Results for BSE out: Better results than the street expected mainly attributed to increased treasury (due to FNO) and better IPO book building cylce.

Revenue up 59% YoY

PBT up 257% YoY

Commentary from management:

The company has been bleeding heavily in settlement charges due to which the prices were increased earlier than expected. But Sensex has achieved critical mass way before expectation which allowed them to do this

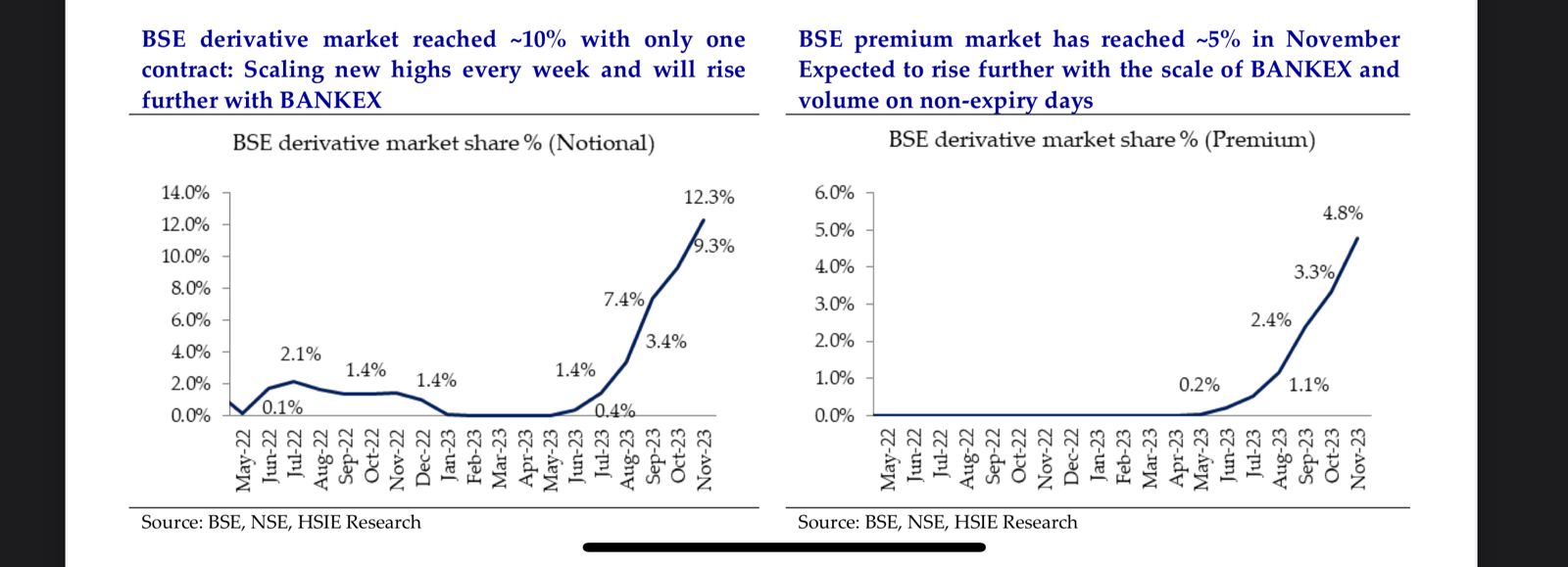

Bankex has achieved the same volume in 4 weeks that Sensex derivatives took 12-14 weeks to achieve. Prices will be hiked in Bankex as well when critical mass is achieved but surely be done

Due to most trading happening on expiry days the premium turnover / notional turnover remains lower than NSE. Focus will remain on increasing and developing the longer dated expiry volumes (Upto T+2 weeks) to increase liquidity and price turnover

New products are being worked upon and eventually be released in the market; however what days still remains uncertain

Working out things with brokers, members and NCL to further reduce down these costs as the volume in derivatives keeps increasing

