With new coalition government and SEBI board level changes we can likely see the regulatory over action on derivatives market may reduce.

While there is excessive stock level derivatives contracts which exchanges so reduce it also provide more liquidity to overall futures and cash markets when there is more trading in the market which disperses risk and reward overall so it benefits when markets are volatile…tough inhertly increasing the volatility also

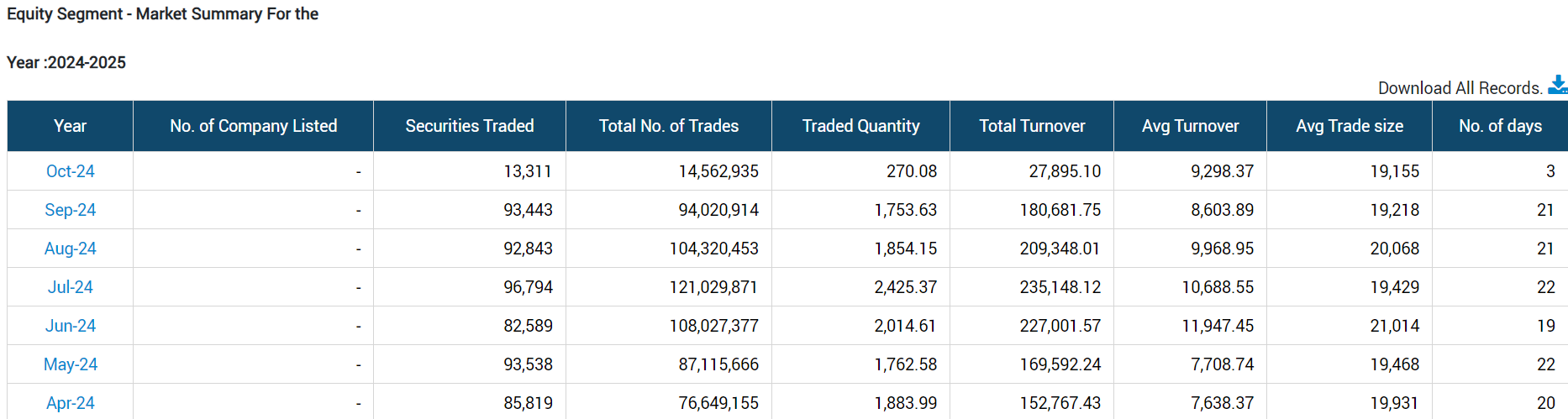

Quick snap shot of BSE’s performance during the quarter(Q1 2025):

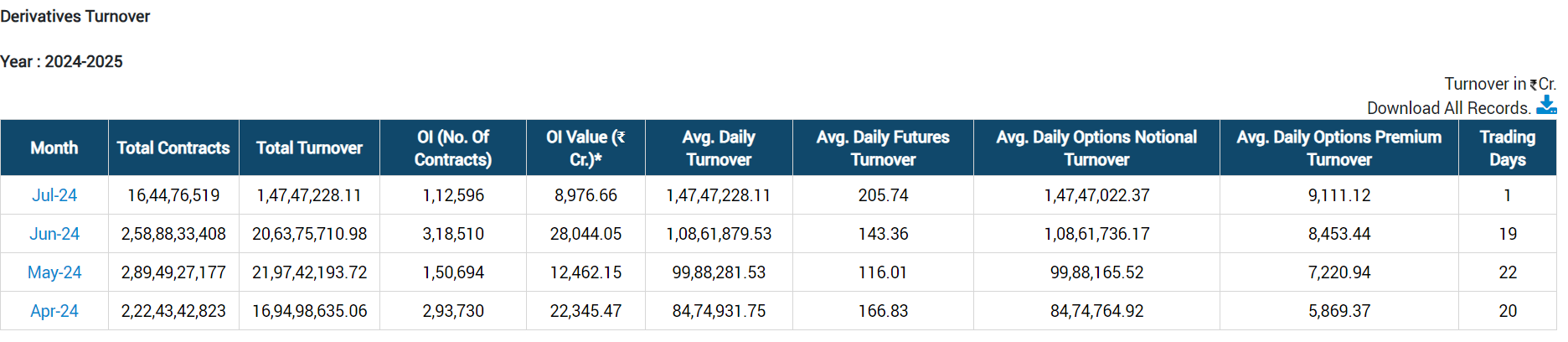

Derivatives:

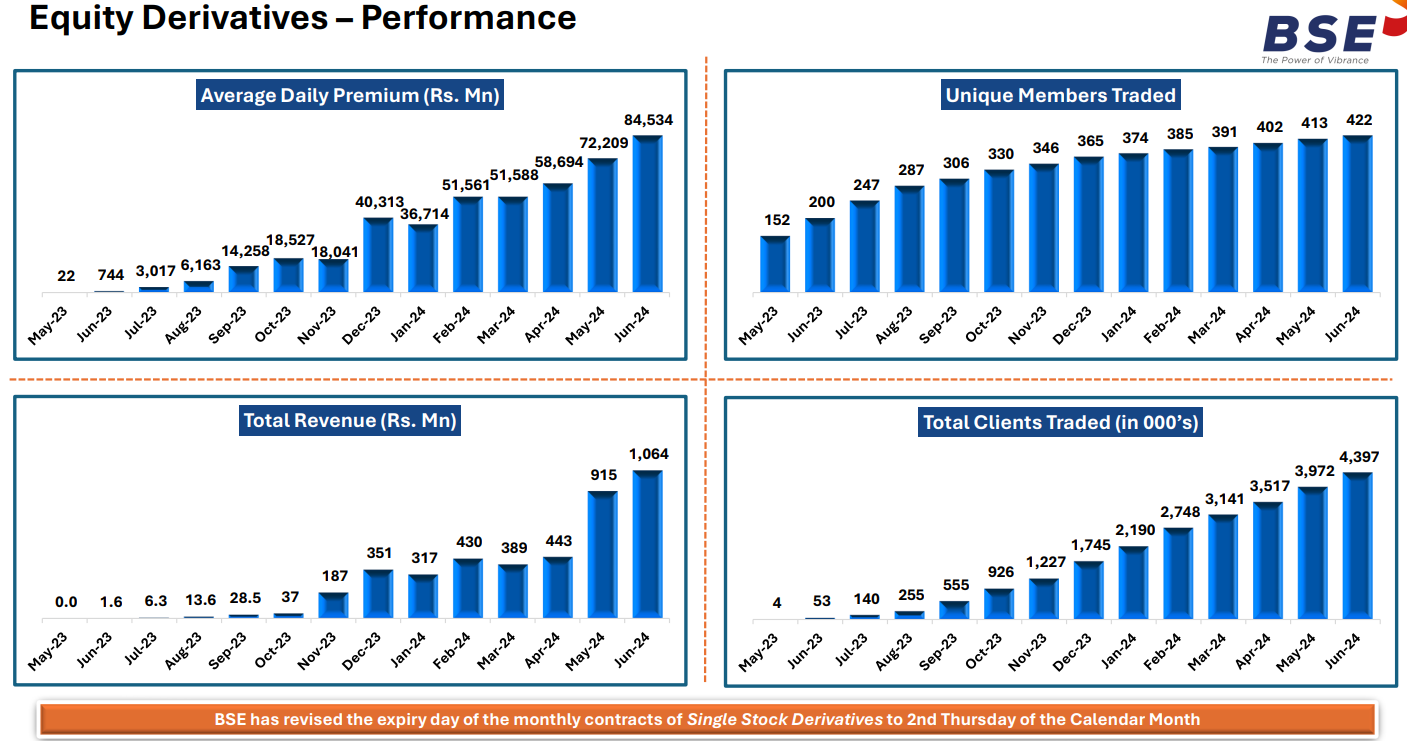

The derivatives volume in general has been showing growth month over month during the current quarter - average daily premium turnover has moved steadily to above 8000 Crore during the month of June. The growth in premium turn over coupled with significant increase in price will lead to an exponential growth in revenue from this segment during the quarter. I expect the revenue from this segment to be at least 50% higher as compared to March quarter - the profit from the segment would be a positive surprise when the results are declared.

