The stickiness of customers will not remain unless there is a futures product launched on this new exchange. Just for cash trades no one will go to mse. If there is an expiry here only then will customers be attracted to this, otherwise mse will not succeed. Until that happens, bse is the best bet.

3 Likes

Any thoughts on the possibility that NSE may prefer to list on Metropolitan Stock Exchange and not on BSE?

BSE is the obvious practical choice in most scenarios because it’s already a liquid with deep markets and wide institutional trust. MSE is still rebuilding and does not yet have the liquidity or market share to be a natural choice for listing

The article explains why India’s stock market has long been dominated by just two exchanges NSE and BSE and whether the Metropolitan Stock Exchange (MSE) can break that duopoly.

It highlights that exchanges make money from transaction fees, which only work if there’s deep liquidity and high volumes. NSE and BSE benefit from this network effect, making it very hard for any new exchange to attract traders.

MSE plans to tackle this by launching a Liquidity Enhancement Scheme (LES) where designated market makers will quote buy/sell prices in about 130 popular stocks, and transaction fees will be waived temporarily to attract early trading activity.

However, the article notes that once these incentives end, real liquidity must sustain itself, or traders will go back to NSE/BSE. Given NSE’s overwhelming market share and entrenched infrastructure, MSE still faces a tough road ahead.

Metropolitan Stock Exchange (MSE)

MSE is not exactly “new,” but it is undergoing a massive relaunch in late January 2026 after years of dormancy. It has raised over ₹1,240 crore from industry giants like Zerodha (Rainmatter), Groww, Peak XV Partners and Major PSU banks have stake in MSE, along with MCX.

MSE’s strategy is to launch 130 liquid stocks and a Liquidity Enhancement Scheme (LES).

By partnering with major discount brokers (who control ~40% of retail demat accounts), MSE has a direct “pipe” to retail traders.

NCDEX (National Commodity and Derivatives Exchange)

NCDEX, the king of agricultural commodities (97% market share), is diversifying into equities with a phased rollout starting in mid-2026.

NSE has highest stake in NCDEX with LIC, NABARD, IFFCO, PNB and Canara Bank.

NCDEX’s strategy is they are targeting Tier 4 and 6 cities, using their existing network of farmers and rural cooperatives.

Their plan is to start with a mutual fund platform first to build a cash base before launching equity trading.