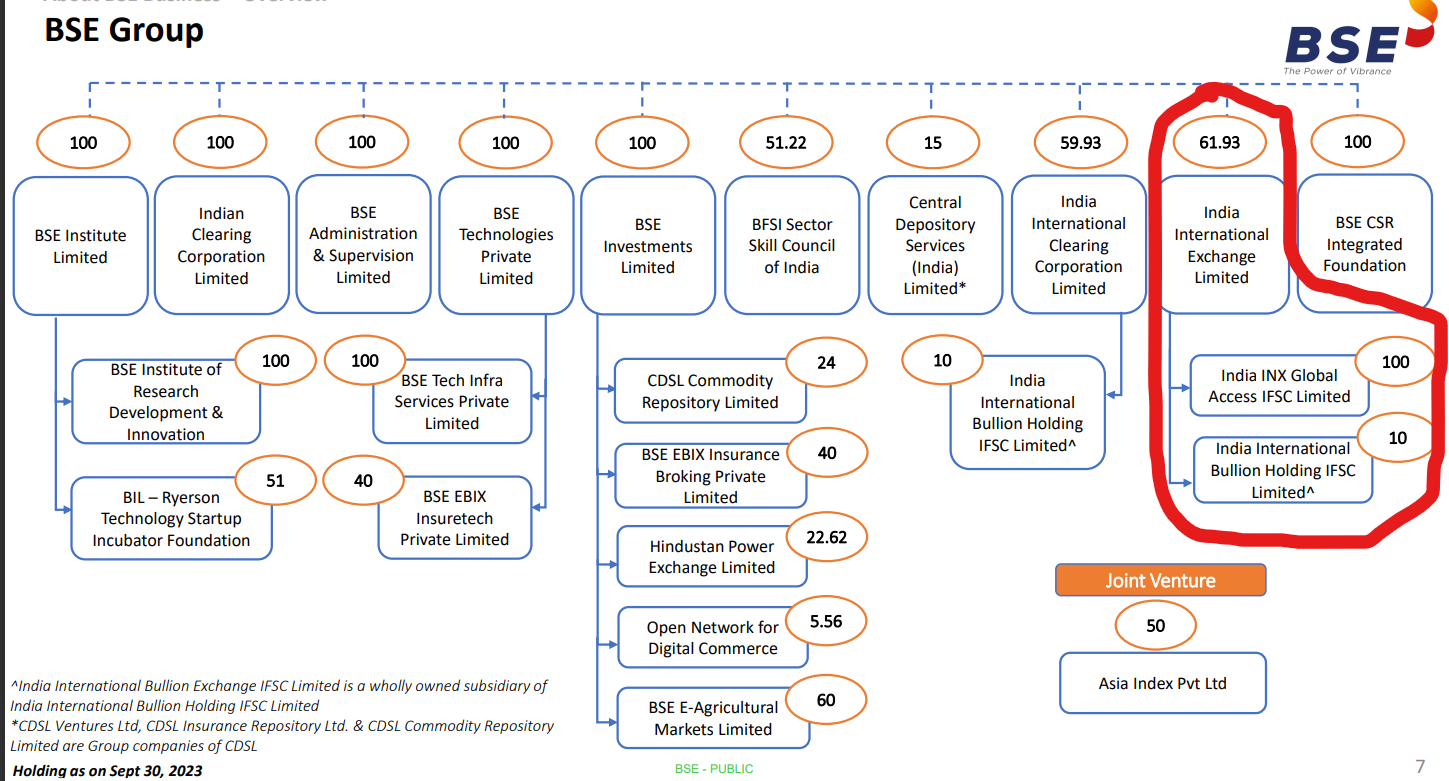

How is this going to work? Who will control the GIFT city exchange? NSE or BSE? The unified exchange will be competing with SG/HK/LSE/NYSE bourses, and will be the GIFT City IFSC gateway for Dollar Inflows to Indian listed stocks/bonds etc.

BSE holds 61.93% indirectly in this. Any thoughts from boarders on this development?

Relooking at some of the key statistics from BSE for the quarter ended December 2023:

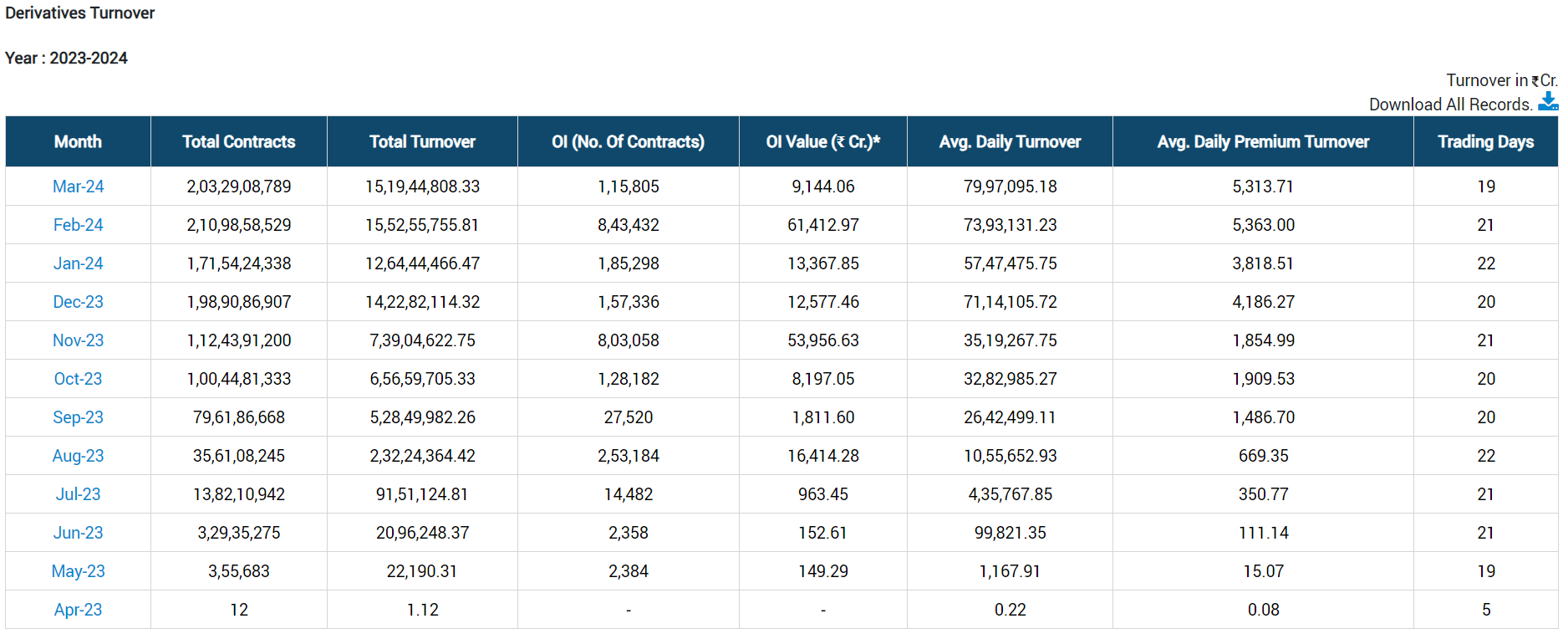

Derivatives:

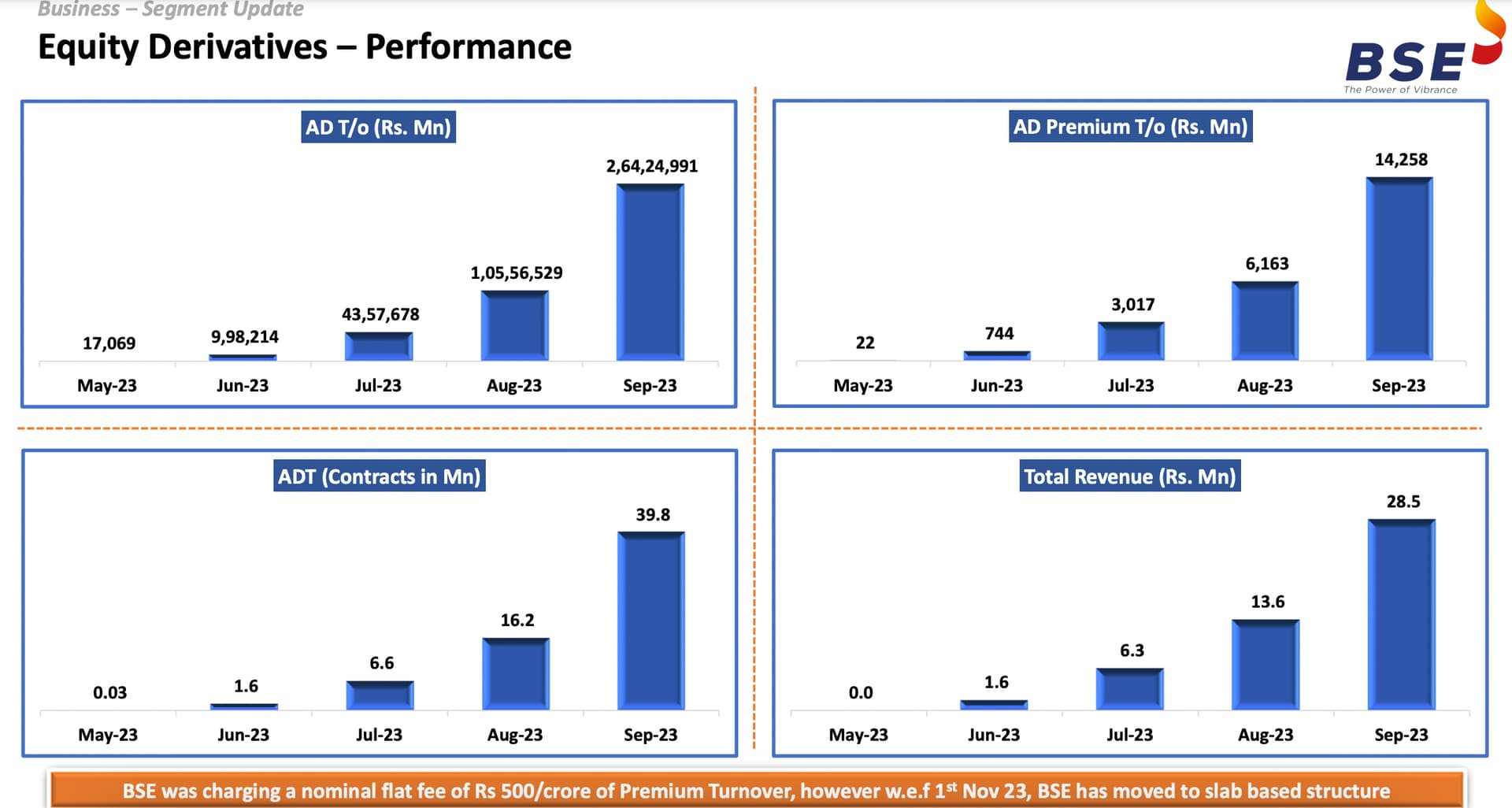

The numbers are growing at a brisk pace irrespective of significant change to charges from 1st of November. Market participants apatite for trading in Sensex and Bankex derivatives are growing week after week. While the tired pricing structure makes it difficult to arrive at the expected revenue for the quarter, my rough estimate of revenue from this segment is that it should exceed Rs. 15 Crore for the quarter (assuming average realization per crore of delivery trade to be Rs. 1500).

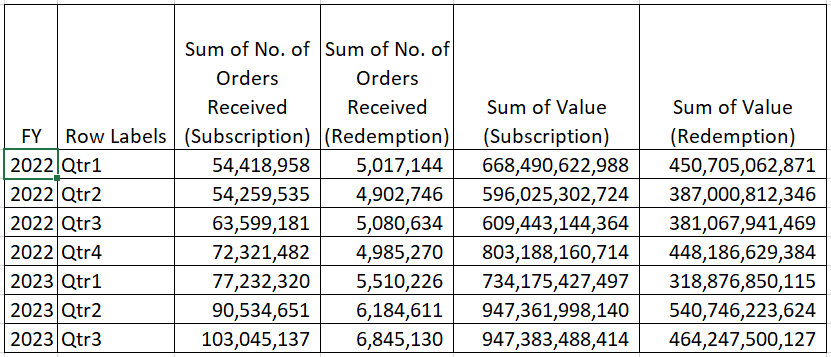

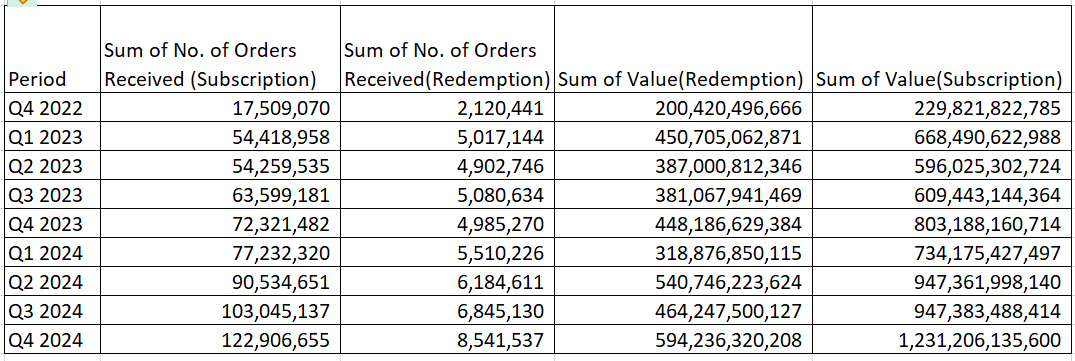

Star Mutual Fund:

The subscription orders grew by about 14% as compared to Q2 2023 and by 62% compared to same quarter PY. The revenue from this segment will grow in line with volume.