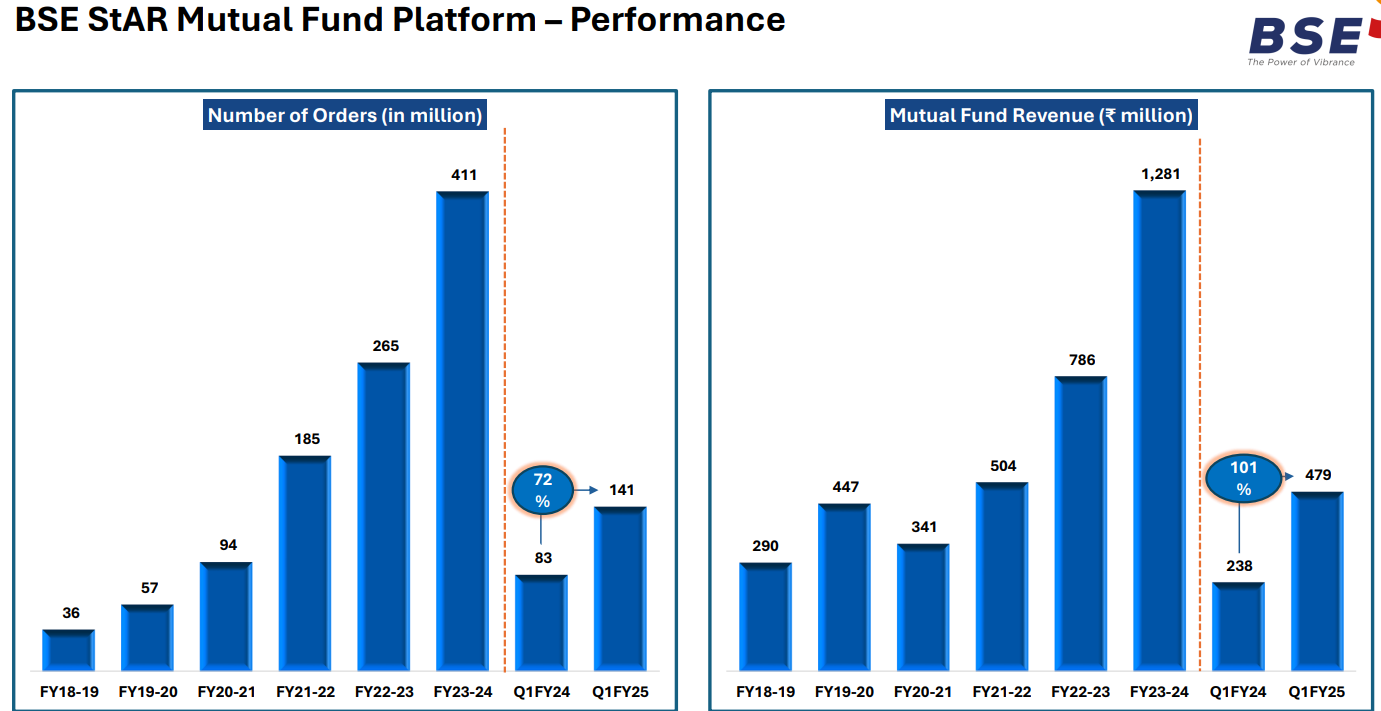

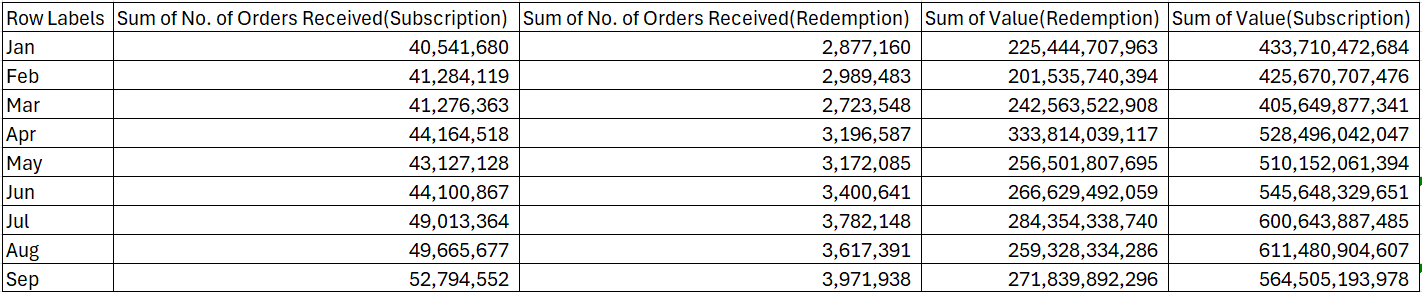

Star Mutual Fund: Robustness in growth continues with the total number of subscription and redemption orders showing an uptick in excess of 25% and 40% respectively as compared to Q4 2024. Expect the segment revenue and profits to grow by at least 25% as compared to Q4 2024.

