NSE Clearing informed Sebi in a letter dated January 9 that there was deficit of Rs 176.65 crore in its minimum liquid assets it was primarily due to the non-receipt of Rs 312.37 crore in dues from BSE.

NSE management has said this is money that BSE owes to NSE for clearing & this amount has been outstanding for nearly a year now.

Do we know why BSE has not paid this amount? I believe there would be a P&L impact in the quarter when they eventually pay this…

Does anyone know if this is disputed amount? If BSE management had anything to share on this part? Would like to get clarifications, since amount is worth 1Q profits.

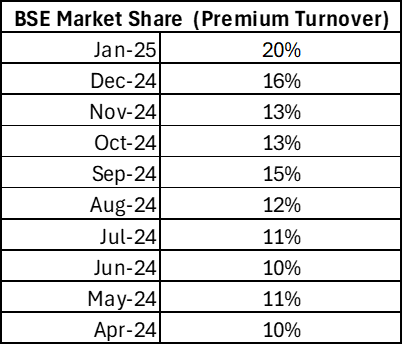

In terms of Premium Turnover - so far in Q4 its been decent ride for BSE with market share in the premium turnover moving from 16% in December to 20% in Jan25 and hovering in the region of 24% in February.

And the Feb Data on Premium Turnover is encouraging to say the list. Moving weekly index expiries to Tuesday definitely has been a great move.

Key Takeaways from NUVAMA Institutional Equities on BSE at recently held 20th Indias Investor Confidence.

Derivatives segment: We expect BSE to continue to deliver robust revenue

growth primarily driven by strong growth in ADPTV. BSE’s retail derivatives

investor base of 1.5–2mn remains significantly lower than NSE’s 4.2mn, indicating

potential for further increasing volumes. We expect the company to increase its

market share to 20.8% in FY26E (+689bp YoY) and 22.2% in FY27E (+137bp YoY).

Bankex volume and premium quality: BSE plans to improve Bankex volumes by

focusing on rebuilding liquidity by encouraging investors to consider strategies

more suited to monthly cycles. Participation on non-expiry days has increased,

which helps stabilise premium volumes.

SGF: The new computation includes three stress test models: factor model,

stressed VaR, and filtered historical simulation. Due to the new methodology, the

core required SGF fund increased to INR5.5bn and thus an additional INR4.81bn

was needed. BSE contributed INR530mn while ICCL contributed INR1.47bn, taking

the consolidated contribution to ~INR2bn. SEBI also allowed for a one-time

transfer from the cash segment to the derivatives segment and thus no additional

amount is now required. This was a one-time increase due to the change in

methodology. Management emphasised SGF cannot be linearly extrapolated due

to multiple influencing factors (price volatility, open interest, new

member additions).

Liquidity: The company is in talk with many brokers to give an option to the

investor for choosing the exchange they want to trade in. This along with common

contract note and combined market depth will provide better prices and attract

flows from institutional investor too.

Cash market share: BSE cash market share slid 150bp YoY/90bp QoQ to 6.1% this

quarter. Management expects introduction of common contract note to enhance

accessibility and aid in improving market share in the cash market.

Colocation: BSE increased its colocation racks to 200–220, but may need to add

additional racks as it still faces high demand. BSE currently charges only rack rent,

and has not yet introduced order-flow based charge. We believe this will be an

additional income stream as and when introduced. They aim to double the

capacity in FY26 via INR200–300mn capex.

Feb Index option premium market share trending at 24 pc , this is further increase from 20 pc in Jan .

