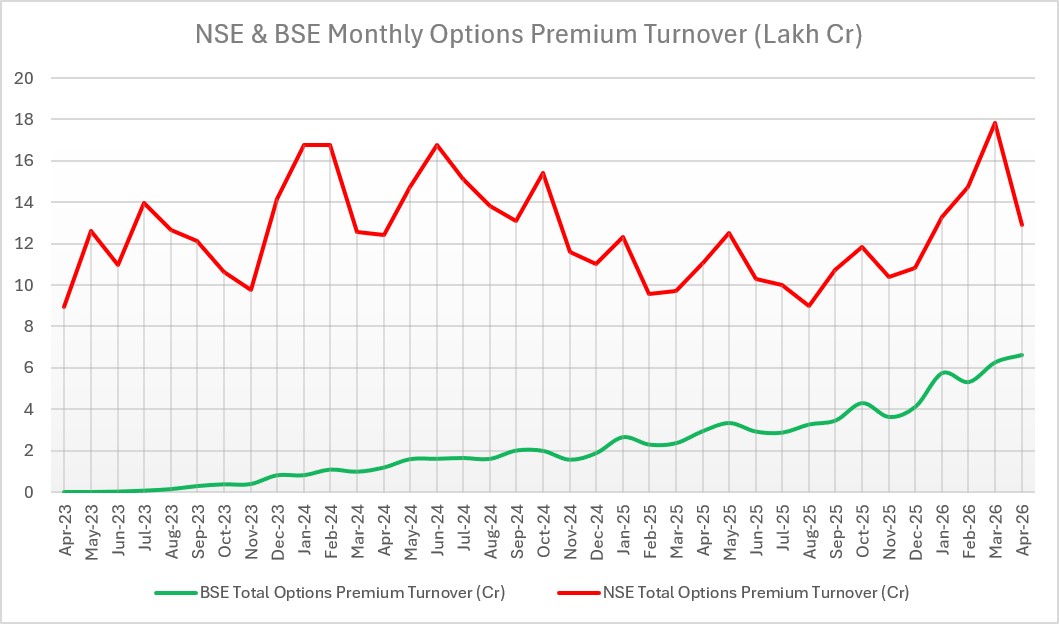

BSE market share seems to have crossed 30% to ~33%.

This share will go higher this month, since BSE has 2 expiries upcoming, and NSE just 1.

Is the drop in volume due to external factors like STT hike? Or reorientation by some traders for the new FY.

Again like previous writings, the options data needs to be seen over a 2-3 month time period to establish a proper trend. But Q1 seems to be signaling some shift away from NSE. Will BSE benefit is a different question?

And on Future Volumes - That spike in March end/April 1st week of daily volumes to ~1K Cr did not sustain and is now back to the 200-400 Cr levels. Also revenue wise this is not adding anything to top/bottom line.

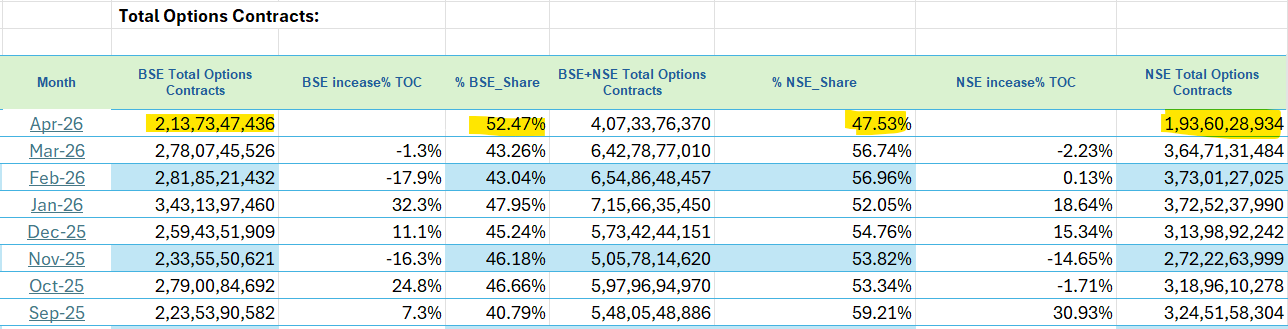

Edit: Seems the trend has held till end of the month. BSE PTO market share is ~34% (6.6L Cr), whereas NSE has dropped to ~66%, but major change is BSE Total Volumes share is ~55.3% up from 43.2% previous month. BSE had an additional expiry this month, this did impact. BSE revenue from FnO segment this month will be ~Rs.431Cr.

On futures contracts, NSE charges 0.00183% (₹1.83 per ₹1 lakh), while BSE levies no fee. In options, NSE charges 0.0355% (₹ 36 per ₹ 1 lakh )compared with BSE’s 0.005% (₹ 5 per ₹ 1 lakh) on stock options.

BSE has lot of scope for revenue increase. Can easily double without dent on volume.

