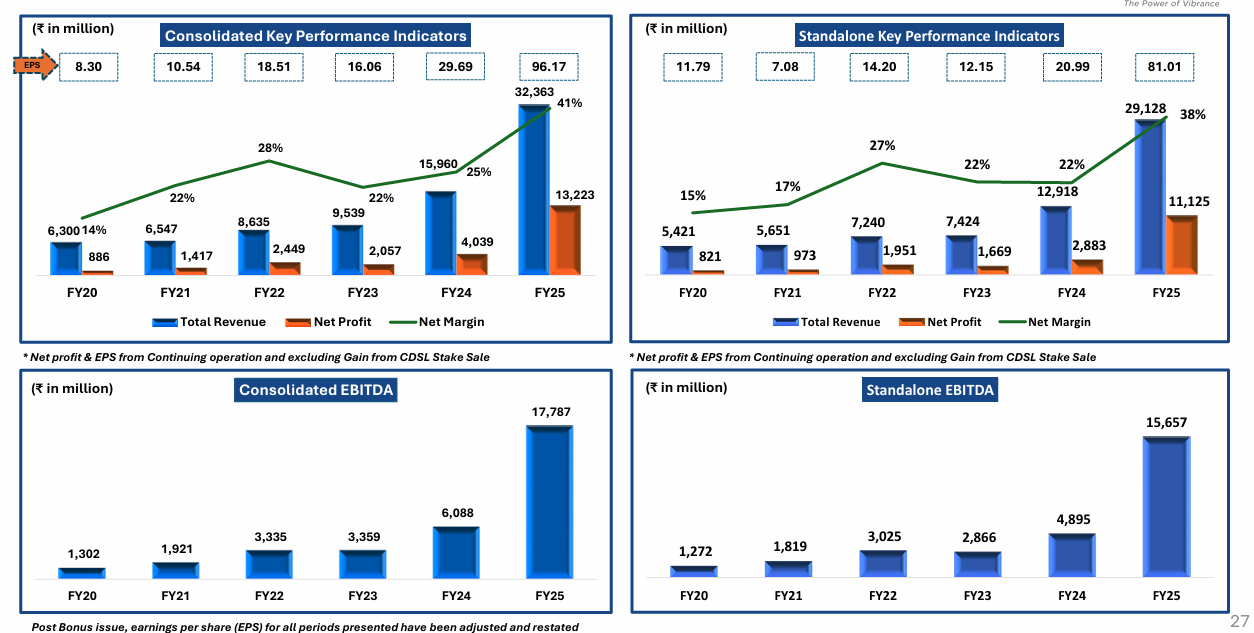

Q4 Income was 846Cr vs 483 Cr YoY, NP was 493 Cr vs 106 Cr YoY

FY25 Income was 2957Cr vs 1371Cr YoY, NP was 1322Cr vs 771Cr YoY

Good results. Investor Presentation Link & Board Meeting, Dividend, AGM, Record Date, etc Link

- Some of the Q3 SGF was reversed due to adjustments.

- Quarterly NP is touching ~400Cr, or yearly ~1500Cr or EPS of ~100Rs. PE ratio of 63 (@6300/share) seems stretched now.

- AGM is on Aug 20th

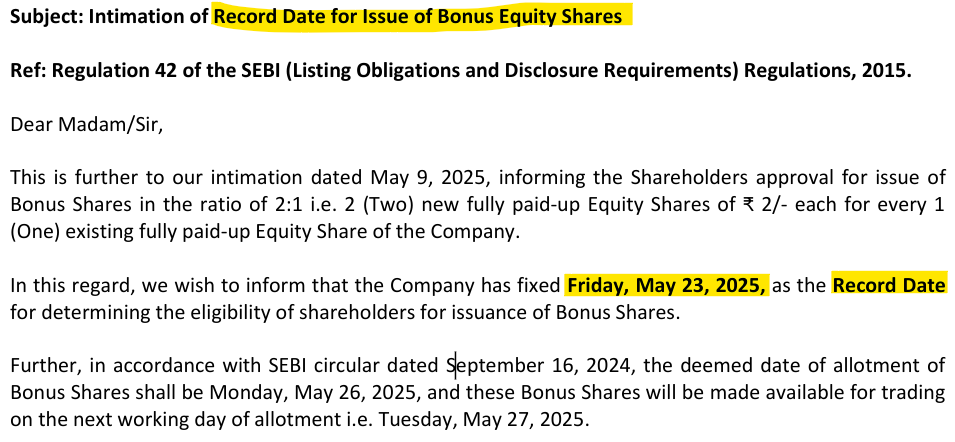

- Dividend is ONLY Rs.18 + Rs. 5 (special dividend), total of Rs.23/share, the Record Date is May 14, payable after AGM by Sept 18th 2025. Since Record date is next week, BSE Bonus shares will not get dividend (smart move by mgmt