2 Likes

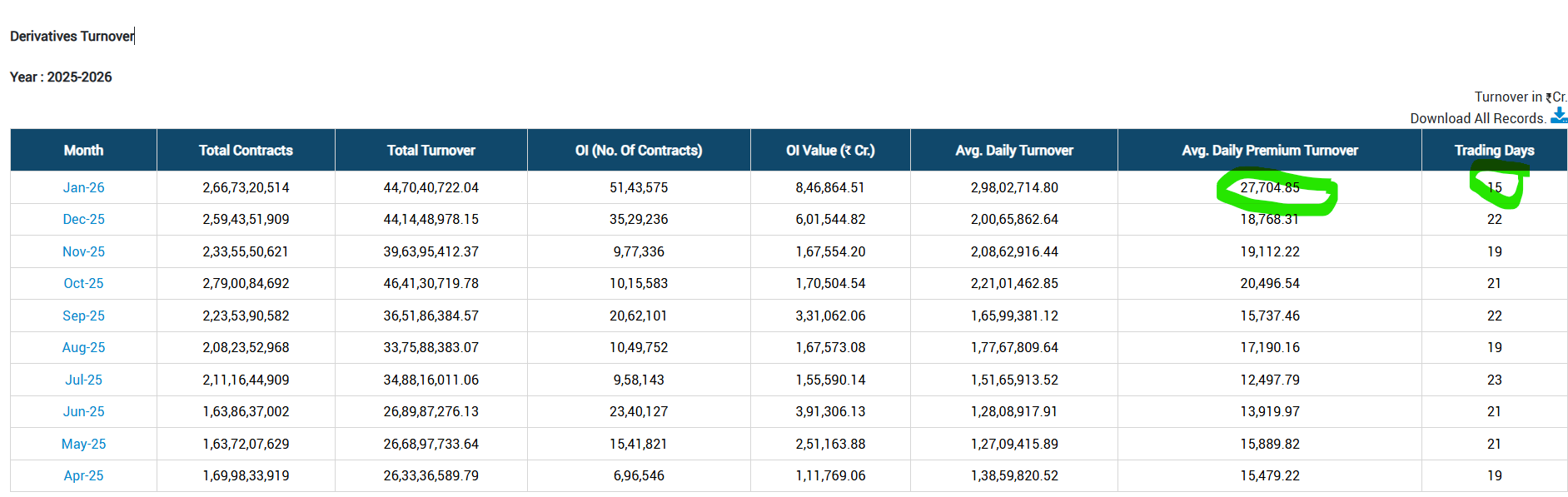

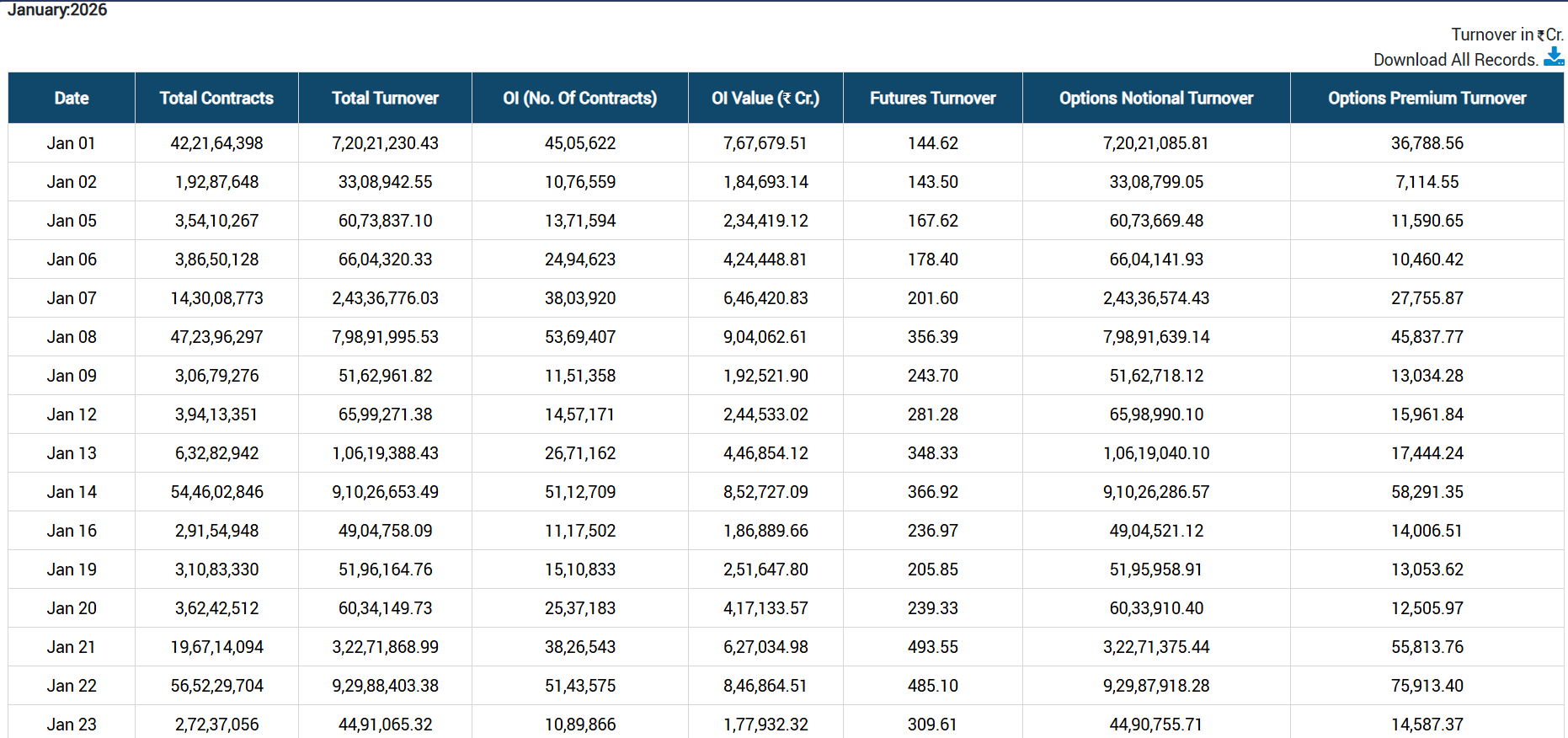

I am a bit confused with the data and I think fellow members can support.

