@Thomala_Sainath : Fully Agree with you , I could see in his body language that he is up to give a good fight to NSE and end their monopoly , Recently he has also made a comments that Exchange monopolies guidelines should be made by SEBI similar to upi by npci

BSE should actually switch to Friday so that they get 4 days of expiry trading volume ,I believe they are waiting for NSE;s April contracts to be released and once that is released to market then NSE cant switch back, then BSE should make this move.

3 Likes

why BSE is falling so much? its well below crucial level of 200 day EMA also and that too on high volume…It seems, some institutional investor is selling?

1 Like

due to possible loss of market share after NSE changed their expiry date to Mondays

3 Likes

@rshankv : By when NSE is likely to release its April contracts ?

The existing weekly contracts are due to expire on 24th April so the Monday after 24th April is 28th April and the contracts for 28th April should start from 17th March (6 weeks before expiry) , so once the new contracts become active then BSE can change their expiry date.

This is just my hypothesis please don’t any investment Soley based on my theory .

2 Likes

Thanks @rshankv , Do you think if BSE change their expiry to Friday , it can work in their favour as the premium cost of NSE options will increase on Friday due to 2 days of weekend and good volumes might shift from nse to BSE

IF BSE changes their expiry to Friday they will get elephants share of weekly contracts ![]()

1 Like

BSE being listed entity they need to take consideration of their stockholders interest much more intently and SEBI doesn’t have a say in the expiry day change for an Exhange.

2 Likes

Will Not Run Behind Derivative Market Share However There Should Be A Spread Behind 2 Expiries: BSE - YouTube

These are the edited excerpts from the interview.

Q: The National Stock Exchange (NSE) has tinkered with the expiry day; they have shifted it to Monday. The question is, is BSE thinking of changing the expiry day? Have you had a look at it, and by when could we hear a response coming from the BSE regarding tinkering with the expiry day, or will you stay with status quo on Tuesday?

A: As you may recall, I worked with NSE for a significantly long time, since the inception of derivatives in various facets of market development, investor protection, investor awareness creation, surveillance, clearing, and settlement. Thursday has been a hallmark expiry day for a significantly long time. With the introduction of multiple products, expiry days were spread across all days, leaving only BSE to choose Friday at that point as an expiry day.

The past has shown us that clubbing expiry days on a single day does not help a product serve its utility for the market. For example, Sensex expiry coincided with Thursday’s expiry for a very long time, and despite multiple efforts, Sensex did not take off. And when we changed the product specification, the utility of the product was visible. When we made it very close to Thursday because we had no other choice, while its utility improved, it was not coming out in full. The concentration of trading activity on the expiry day was far higher.

Now, when we shifted it to Tuesday, interspersing the expiries with time, the concentration on expiry day activity has almost halved. This indicates the economic significance of a product can be well achieved, particularly if it is a highly correlated product by interspersing expiry days in between, but properly spreading the contract so that people can use it for the desired purpose of hedging against volatility over different periods—across the week, next week, and the month. That is our thought process.

Regarding BSE’s stand, we are considering market feedback from both people we have approached and those who have approached us. The point that stands out is that there should be a spread between expiry days. What that spread should be and how it should be structured are nuances that we need to analyze based on how the market evolves. Since many other realignments are already underway, making any rushed decision would not help with product development and economic development. So, for now, we are assimilating all the announcements and changes, and we will come out with a stand that will be useful for the product.

Q: This is a two-part question. What is the probability that you will change the expiry date? Is it high, based on the feedback you have received? Secondly, by when will you respond to this? If there is a change, it appears unlikely that it will happen in April. Please correct me if I am wrong. By when can we expect a response from BSE?

A: I would like to reiterate that BSE’s expiry was previously scheduled next to NSE’s expiry of Nifty and Bank Nifty for a significantly long time when it was relaunched. Notwithstanding the fact that Sensex was trying to find its footing, the only thing it was unable to achieve was proper economic significance for itself. So, in this revised scenario, when BSE Sensex is establishing itself as a strong product, any decision must be carefully considered. It cannot be dictated by a time horizon; instead, it should be aligned with broader market realignment.

Q: But there is a probability that you will change it?

A: No probability can ever be ruled out; however, ascribing a high or low percentage to it is very difficult at this point.

Q: The street believes that BSE’s rough market share is in the early 20s—around 22% or so. They believe that since NSE has tinkered with the expiry day, BSE could lose market share. Do you think that is the case?

A: I want to clarify something—as I have always said to the media and press, BSE in the derivatives segment will not chase market share because our market share is 100% since the product is unique.