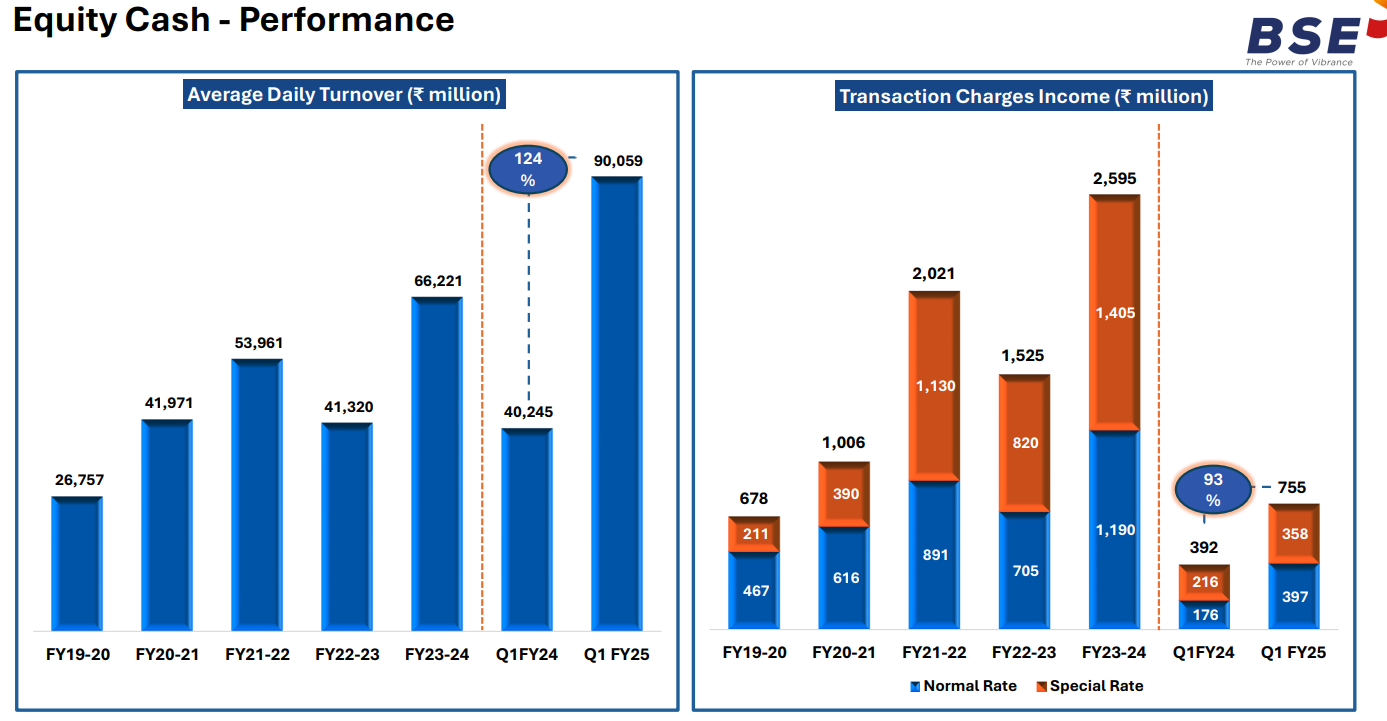

Cash Segment: The numbers seems to have slightly dipped as compared to Q4 2024. Expect the results to be slightly lower as compared to last quarter.

Currency and commodity markets are not showing any sign of improvement.

Overall, the results are expected to be blockbuster for Q1 2025. Looking forward to managements commentary on the new single stock futures product that is being introduced from July 1st.

If this happens how much it can impact on the BSE business? Any views? If only 10% traders make profits it will discourage them also due to higher taxation. Can it affect the long term prospects of BSE.

Did i say the numbers are going to be outstanding? Yes, now we have official confirmation.

Snap shot of standalone numbers along with comparison with March 2024:

Revenue up by 30% and Profits up by 120%!

See the press release here.

Leading stock exchanges BSE and NSE on Friday revised their transaction fees for cash and futures and options trades after markets regulator Sebi mandated a uniform flat fee structure for all members of market infrastructure institutions.

The revised rates will be applicable from October 1, the exchanges said in separate circulars.

BSE has revised the transaction fees for Sensex and Bankex options contracts in the equity derivatives segment to Rs 3,250 per crore of premium turnover.