January 26 is a bear market, and I was under impression that option turnover in bear market should go down, however, BSE option turnover data presents opposite picture. During first 15 days of trading, average daily option turnover is hovering around 27,000 Cr, its highest ever. What could explain it?

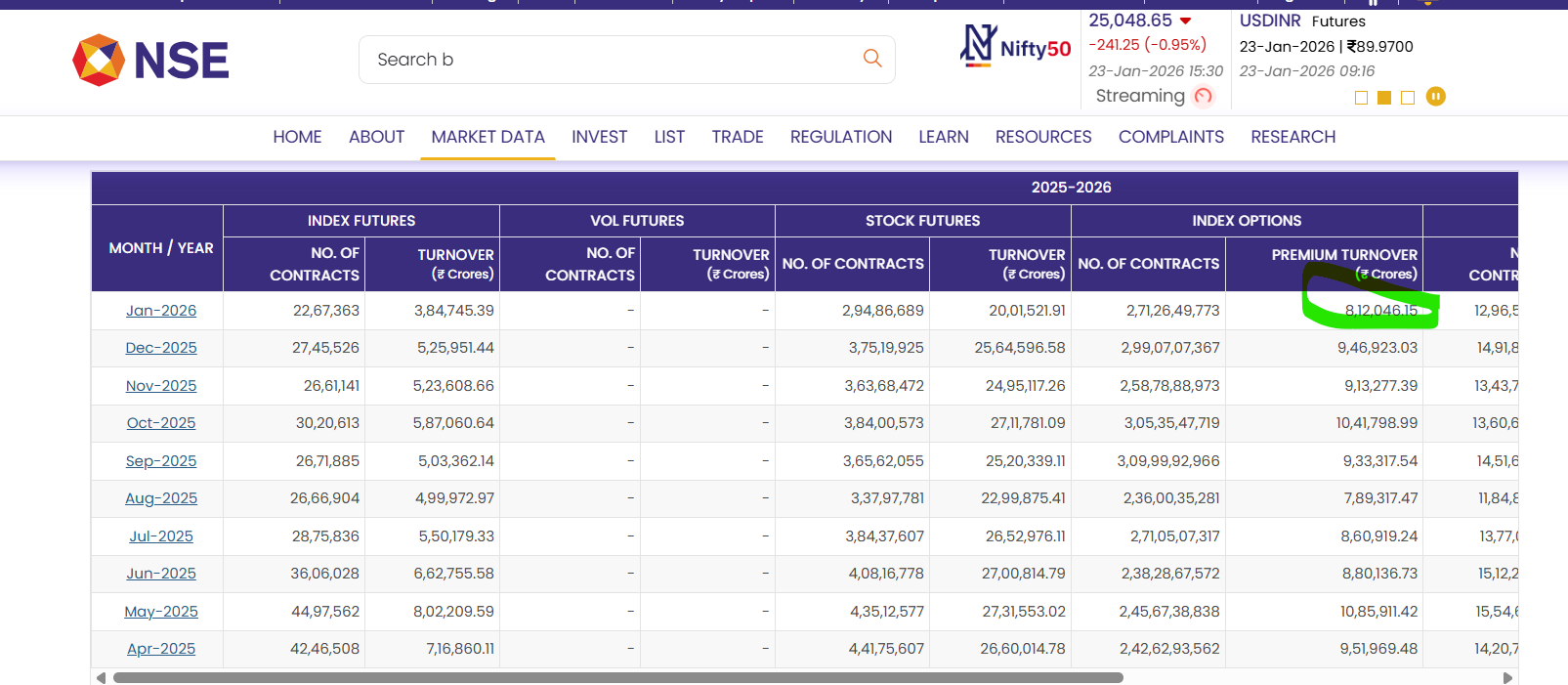

Where as NSE option Premium turnover data does not present same spike for Jan 26, so confusion continues

4 Likes

Higher the volatility higher will be the derivatives activity and premium. Other than that, BSE is steadily increasing the colocation racks available and as per management, the demand for these racks has been robust – it is natural for the derivatives turnover to go up in line with the addition of racks.

AJ

Disclaimer: Remian invested. Consider my views as biased.

8 Likes

Off lately, I can see BSE has launched many new sectoral/momentum indices like BSE 500 momentum 50 etc.