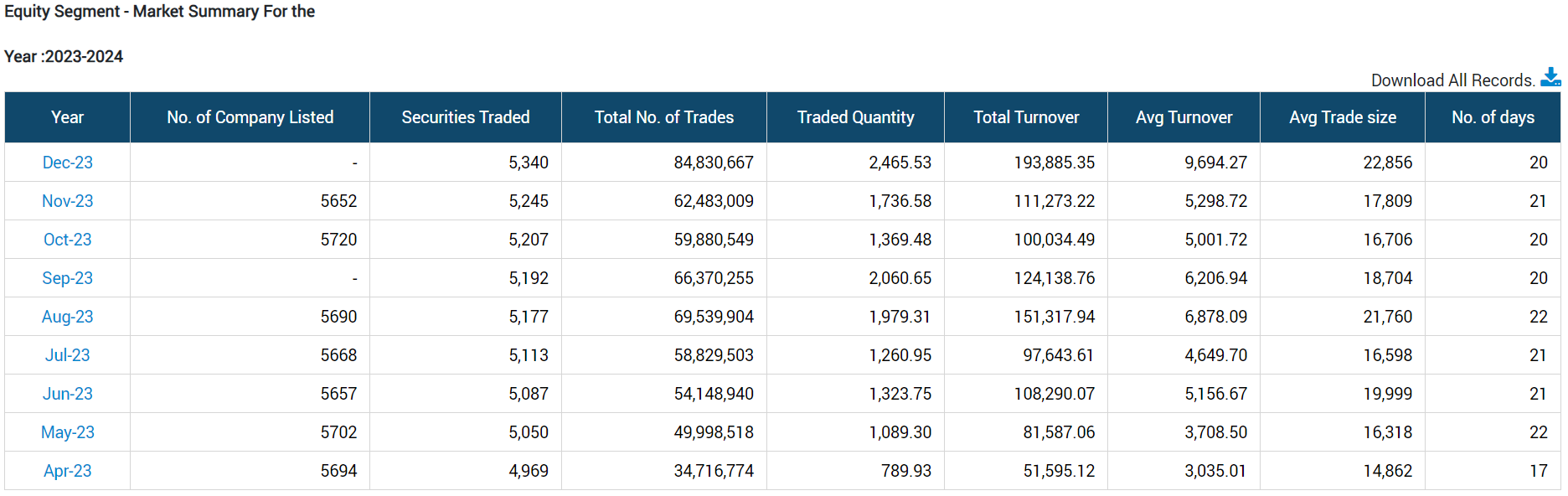

Cash segment:

The segment seems to have got a rub-off from the robust growth in derivatives resulting in a 6% growth in number of trades as compared to Q2 2023. The revenue growth should be robust.

IPO Market:

The number of new companies listed on BSE during the quarter broadly remained same as last quarter and accordingly the revenue from the segment should be stable when compared to Q2 of this FY.

Other observations:

Buyback that was announced during the previous quarter failed due to lack of participation on account of sudden spike in share price during the current quarter.

Commodity and Currency markets are not really showing any real momentum.

Overall I expect the results for the current quarter to be the best one from the time BSE got listed. Let’s wait for fine prints and management commentary once the results are published.