However, the transaction charges for other contracts in the equity derivatives segment remain unchanged.

For Sensex 50 options and stock options, BSE charges a transaction fee of Rs 500 per crore of premium turnover, with no transaction fee applicable for index and stock futures.

According to NSE, the transaction fee for the cash market will be Rs 2.97 per lakh of traded value.

For equity futures, the fee will be Rs 1.73 per lakh of traded value, while for equity options, it will be Rs 35.03 per lakh of premium value

The impact on CDSL may not be substantial because this regulation is more about managing market speculation rather than directly affecting depository functions. while this regulation could slightly reduce trading volumes, it is unlikely to have a major positive or negative impact on CDSL stock directly.

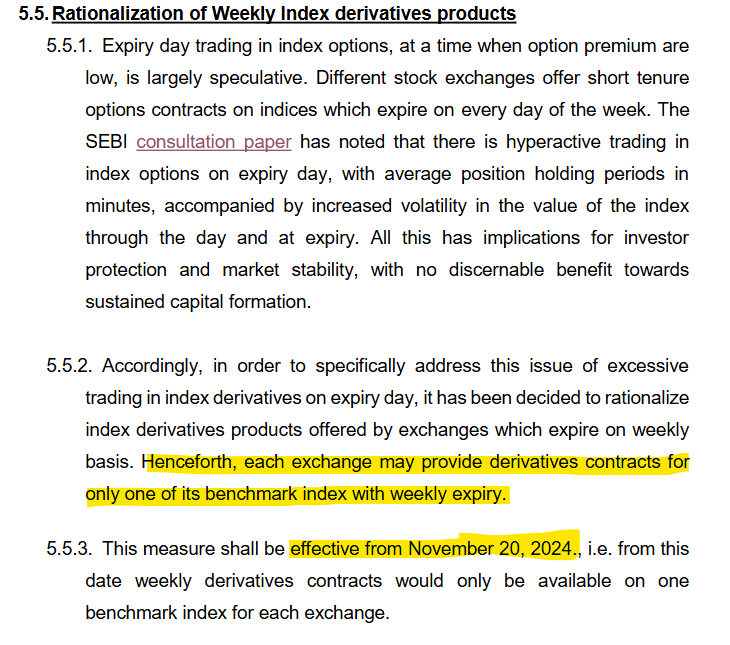

One index option per exchange in weekly expiry segment would make NSE choose between it’s two crown jewels i.e. Nifty or Nifty Bank. Assuming speculation market size to remain the same [i.e. INR 10,000 crores index option market], BSE which now makes INR 1,200 cr would gain market share with some speculators shifting the trade from NSE delisted index options [w.e.f 20 November 2024] to BSE.

Mental models:

expected market share gains;

risk reward seems in favor [FY’25 expected PAT 1100-1200 crores; PE [FY’25]: 45-50]- this is without factoring market share gain]

Breakout with huge volumes

EDIT:

To monitor:

Loss in revenue due to increase in lot value and delisting of one index option by BSE (current has 2) is lesser than increase in revenue due to market share gains from NSE

Quick snap shot of BSE’s performance during the quarter(Q2 2025):

Derivatives:

On an average premium turn over has grown by about 15% as compared to Q1 - since the price revision was effective May 2024 - I’m expecting the revenue from the segment to grow in excess of 20% as compared to Q1 to reach around 300 Crore.

Star Mutual Fund: The growth momentum is very much intact. The number of subscription and redumption orders processed has grown by about 15% on an average. I’m expecting the revenue from the segment to grow to about 50 Crore for the current quarter.

Cash Segment: The number of trades has grown in excess of 15% as compared to Q1 2025. While I have not performed category wise performance, the revenue that I expect from the segment is in excess of 80 Crore.

IPO Market: More than 40 companies hit the IPO market during the current quarter as compared to about 20 companies during Q1 - I’m expecting the revenue from services to corporates to reach in excess of 30 Crore.

The single stock futures and options has not really gained much traction. Management will need to focus on this after the firefighting expected during the months of November and December due to change in weekly contract expiry.

Overall, I expect the numbers for the quarter to grow by atleast 10% as compared to numbers reported during Q1.

NSE has chosen NIFTY as the weekly expiry index. Any news on BSE? Hope they choose to go with BANKEX weekly expiry instead of SENSEX. Any views of the community?