Q: But investors want to know because your market share has gone up, and you have gained significant traction since you took charge—especially since you adjusted your expiry day as well. The street fears you may now lose market share. How do you respond?

A: What I would say is that BSE strives very hard to deepen and broaden the market. When you focus on this, what some might call market share is a byproduct—not the main goal.

What do we mean by deepening and broadening the market? We want more investors who qualify to trade in derivatives to actively participate. We want more FPIs with a long-term perspective on the Indian market. We want more brokers and a wider market reach—that is what we will work on. Any product change or development necessary to achieve this goal is what we will focus on. The resulting market share will follow naturally.

I would also reiterate that BSE’s expiry was aligned with two major contracts when it initially gained its foothold and started growing. So, it is difficult to predict how the market will respond in the future based on just one change. Does that mean we are ruling out any options? Certainly not. Does it create any anxiety or fear? No, because our goal remains clear: to deepen and broaden the market.

Q: Let’s talk about the SEBI consultation paper that has come out. The fear is that trading volumes will get curbed, and in turn, it could impact your turnover and the average traded quantity as well. Could you tell us what the key takeaways are that you have seen in this consultation paper and also any kind of recommendations, any thoughts on this SEBI consultation paper?

A: SEBI’s role has two important points. One is market development, and the second is investor protection. If you look at all the activities of SEBI with regard to derivatives; with regard to anything till now, and particularly derivatives, what we have been seeing since October has aimed to achieve this twin objective. The objective of no regulator is to curtail the market and make its liquidity dry up. At the same time, along with development, it should also focus on investor protection.

If you look at all the discussions that are happening, it’s all happening in that way.

The key takeaway for us is that this is the goal and this is the process. In the process, there will always be some outcomes from the expert working group. But SEBI does not feel that it is complete without consulting the public. That is why the consultation paper is published.

Multiple people have given a lot of feedback, which we are hearing, on how to ensure that there is an open position limit, particularly in terms of index derivatives, which are very heavily talked about. How to set an open position limit at a client level and at the same time aid market development is a key focus. The regulatory process in India is very healthy and collaborative. Regulators have never acted in a silo without consulting market views.

So, I am sure this time as well, while the expert group has come out with a consultation paper to seek and solicit views from the market, a large number of responses have been received by the regulators. All these factors will be considered, and at the appropriate time, the right decision for the market will be taken to ensure the twin objectives of market development and investor protection. That is our strong feeling.

Q: The market has softened a little in the last few months, and there has been a bit of a correction as well. There are also curbs that could probably be in the offing. What is the fall you’ve seen in total turnover from BSE? If you compare it with averages from the recent past, how much lower are volumes in the last month or so in comparison to earlier?

A: In terms of the cash market, well, the average yearly traded volume has increased for us. In terms of percentage market share, it has not grown significantly. It’s hovering around 6.5 to 7%. At one point, it touched up to 10% to 10.5%, but it is not increase further. There are a host of reasons for this. Some of the major reforms in the pipeline are yet to take off for various reasons. One such reform is the common contract note, which has been a huge demand from institutional players. For various reasons, it has been postponed from October to November, and now to April 30th. We hope that it will come out.

The second factor is that the next important participant in the cash market is retail investors. For them to participate, mobile apps are very important. Many times, today, what you find is that the mobile apps provided by brokers do not offer a level playing field. There have been quite a few SEBI interventions in this regard. We hope all of them will fructify and direct the regulators to the brokers, which will also help in this area. So that is the second thing that is a work in progress. If these two developments take place, people who are liquidity providers will come into the market. We feel there is significant potential for the complementary growth of BSE in the cash market, where the overall market expands and BSE’s share increases as well.

Q: As of now, you are saying BSE’s market share is around 6-7% in the cash market, and cash market volumes haven’t really picked up?

A: They have gone up slightly in terms of average daily traded volume.

Q: Something that we spoke about in the past as well—you mentioned that derivatives market volumes might decline, but there could be a shift towards cash market volume. We’ve briefly spoken about this in the past as well. In the derivatives market, what is the volume fall, and if you could tell us your updated market share over there?

A: Overall, national turnover across the exchanges has come down by around 40%, and the premium has declined by 17%. While I would continue to reiterate my earlier stand that we do not chase market share, our market share remains 100%. Regarding the figures you asked for, notional volumes at BSE have fallen by around 17%, etc. Premium volumes, however, have stabilized as far as Sensex is concerned, there has not been any significant fall, but I would call that part of a catch-up process and realignment. Bankex is not seeing much volume yet because it will take time to develop as a monthly product instead of a weekly one.