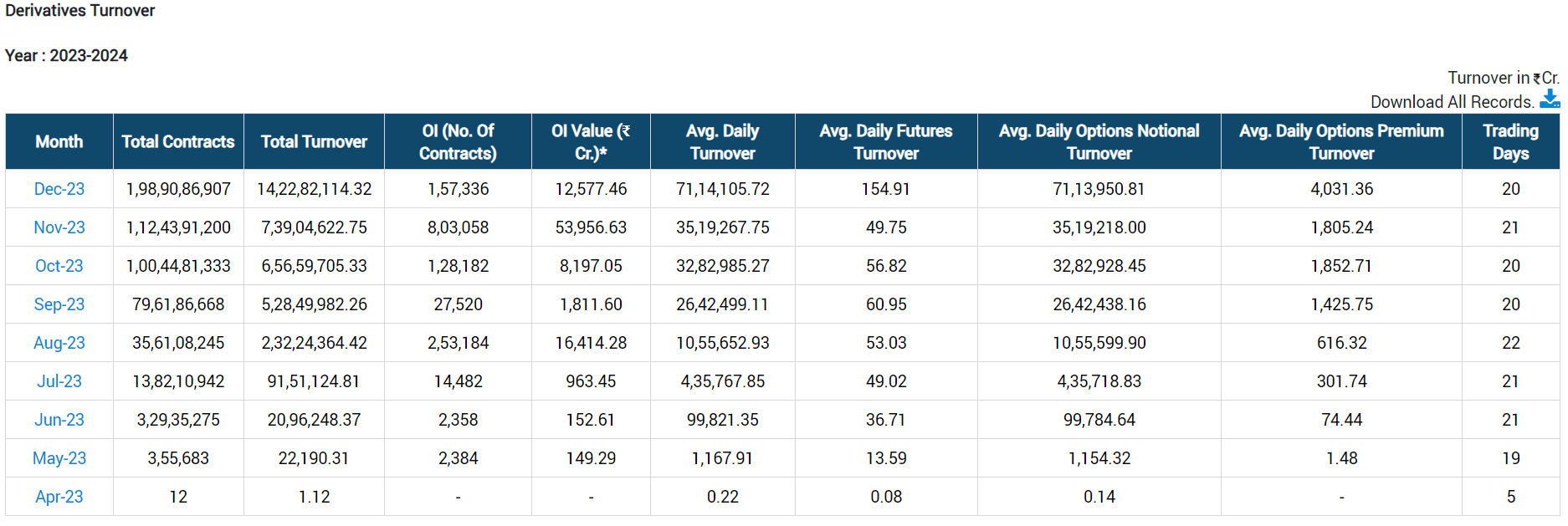

Off late i have seen sensex derivatives contracts are not growing much rather have became stagnant. That can be seen partly from October & novermber’s data also of similar ADPT. December growing mainly because of Bankex contract. Still many large traders are avoiding sensex because of random ticks on 0DTE. Need to see, when those large traders come to sensex. It is circular nature - when they come, liquidity will improve more & So on.

For BSE, there is not much scope, apart from Friday & Monday - Because all other 3 days have decent volume & interest in NSE derivatives.

Have u heard last concall ? Even though they are growing at decent pace in derivatives, actually they are making losses here - Bcoz settlement cost is higher then revenue & 90% of settlement is going through NSE’s settlement exchange. So, despite BSE making so much efforts, NSE is gaining indirectly from it rather than BSE - That’s what my understanding is. Any opinion on it ?

Regarding my query no. 2, I got answered from them.

So basically in Q3, they earned 56.6 cr. revenue for equity derivatives segment. While they paid 44.4 cr. towards NSE clearing house (These 44.4 cr. includes all segment so we can assume 80% (nearly 33 cr.) of it for equity derivatives. Plus we need to add some charges of ICCL as well (But anyhow it comes back to BSE’s profit as subsidiary). So unlike previous quarter, this quarter they actually made profit from equity derivatives segment as well.

Also if we compare October & November’s Avg. daily turn over for equity derivatives - it is almost same however revenue for November month is 18.74 cr. Vs. 3.7 cr. for October month. So clearly the revision in charges is working on their way.

Another important aspect is - SGF liability comes to Clearing house & not on exchanges. & for BSE - majority (80-90%) of trades are settled by NSE clearing corporation. So, although BSE have to pay huge expenses for NSE clearing corporation the onus of SGF liability for such trades largely goes to NSE clearing corporation.

For BSE, in currency segment they are continuously loosing market share & volume & now they have concentration risk of few large customers (Like banks, Institutions) that’s why despite lower volume they have to incurred more SGF liability for currency derivatives.

My view:

In equity derivatives segment - If they can fetch more liquidity except 0DTE, particularly on monthly expiry then it would be bumper for them. As of now, these seems far ahead. Bankex is gaining popularity on Monday however, still many big traders are avoiding Sensex & Bankex. Sensex volumes have become almost platue since last 2 months.

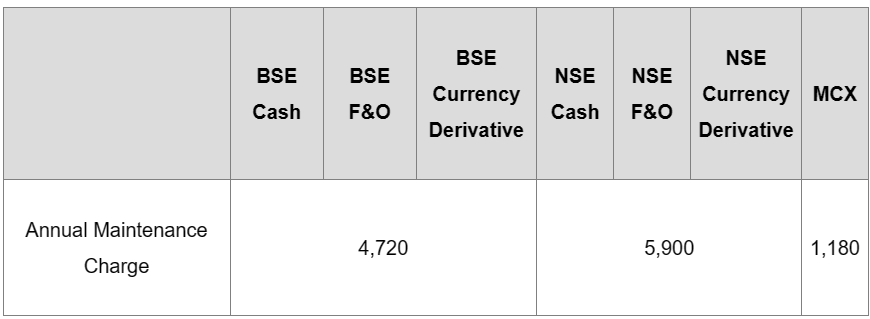

Below is the yearly AMC fees that are being charged for each Authorised Person of a Broker. BSE is priced lower, but this might be another revenue source. Need to wait till Qtr end to see how many APs are still registered with NSE, BSE.