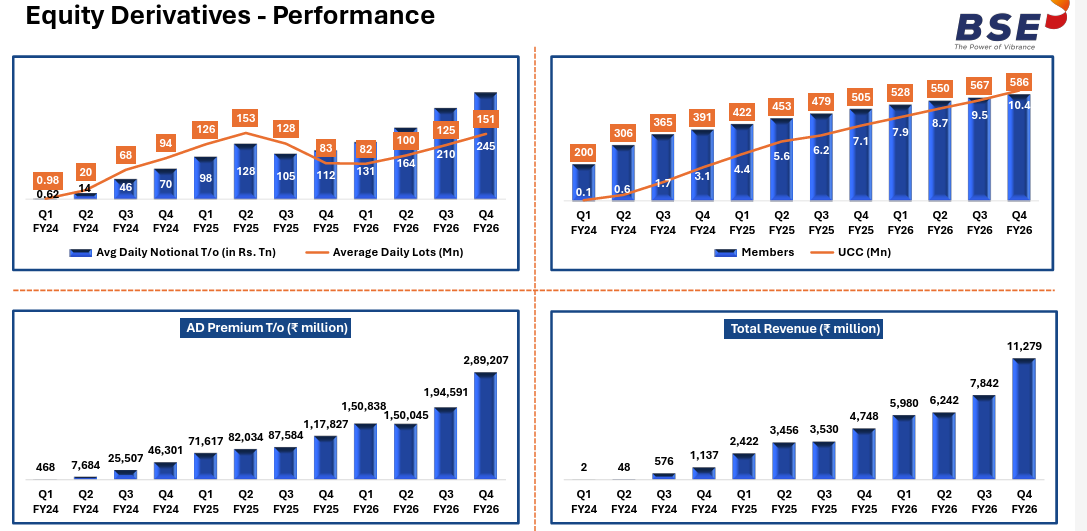

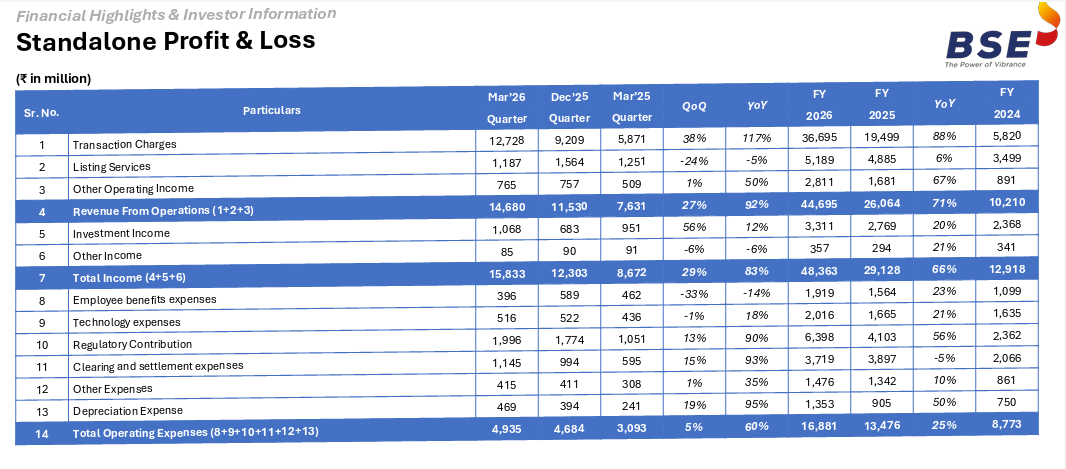

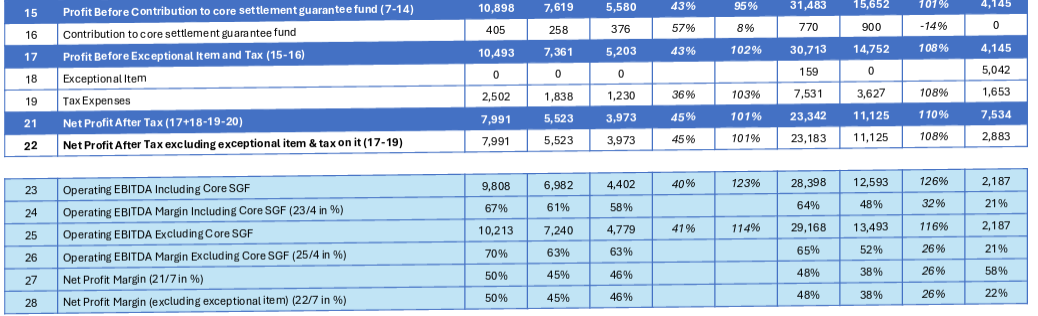

Numbers are very much in line with the expectations with standalone revenue at about 1500 Crore and profit after tax at about 800 Crore for the quarter.

The revenue from equity derivatives segment has exceeded 1100 Crore. See the details below:

Now that 2026 is behind us, we have a new benchmark of about 1500 Crore quarterly revenue and about 750 Crore quarterly profits. At the current market cap of 161K Cr, BSE trades at a normalized forward PE of about 53, which is very much reasonable for a business that is growing at this pace - I see further scope for valuation growth as the BSE has plenty of room to grow pricing in its derivatives business and hopefully penetrate into the stock derivatives and then into the currency and commodity segments.

I’m not sure why the dividends are only Rs. 10 per share as the business doesn’t need significant amount of money that they need to reinvest for growth - it would be a good question to ask management.

On the balance sheet side - the growth in fixed assets is understood to be on account of investment in its office building upkeep , co-location racks and technology upgrade - which are all in the right direction.

Looking forward to another good year with BSE and i would expect them to post a minimum of 6K Crore revenue and 3K Crore profits during 2027.