Q: There is a clearing cooperation dispute between the exchanges, and reports suggest there has been a push from SEBI to resolve the issue. Are there any such talks about that with regard to these reports? Also, since we are talking about NSE, there is the settlement guarantee fund (SGF). As your volumes grow, do you believe BSE will also need to contribute more to the SGF?

A: As of today, BSE has no outstanding dues towards any clearing corporation whatsoever.

Q: But now volumes are going up. So, will you need to contribute in time?

A: Are you referring to SGF? Yes, I was replying to the earlier question. Alright, so as of now, BSE does not owe any dues to any clearing corporation. Yes, what I understand is that NSE has some dues to be paid to Indian Clearing Corporation Limited (ICCL). Indeed, the matter has been raised with the regulators by both parties. I am sure that as mature exchanges and clearing corporations, a resolution will be found.

Regarding SGF, the challenge is in predicting SGF requirements due to the complexities of the algorithm. If the algorithm is not conducive, it becomes difficult to forecast the contribution requirement. However, if there is historical data available, contributions can be planned proactively and accounted for in the P&L. It is a work in progress, but it is not easy.

Q: Another work in progress is the NSE IPO. Will it be competition, or how do you view that? You have been part of NSE in the past as well, and this has been a big topic of discussion.

A: I am no longer part of NSE. This is a question best answered by NSE.

For the entire interview, watch the accompanying video

(Edited by : Sriram)

3 Likes

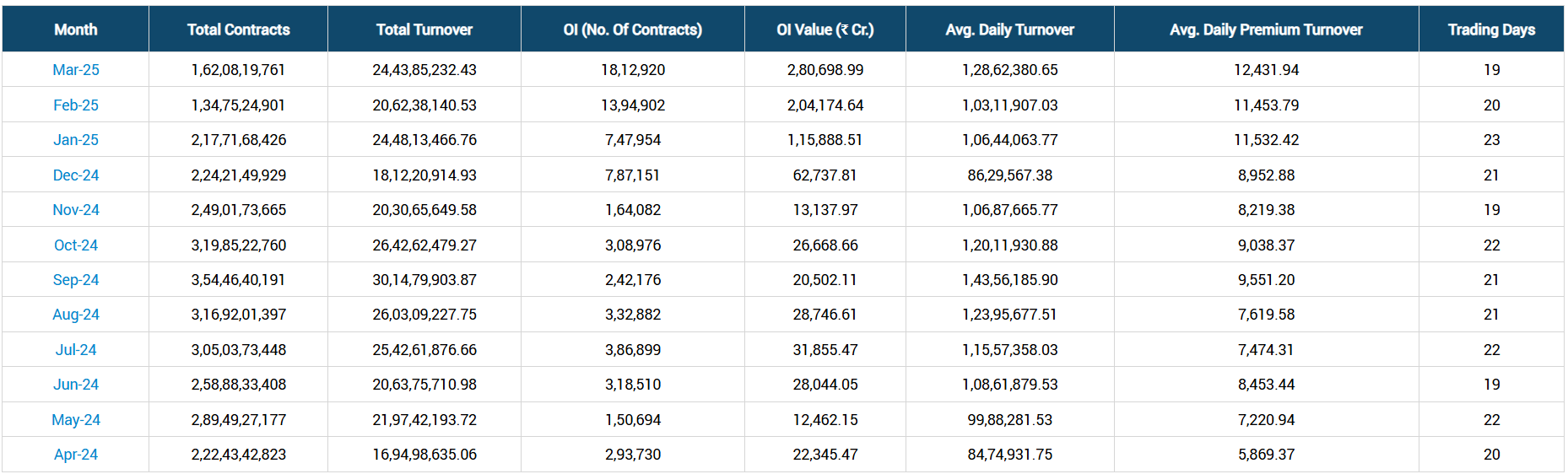

Even after the NSE move announcement, BSE volumes are holding up and steadily rising above 12,000Crs. Infact march 25th expiry day volumes was a massive 34,000Cr. Need to watch the BSE move on a possible change in Expiry day or they are confident to match with NSE.

FY25Q4 daily average volumes are ~35% higher (still 3 more days to go), might settle around ~30% since the 3 days are non-expiry. Will this translate into ~30% revenue growth & a higher addition to the bottomline in Q4 results?