Quick snap shot of BSE’s performance during the quarter:

Derivatives:

The Sensex derivatives volumes remained largely range bound during the quarter. Bankex volumes are picking up slowly. The average daily volume improvement is largely on account of Bankex growth.

Star Mutual Fund:

Robust growth in subscriptions and redemptions orders - Noted nearly 70% growth in both subscription and redemption as compared to Q4 2023. Expect this segment to deliver its best ever results till date.

Good question, lets see how this plays out. It will definitely impact results of Q1FY25, not sure if they will make provisions for this in Q4FY24.

BSE has issued a clarification on this matter. They say totally from FY 2006-07 to FY 23-24, they will need to pay ~Rs.165 Cr (including interest, 68.64 & 96.3 ) + GST that comes to ~Rs.195Cr. 195Cr is basically 1 yr profits based on previous years earnings, but since last 1 year profits have jumped up significantly, this is approx 2 quarters profts. STILL a BIG NEGATIVE impact.

Wonder how NSE has been paying this? Are they in similar boat or they have accounted as per SEBI?

BSE is gaining market share in derivatives segment, however, profitibility is miniscule in this segment because

a) They are charging less compared to NSE to lure customers. However, recently they have inicreased charges significantly comparabe to NSE.

b) NSE Clearing Corporation is charging BSE heavily on derivative trades.

c) Recent SEBI order on calculating regulatory fees based on notional turnover, will eat away lot of profitibility.

Derivatives turnaround has raised investors expecations multifold from BSE, and that’s visible in BSE price performance during last one year. I think BSE will have to live upto investor’s expectations to justify current price.

Yes, there is a possibility that BSE may compete with NSE in derivatives in future, but that’s a big question mark.

Overall BSE profitibility is running all time high, due to huge capital market tailwind. Transaction revenues have increased a lot due to on going bull run.

Again, BSE has rewarded shareholders with rise in profits, but I think, the increase in profitibility is not structural, due to cyclical nature of the capital markets business.

STAR MF also has done pretty well in terms of number of transactions and revenues, but to ME, it is not a product that commands pricing power. Pricing power rests in the hands of mutual funds, who continue to reduce the transaction charges as volume at SATR MF grow.

While AUM of Mutual Funds collectively have grown many times in last few years, BSE STAR MF is far behind in revenue growth, when compared to AUM rise of Mutual Funds.

BSE has not increased dividend for FY24, despite

a) Increase in profits

b) Sale of CDSL Stake

c) No need of growth capital and

d) Sitting on tons of cash

I failed to understand management rational behind the same during the concall. However, for most of the investors it’s a irrelvant topic as share price is running all time high.

Summarizing, Capital market tailwinds has increased profitibility and share price performance of BSE. To ME, Underlying business is good, but share price performance is running ahead of fundamentals. Other investors may have opposite views and no body needs to agree with me. Take your own judgement.

Disclosure - Invested. Amature investor , not a SEBI registered analyst

On May 8, 2024 BSE announced that it will launch single stock futures starting July 1, 2024. The product will be free of cost initially and will be offered fortnightly. BSE may offer a lower number of stocks to begin with, compared to the over 180 stocks offered by NSE in index derivatives.

On Point 4, dividend , why is it hard to understand what they have not paid out full Div. Firstly Div paid was Rs 15 highest ever. Yet it was not 100% , because as explained they have made a huge provision for the SEBI fees, they have to plan for future growth which means significant TEch and hardware expenditure to introduce new products and ensure scal. so its fine that the firm keeps the profits instead of payout. The Reserves are always needed for various markets guarantee funds and growth will keep increasing in Derivative taking off .