My query is - If any mutual fund launches BSE indices (like Sensex, BSE 500 momentum 50 etc.) either passive index fund or ETF, is it compulsion for them to buy corresponding shares at BSE exchange only? Like sensex has 30 companies. Same is available for trade in NSE also with higher liquidity. But if fund house is launching BSE indices product, do they have agreement to compulsorily buy/sell on BSE?

Why I am asking this is - If they do compulsion to trade only at BSE, it can provide some institutional liquidity at BSE cash segment which is not doing great. & As we know, in ETF & passive index fund also, NSE indices are currently dominating but I can see lately BSE is also trying to catch the missing train here with some good products. So if their indices ETF/MF gets some traction & if they have agreement to compulsion to trade at BSE only - Down the line after few years we can have improvement in liquidity in BSE cash segment.

There is no regulatory rule that forces ETF units to be traded only on one exchange just because the index itself is from BSE. it doesn’t restrict which exchange the fund manager must use to buy underlying stocks

1 Like

Any idea if BSE gets royalty from passive index funds?

Yes, BSE does get paid when a fund uses its index as the basis for a product like a Sensex ETF or an index fund. Although Indian mutual fund documents don’t publicly list exact fee payment terms,

But the standard global model for index licensing is that asset managers pay the index provider a recurring fee; typical licensing fees seen in other markets are roughly 0.015%–0.16% per year of assets under management tied to that index.

This can give an idea; they charge for giving simple data, so it’s obvious they will charge AMC as well so better if more Indices are launched and More AMC come out with Passive Funds on it.