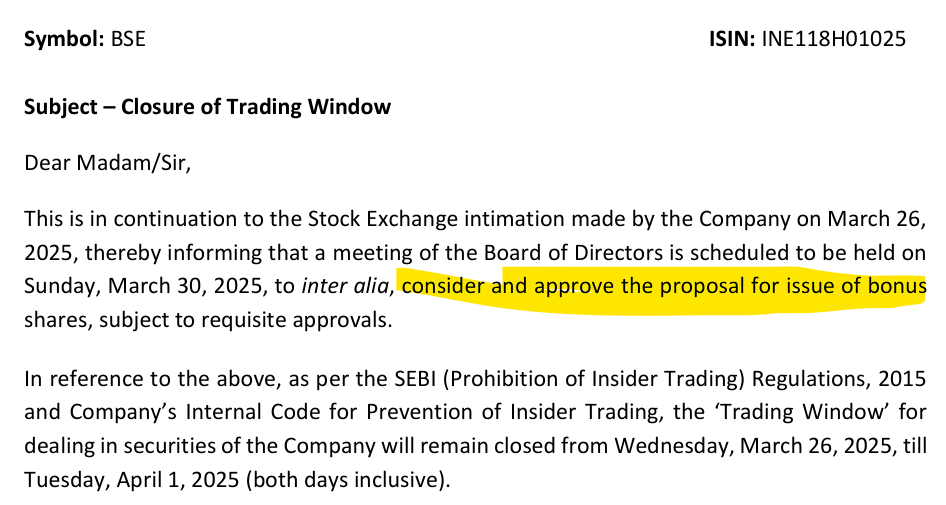

March 30th Board meeting for 150th Anniversary Year Bonus declaration ![]()