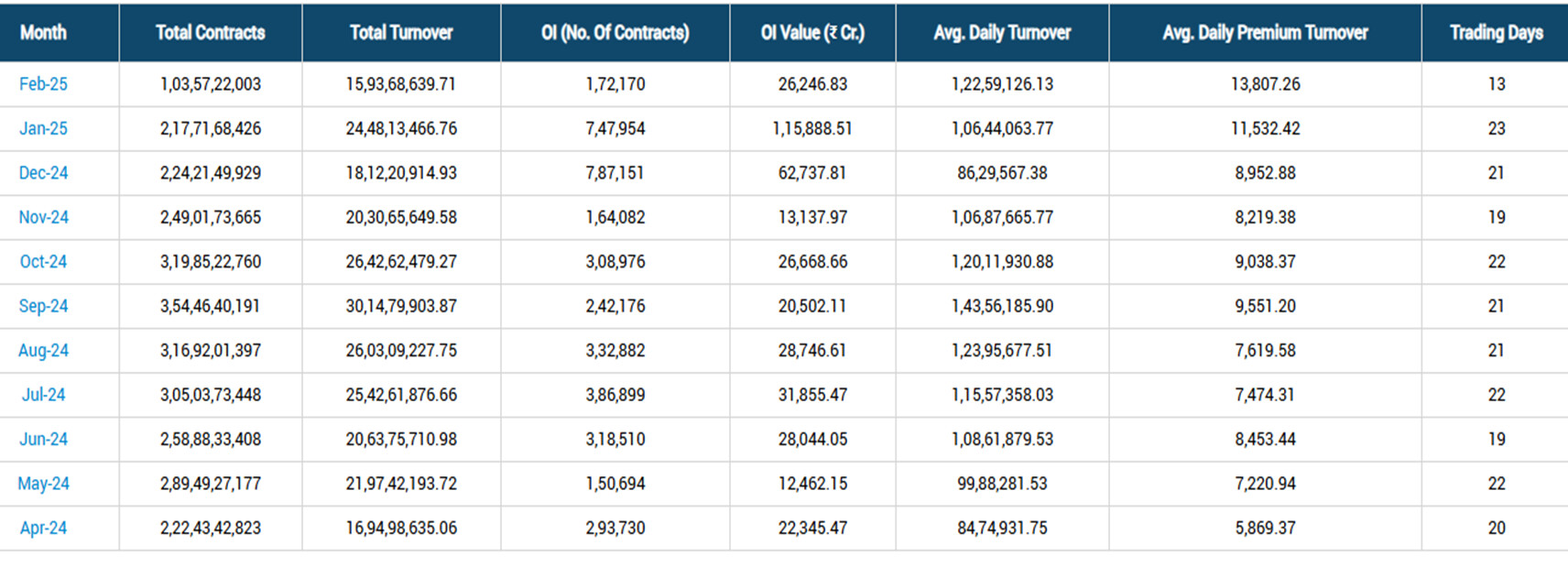

As per my limited understanding , SGF contribution mainly depends upon maximum open interest position and if max open interest position in Q4 is lower vs q3 , there may not be significant SGF contribution provision in Q4 .

Thanks all for contributing generously to this thread, especially to contributors after Oct 24.

Since middle of last year, I had been seeing BSE share price performing exceptionally well, despite being overpriced in my limited understanding, and I had formed my foolish view that its running with the bull market

Things have pretty much crystallized now, with few facts below:

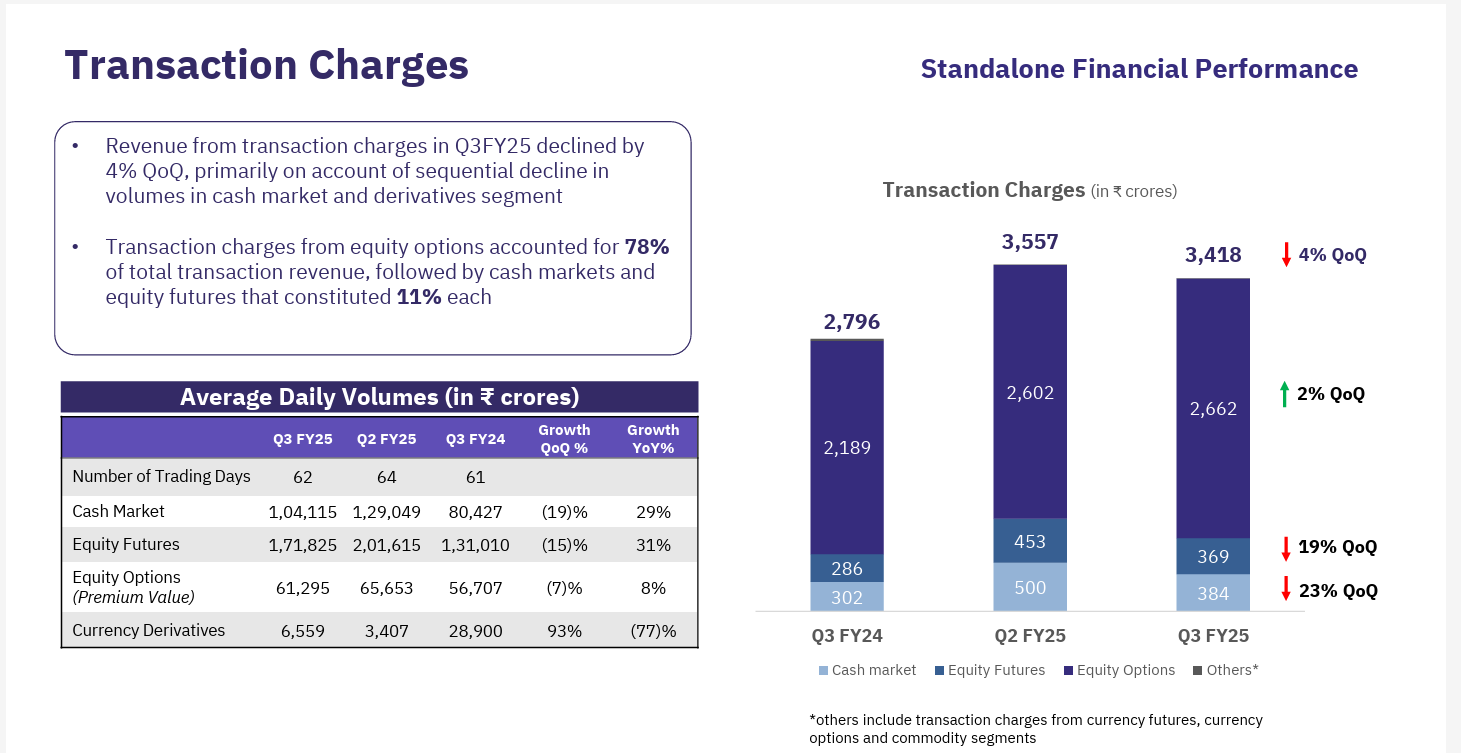

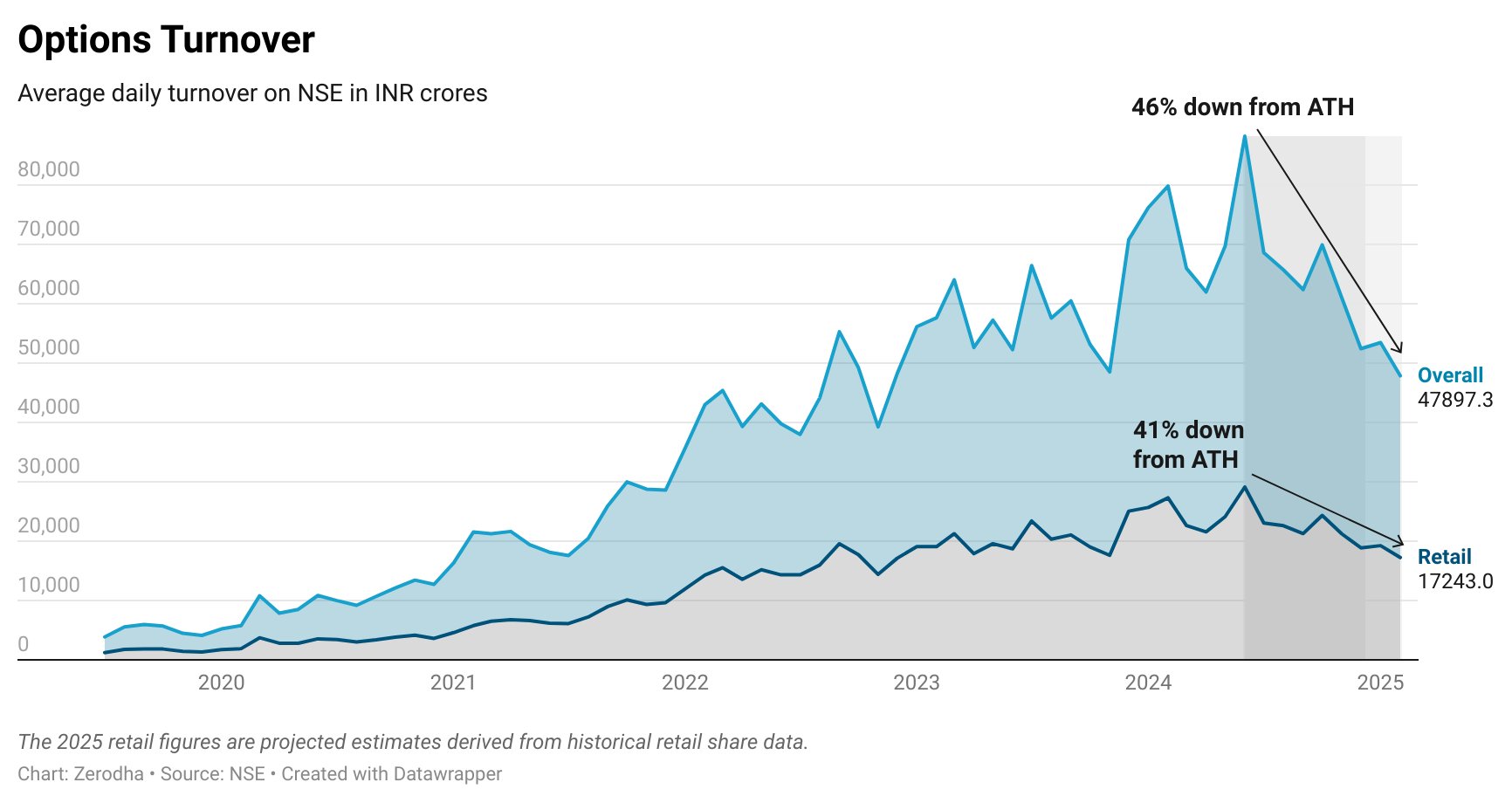

Market Leader (NSE) makes most of its profits from trading in equity option (primarily index options), roughly Rs 10,000 Cr per year (see chart below).

NSE had roughly 99% market share in equity options till Dec 23 (timeline may be off few months here and there), since when things started changing.

BSE that was sleeping since many many years suddenly woke up, and now commands 15 to 20% market share in equity options. This may be due to dumb luck, management execution or favorable regulation, but the fact of the matter is that it is giving serious competition to NSE today.

From 150 Cr profitability in FY23, today it stands to deliver 1500 Cr profitability in FY25 (including contribution of one off 200 Cr in SGF), a jump of 10X. No doubt why that market has rewarded BSE investors accordingly.

Will this trend continue or how will it pan out in future, is yet to be seen. But at current price, I see risk reward against the the buyer (my view, you may differ)

Hi Amit , You need to look ahead and not look

At valuations basis current profit ; I would add some additional facts

1 ) BSE ‘s Index option premium market share is already touching 24 pc in Feb and its increasing by almost 2-3 pc every month , this has gained momentum especially after change in weekly derivatives rules

2 ) Mutual fund business stellar run continues in Feb , growing at ~ 8-9 pc every month ; it has almost 100 pc market share

3 ) In my view Q4 PAT may be ~ 450 cr ( if there is no significant contribution to SGF ) and next year can be ~ 2200 cr PAT

4 ) For a company that’s growing its PAT and top line at more than 100 pc , forward PE of 35-40 is not too much

5 ) In my view , if BSE continues to increase it’s option premium market share to around 40 pc , increase in cash segment market share , expand its co location business and gift city business , I see BSE market cap to touch atleast 2 lacs crore market cap in next 3 year

5 ) NSE market cap has already touched 5 lacs crore in unlisted market .