5 Likes

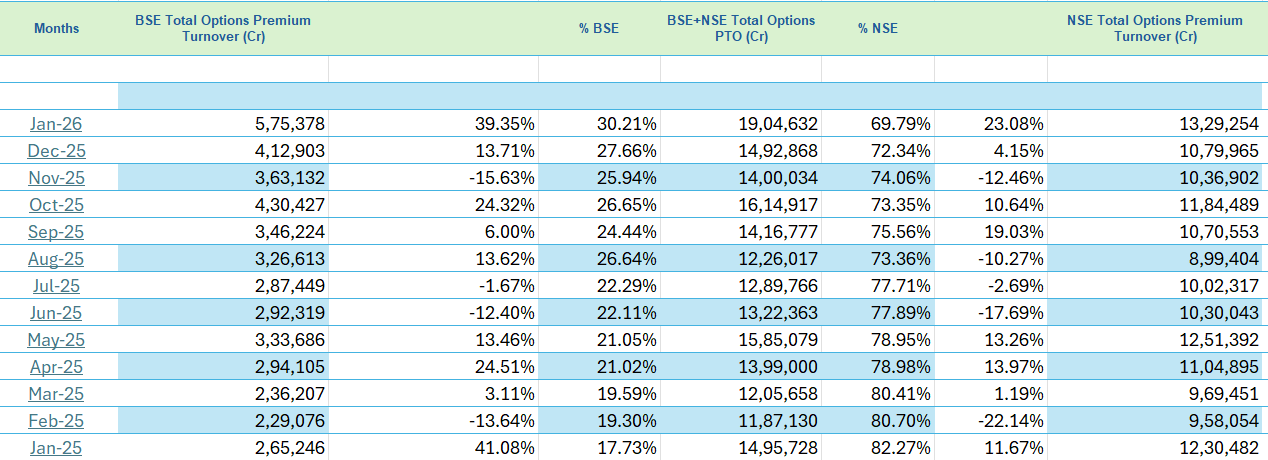

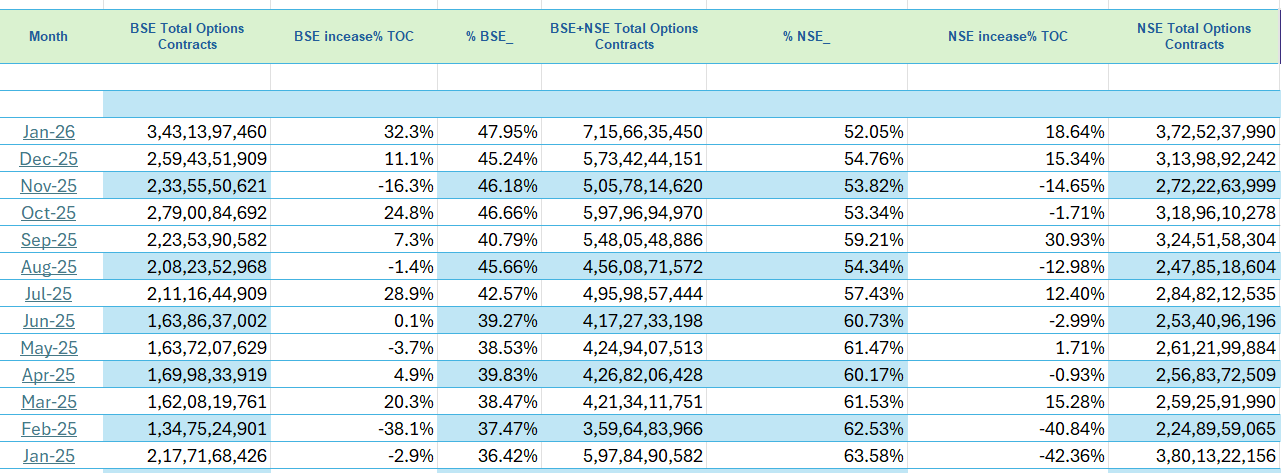

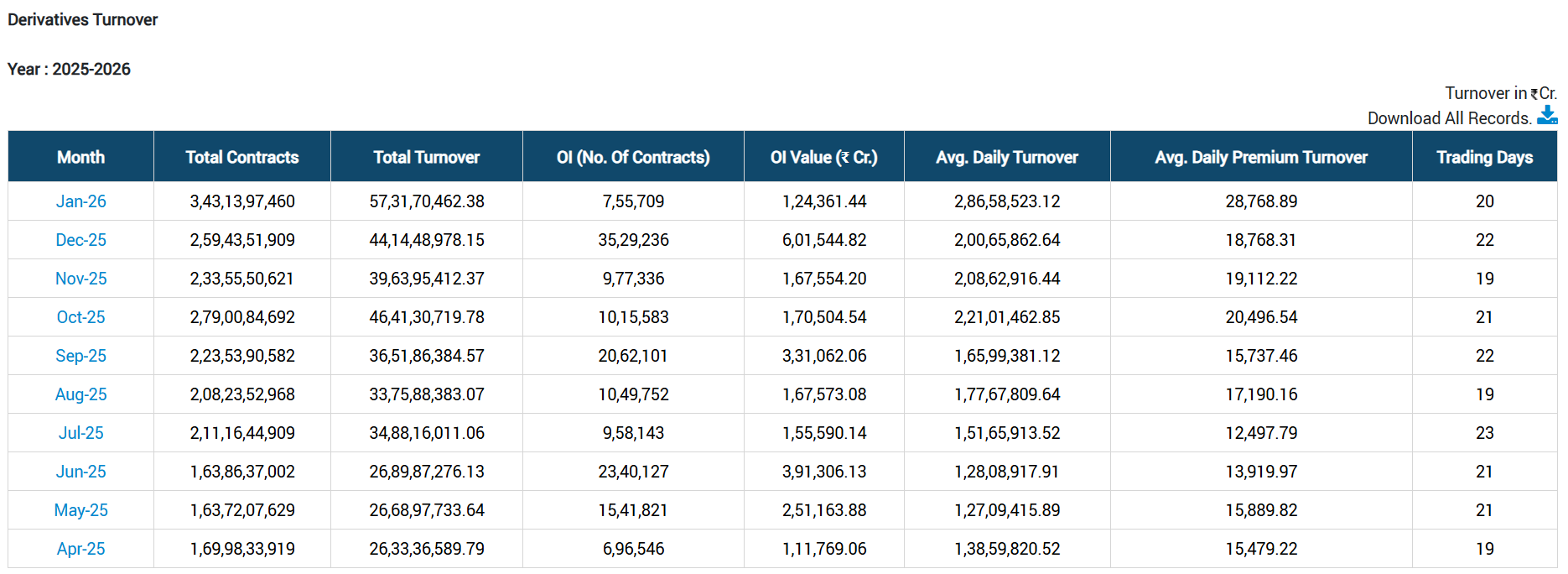

BSE Derivatives segment Jan 2026 update -

-

PTO data suggests BSE share has now climbed to 30%. But the last 6 months has been trending towards BSE maybe 1%/month average.