I dont think brikers will just come back because charges are higher now. Yes some impact will be there but the major growth was because of huge outreach process and tech integration that MD has done vist visits to over 1700 markets participants. thats huge sell job and once people get used to an index for trading they dont give u for few hundred rupees

The BSE is heard to be reaching out to custodial participants (CPs), trying to persuade them to switch to its clearing corporation ICCL. But the bourse is not having much luck on that front. While it has managed to grow its derivatives volumes exponentially, CPs don’t see any merit in shifting because the charges are the same. But the bigger hurdle is the SEBI rule that CPs can sign up with only one clearing corporation. That is because inter-operability across both clearing houses does away with the need for CPs to sign up with more than one clearing house. BSE’s challenge right now is that it is hurting from a higher SEBI turnover fee as well as the clearing charges it has to pay for the trades cleared by the NSE-owned NSCCL. NSE too is seeing its SEBI turnover fee rising faster than premium turnover, but the charges it pays to NCCL ultimately reflects in its consolidated financials. Source

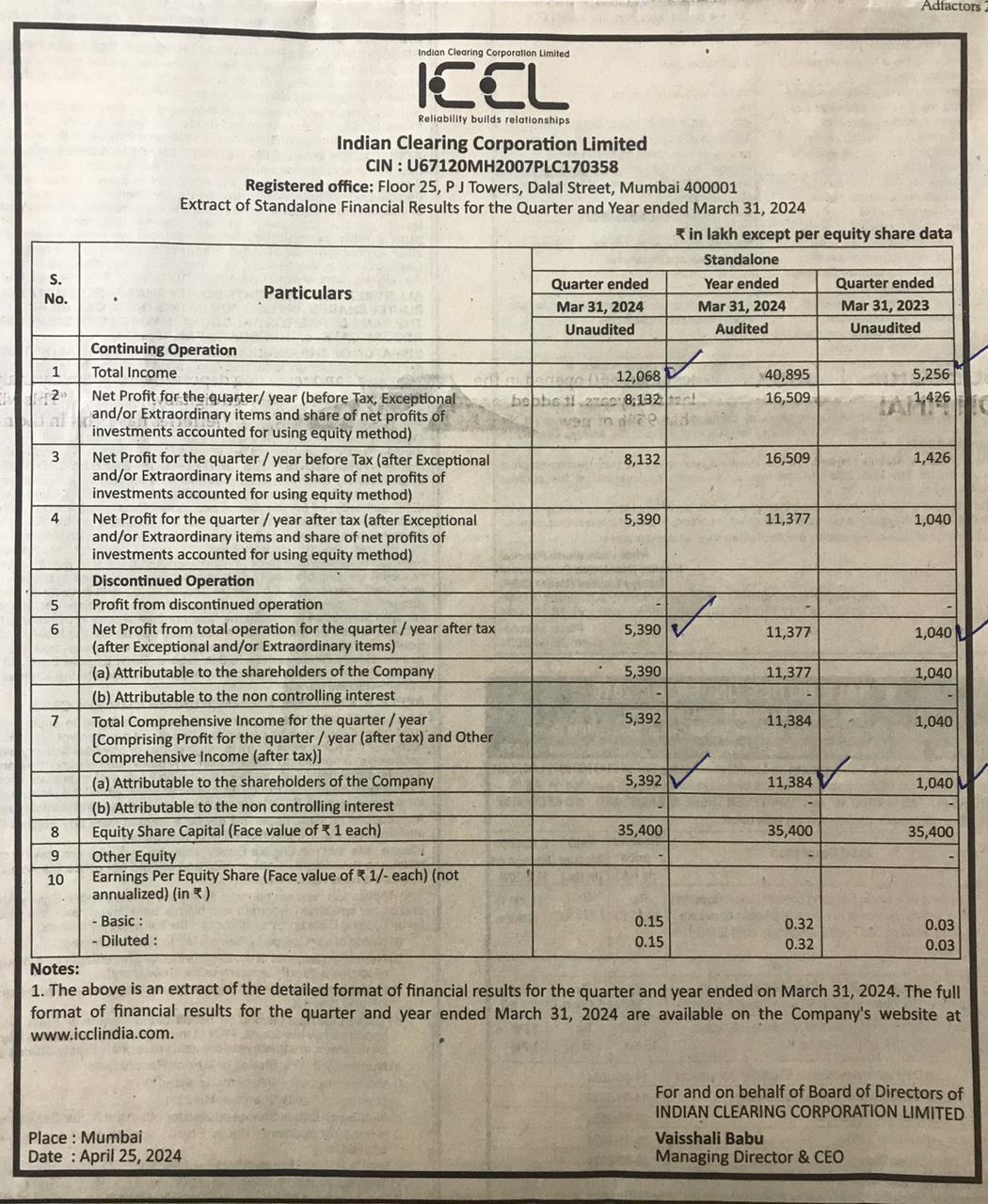

ICCL Q4 results.