@bibhor The numbers you are projecting are something, I definitely look forward to those getting achieved by BSE, have been a long term shareholder.

BSE got great tailwinds (direct and indirect) from,

Exit of previous CEO, previous CEO joining NSE,

Current CEO joining BSE from NSE,

Strategic initiatives from the current CEO,

SEBI restructuring the entire FNO market

SEBI started restructuring the clearing house process/shareholding

Previous system issues at NSE, showing fragility of system for overdependence on one exchange

NSE IPO valuation speculation + NSE profits from various segments (replicating these in BSE)

Options Premium T/O volumes

The challenge is, many (not all) of these direct tailwinds are done, and BSE now has to show the performance by its own efforts (e.g. BANKEX Options monthly strategies, etc) to increase volume and revenue share.

The expectations is fairly priced in, and anything higher might be difficult to justify in current market conditions.

BSE though in sweet spot … Only risk is reduction in speculation activity

Equity Option market has increased to 33% of GDP i.e. nearly $1.4 trillion which was around 1% in 2015 …

Projecting serious gr in equity options from here on can be dangerous for economy as losses and gains can hit economy in multiple ways esp if profits are going abroad and losses are incurred within India …

Previously similar incidences have happened in Japanese and Korean market and regulator push has crashed the market dramatically …This risk needs to be considered while buying BSE at current levels

What matters is to take a realistic sense of possibilities in front of you.

BSE is a part of extreme cyclicial industry, and is currently at peak cycle and peak valuation. Does it mean I am negative on its prospects, absolutely not, but markets are volatile and BSE has to take its share when it falls, with reduced trading activity across board.

Current bear market is already causing reduced trading volumes. We know that this too will pass, but there will be pain till it lasts.

So, calling BSE a secular growth story is not approprite in my limited understanding, however, BSE may continue to take away market share from NSE going forward, and may increase option turnover even in a falling market.

You are right Amit that overall Option market has dropped almost 40 pc from its high , but despite that BSE volumes has not gone down much , the reason for that is consistent increase in its market share and I think govt also supports the idea of 2 very strong exchange as it does not supports any monopoly , most of the govt recent action points towards it

During this market downturn, BSE retained its premium, rapidly expanding its market share. Whether this trend will persist after the market recovers remains uncertain, but there are signs indicating a possible continuation.

Why this is happening is more important to know so that we understand sustainability of the move …GOVT wanting something does not mean people will trade accordingly …

Are specific agencies supporting option trade on BSE … What is their motivation since there no major cost difference …Unless we know this can fade pretty fast as it did post post BSE IPO