BSE_26032025162427_NSEIntimationTrade_WindowClosureIntimation.pdf

5 Likes

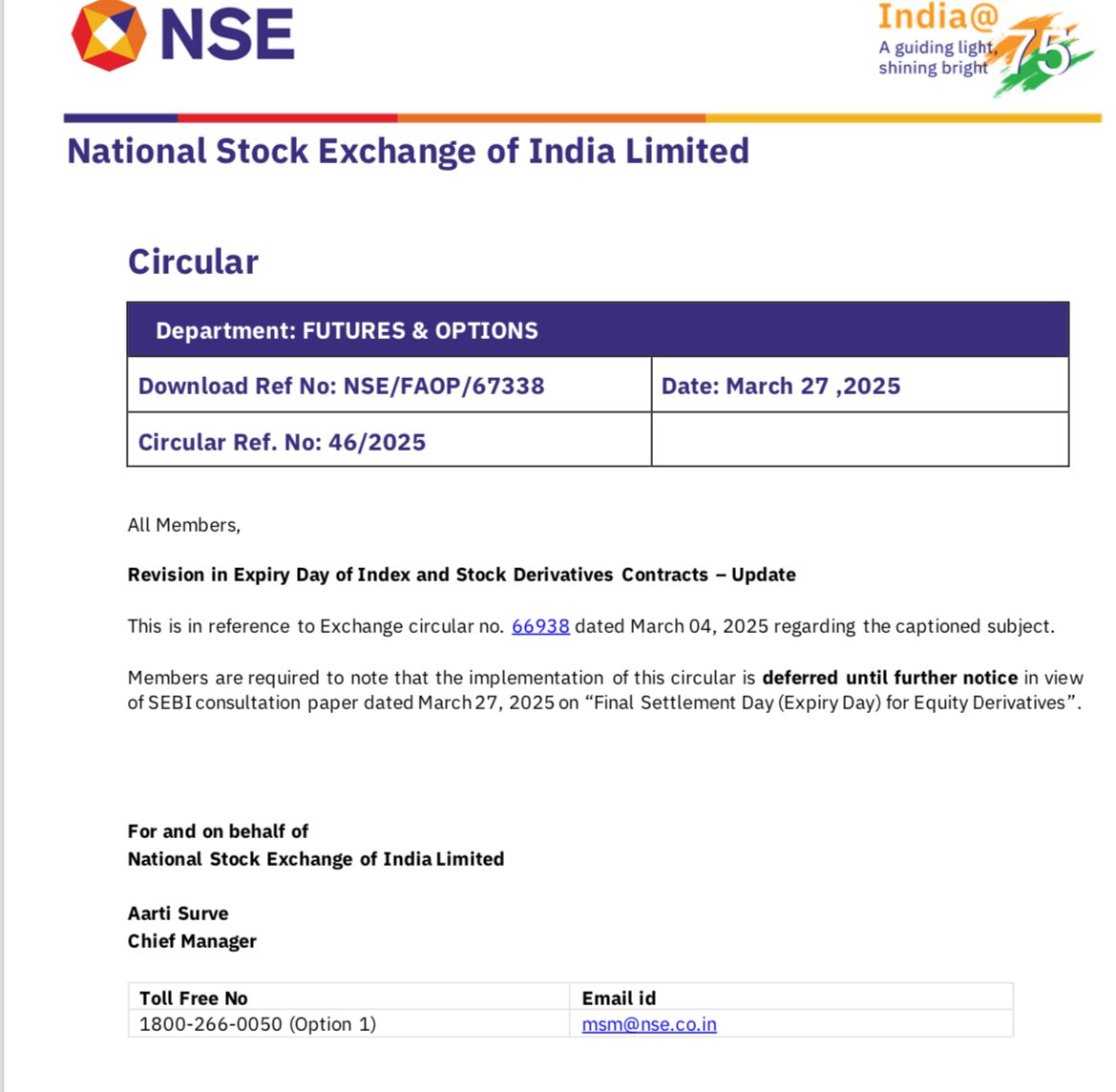

SEBI has proposed only 2 days of expiry : Tuesday and Thursday ; It’s a hit on the knuckles of NSE , very likely that NSE decision on moving expiry to Monday might be rolled back

4 Likes

Actually they have released a consultation paper on this. Mostly NSE will need to defer their Mon Expiry notification till this paper is formalized (needs to be confirmed) as per point 4.4.

They are asking for comments at this link - SEBI | Public Comments. Please submit your comments by April 17, 2025. Please share your comments with SEBI ![]()

1 Like

Bonus ratio declared.

2:1 i.e. 2 bonus shares for 1 share held.

https://nsearchives.nseindia.com/corporate/BSE1_30032025171031_Nseintimation.pdf

4 Likes

Q4 Update:

Derivatives: The average daily turnover was approximately 11,800 Crore during the quarter which roughly translates to about 30% growth as compared to the previous quarter – revenue from the segment is expected to grow by 20-25% taking into account the reduction in pricing during previous quarter.

Star Mutual Fund: To my surprise irrespective of the market volatility, the subscription order number remain same as Q3 and redemption reduced as compated to previous quarter - the revenue from the segment may show a slight downtick as compared to last quarter due to fall in redemption orders.

Equity segment: The numbers from equity segment continue to be disappointing - while the management can blame overall market sentiment for the poor performance, 20% fall from last quarter is significant.

The revenue from the segment should be lower by about 20% or more as compared to last quarter mirroring the fall in volume.

IPO Market: IPO market remained obscure during the months of Feb and March with just 6 and 4 new listings largely reflecting the market sentiments - overall the total number of listings for the quarter was about 27 with January contributing to 17 listings. Compared to last quarters 36 listings this is a fall of about 25%. The revenue from the segment should also fall by a similar %.

Overall, the revenue numbers are expected to be about 5 to 10% higher than what was reported during Q3 considering robust growth in derivatives numbers compensating for a poor performance in equity and IPO.

Disclosure: Remain invested - no recent transactions.

10 Likes

BSE has achieved premium turnover over >50K Crore for the first time today. Todays’ statistics as per the report available on BSE’s website is as below:

Volatile market is perfect breeding ground for higher premium turnover and poor retail to donate their valuable savings to the hands of the smarter ones.

Yesterdays’ premium TO of 31K is possibly another record for a non-expiry day.

Interesting time for stock exchanges!

Thank you!

AJ

Disclaimer: I’m a long-term investor in BSE and consider my views as biased.

11 Likes

BSE shareholders need to track the below topic of demerger of clearing corporations from stock exchanges. This will have a huge impact. Also the optionality of receiving shares in a clearing corporation (if that is given as part of demerger, but SEBI is reluctant to list clearing corporations).

SEBI’s proposal for demerger of clearing corporations, One point in the article:

SEBI should first look into the transaction charges part. This needs to be unbundled. This will help SEBI to understand how much money is going to exchanges and how much clearing corporations are paid out of that.

This possible move to unbundle transaction charges between exchange & clearing corp, might benefit BSE, if the NSE clearing corp charges are a big expense for BSE.

3 Likes

April 2025 was a very volatile (see the India VIX chart below), compared to March & Feb. We see this reflect in the Premium T/O numbers, as it touches average 16K/day. It is a good >30% higher, but is it sustainable and will it continue to grow at same pace?

5 Likes

1 Like