)

) - Consolidated EBITDA has grown hugely, 1778 Cr vs 608 Cr YoY.

- Lot of Cash generation have grown quite well in BS, but dividend seems to be disappointing, esp in 150th year. Are they hoarding it for any capex needs? [Edit - Why the percentage of dividends payout is lower, CEO explained that they have spent 500cr on technology related to clearing, etc and that has already given the return to that fold. Balance between 1) Customers want confidence in the exchange and its clearing facilities, 2) A strong sound balance sheet.]

- Common Contract Note - This the CEO has been stressing is needed, but I am not sure if this will benefit BSE or not.

Disclaimer: Invested. No recent transactions. Was planning to lighten earlier, might continue with that thought.

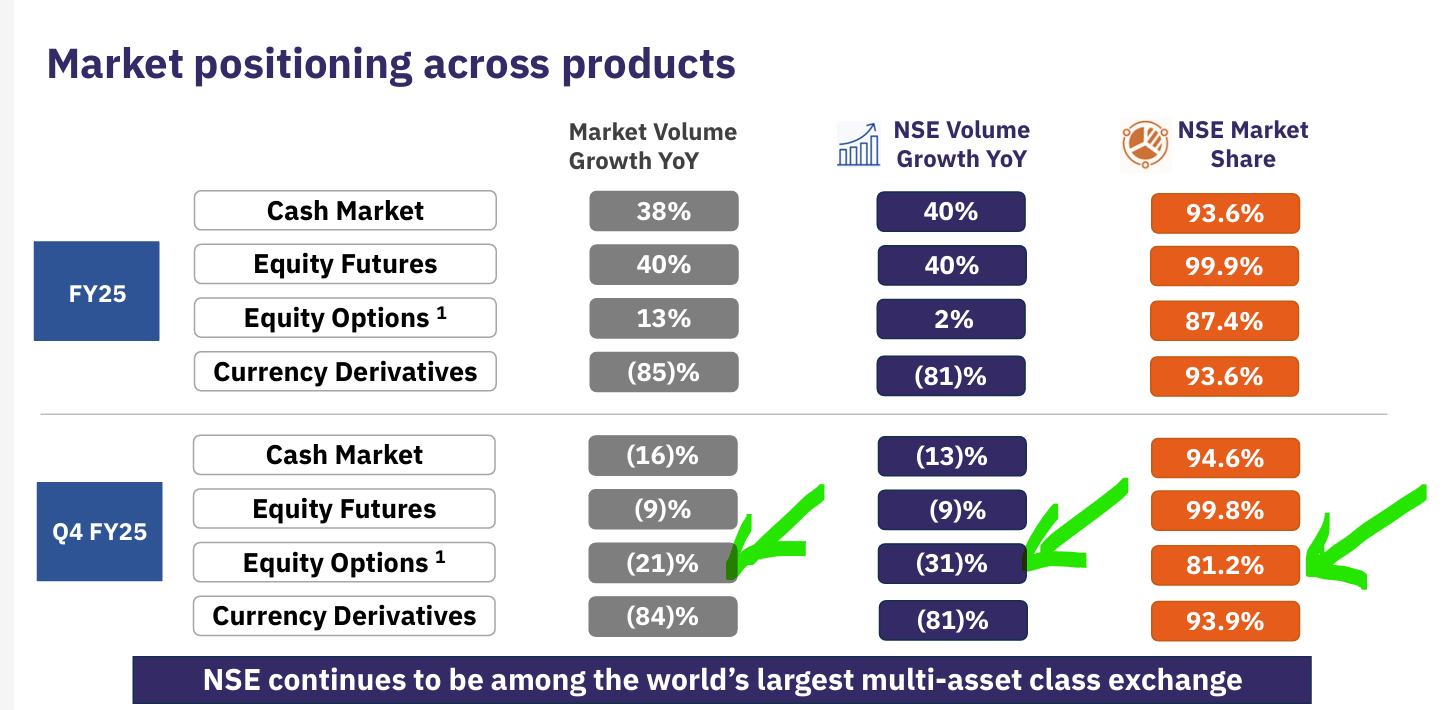

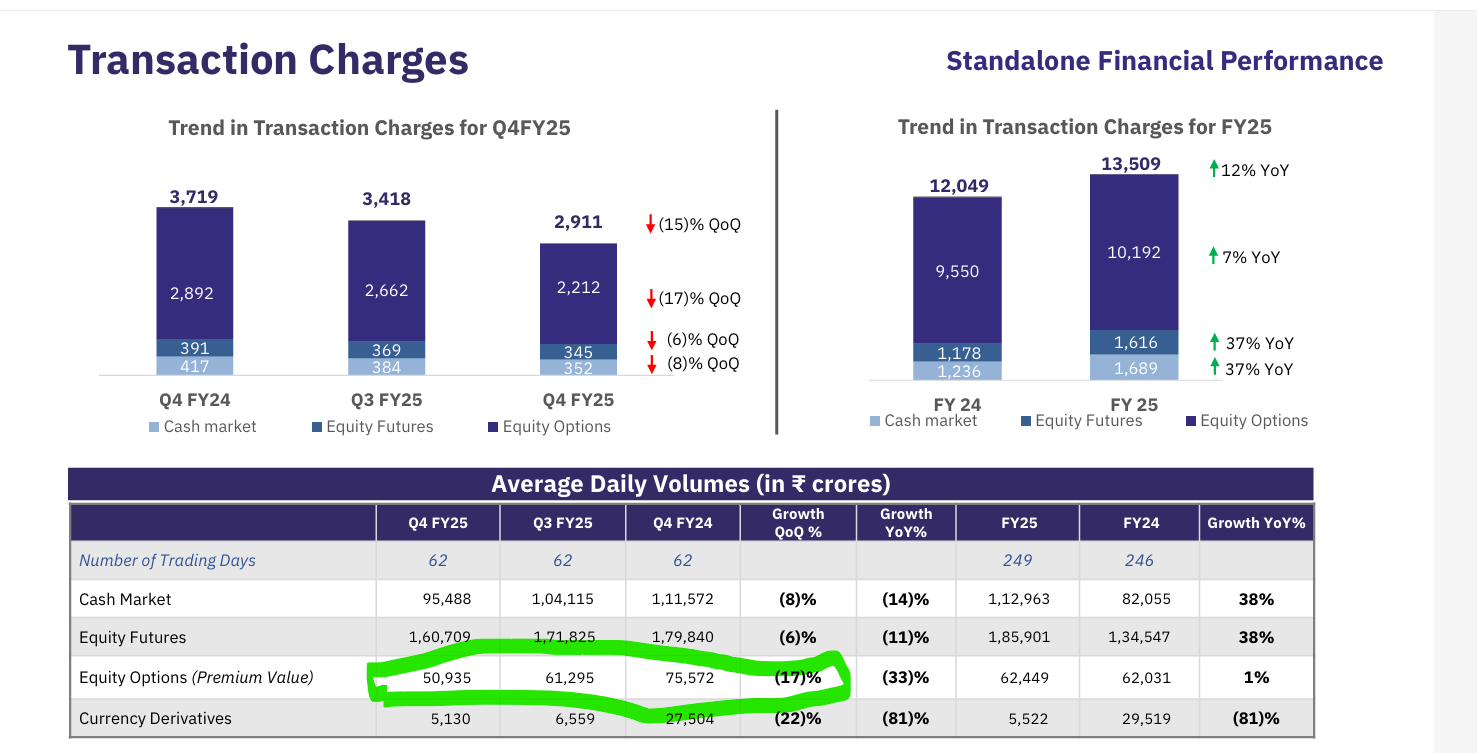

Coincidentally NSE also declared their results today - STANDALONE_CONSOLIDATED_RESULT_MAR25 & NSE Q4 Results

- final dividend of Rs. 35 per equity share

- Only 12,187Cr FY25 Profit, BSE is just 10% of this…long way to go.