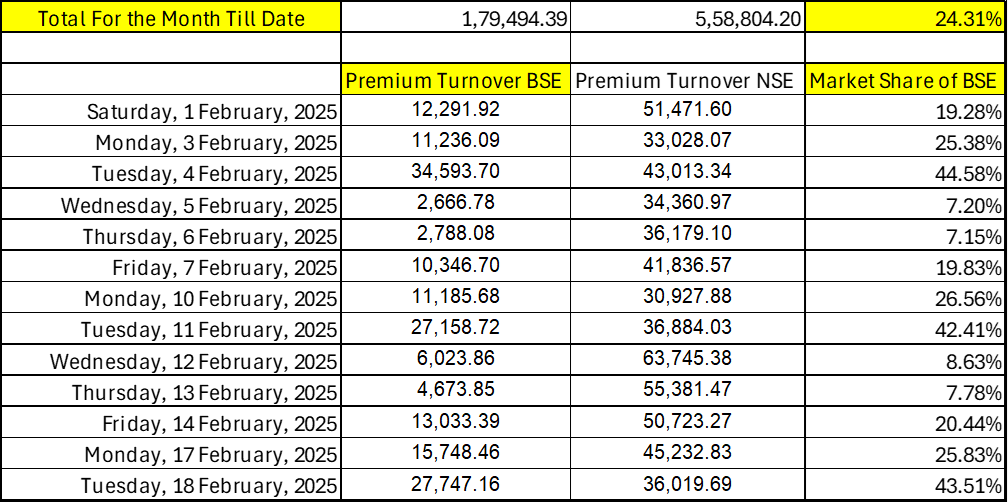

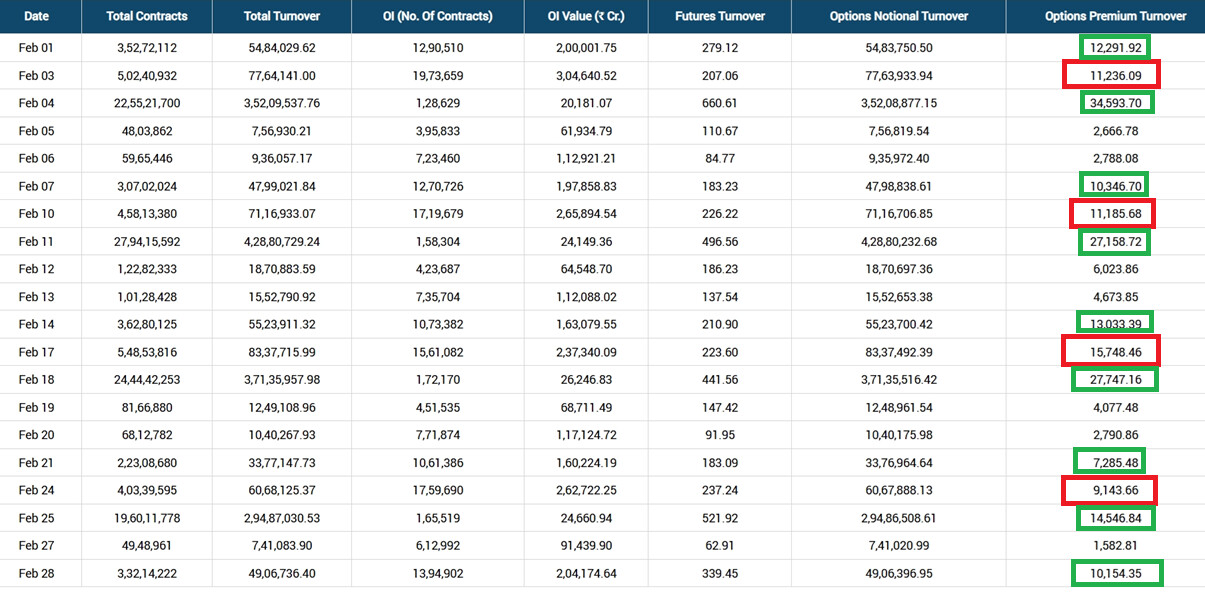

NSE is moving expiries to Monday (Notice Link). I checked the Premium Turnover data for Options for BSE in Feb.

Wed & Thur [no boxes] are the lowest volume days for BSE. They are 20-30% of volume of other 3 days mentioned in next point.

Tue are the highest [Green Boxes AFTER RED], with Mon being 2nd highest on most weeks [RED box], Fri is the 3rd highest [Green Boxes before RED].

With NSE opting for the center day i.e. Monday, it seems to be playing to capture the BSE’s Fri & Mon volume build up and drying out the OI for Tue.

Will BSE change their Expiry day? If yes, what day? Fri?

The news and regualtory actions e.g. “recent proposal by Sebi to tighten the way outstanding positions in stock futures and options are calculated in an attempt to reduce the possibility of manipulation in derivatives trading” might be forming some -ve’s for BSE.

IDEALLY they should also switch to Friday… But given that now Thursday is free and all traders for years have experience with Thursday may be thursday will be the best . it will kill NSE,as people will just switch to BSe and carry on with their old strategies

Recent interview by Mr. Sundaramam Ramamurthy sir MD CEO of BSE suggests that he will always take decision considering consensus of the Market Participants and he says he wants to make BSE one of the world class exchanges primarily focusing on customer delight in its services.