-

Contract Volume data also suggests BSE now having ~48% market share.

Based on the above data, total PTO for Jan was Rs. 5.75L Cr (30% of Options PTO market share), this will translate to Rs.~374Cr of revenue from Derivatives segment (assuming no change in pricing) only for Jan month. This if it continues over next 2 months, might bring in revenues of Rs1,000+Cr only in the Derivatives segment.

Jan 2026 saw a 32% increase in the total count of traded options contracts, but a 39% increase in PTO income, over Dec 2025. Avg Daily Premium increased almost 50% in Jan 2026 (Rs.28.7K Cr) versus Dec 2025 (Rs.18.7K Cr). The total PTO increase was lower since Jan had 2 less trading days.

Also last two expiry day PTO was Rs.68K and Rs.75KCr. Also the T-1 expiry day volumes are near to Rs.50K Cr. The increase in VIX in Jan + Budget might be contributing to this PTO increase. Need to see if this continues over the subsequent months.

10 Likes

Will NSE be listed on BSE exchange or NSE will list on another exchange?

Technically NSE can choose which exchange it can list on. Options are given on the SEBI website SEBI | Details of Stock Exchanges. Only BSE, NSE and MSEI have equity segment.

-

NSE cannot list on itself

-

MSEI has equity volumes of a few lakhs / day.

So only BSE is the option left.

5 Likes

Is this the end of the growth story?

Calling it the end is likely an overreaction, but the easy money phase for BSE is certainly over.

If retail volumes drop by 20–30% due to the cost increase, BSE’s transaction revenue (its biggest growth engine) will take a direct hit. High-frequency traders (HFTs) may also move their capital to more tax-efficient global markets.

But traders are a stubborn lot. Despite multiple tax hikes over the last decade, Indian derivative volumes have consistently hit record highs. Furthermore, BSE still has diversified revenue from its SME platform, mutual fund distribution (StAR MF), and listing fees, which aren’t affected by STT.

So it’s not the end, but it is a valuation reset. Now, it has to be priced as a mature exchange navigating a tougher regulatory and tax environment.

Sad and Angry with the budget, no doubt, but let’s see what future holds for the capital market sector with NSE IPO in line.

5 Likes

Most FNO traders are addicted to it. Increasing taxes have never deterred anybody from having one more drink.

I seriously doubt if the govt has seriously considered the effect of this -05% STT on its own pocket? According to reports 7 lakh crore of wealth was wiped out yesterday. Govt is a major share-holder in not only the PSUs, but in many non-govt companies, directly or indirectly. This year, it is estimated that it earned 55000 cr through STT. As per estimates, on NSE almost 50% of the trade is in the FNO. That will make it 27500 cr, if we assume the percentage for both NSE and the BSE is the same. A .50% raise will add 137.5 crore to the govt’s kitty.

Take the example of NSE. In NSE, PSUs hold 1.74 lakh cr worth of shares. NSE share down 2.5% today, roughly. This means the PSU wealth down by ₹43500000000! This is just one example. Govt has lost more than any @MadhuKela or@ICICIPruMF

My maths, estimates may be awry. Please feel free to correct it. But my meaning would be clear. Govt got it wrong in messaging.

2 Likes

Guys lets not overreact….yet to see impact on volumes starting April 1…..my guess is that futures are more badly hit than options….probably ppl trading in futures will go to options…..30 pct hit to volumes seems pretty high….I doubt the impact will be that much….jefferies estimates it close to 5 pct….will see what will happen post April 1.

2 Likes

Who, anyways, trades in BSE stock and index futures? Most of Vol is in NSE stock and index futures contracts. BSE options will have more impact than futures.

1 Like

Yeah….my point is that there is 50 pct increase in stt on options while there is 150 pct increase in stt on futures….so volumes if any in futures will also go to options because people can create synthetic futures there…..I doubt the options volume will be hit due to this…infact we might see more options trading.

2 Likes

Bse has now 58% of its revenue coming from derivatives . Past 2 years when the STT was increased the price of BSE had little or no impact, however now the share of derivatives is very high and thus can have a negative impact. Also we need to be aware of the fact that this increase in STT is the steepest in the past 2-3 years.

2 Likes

Yes, this STT fiasco will hit big players more than small. The idea of decrease in retail participation by FM is senseless.

3 Likes