I have a few questions on the financial statements published by the company for H1.

-

I see the trade receivables for H1 as Rs 53.2 CR in BS. Isn’t this a big amount compared to the recorded sales of Rs. 168 Cr in H1?Is this normal to have this level of trade receivables? I could not get a chance to compare for previous FYs.

-

I seebelow in teh cash flow statement:

Does anyone know what purchase of Property for Rs. 6.6CR? And what is the Rs. 23 Cr purchase of investment? These seems to be quite significant values compared to PAT.

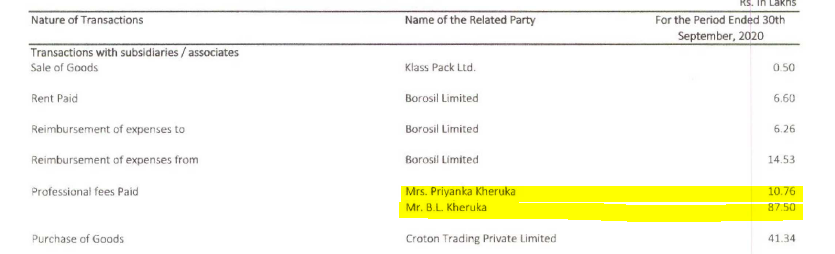

- I see below in RPT statement submitted by company for H1. Do we know why are these professional fees paid?

I do not have much information about the management of Borosil, hence wanted to check if these items ring any alarms?

- Out of 168 Cr sales, around 114 Cr was in Q2 . This means average sales of 38 Cr per month. Assuming 18% GST on this, average gross sales would be 45 Cr. so 53 Cr of receivables means hardly 35 days of sales in receivables, which is extremely low.

- 6.65 Cr Capex for 6 months - Refer recent concall. 3 Cr was spent on refurbishing one glass tempering line and around 50 Lakh per month is the maintenance capex. About investments, since company have spare cash, it must be investing in debt funds so 23 cr invested. Please note of sale of investments of 16 Cr below that line in cash flow.

- No idea about professional fees paid.

Talking Point With Borosil Renewables’ Chairman Pradeep Kheruka

- I think it is not correct to see the trade receivables with GST while revenue without GST. We should measure this in single unit (and i also assume that company will not mention the sales without GST but trade receivables with GST). And in fact if we looks at the trade receivables only for Q2 (not H1) this number looks bit more alarming.

But I am getting a mixed opinion now about this as i read more on the last year’s BS (revenue ~270CR. vs trade receivables of ~40CR for FY2019-20). So this number of 53CR does not look alarming in that sense. However, again, I see in the P. Kheruka’s interview that @ranjeet posted just now that the order book cycle is just 45 days. This means the trade receivables is the almost entire order book cycle. Again as long as company can maintain the working capital cycle, this should be OK. Mr Kheruka also states the same that there is no alarming situation on receivables.

- OK I see the investment of 14Cr in BS.

As such it is more comforting to hear from Mr. Kheruka that out of remaining ~300Cr CAPEX that is required, company will do 120CR out of internal accruals and ~180Cr debt. Believe this is more prudent way to go ahead for CAPEX (though i would like to see the the 120Cr accruals in BS as well in some or other form).

Now that the company is having the Govt support under the belly in terms of recently announced duties and favorable environment with competition having ~40-50% EBITDA which they can follow as well in short term, this will surely attract the competition (as Pat Dorsey says “the success is followed by the competition as surely as night follows the day”). I expect someone to announce the entry in this space in next 1-2 quarters given the favorable macro-economic environment.

Sales are mostly shown without GST (unless someone decides to show gross sales and show GST as a cost) and receivables are always with GST (as GST is charged on invoice and becomes receivables along with the sale value from customer). Hence I reiterate that I do not find anything alarming in receivables which are low in my opinion for any B2B business. (most of B2B have 60-90 days of receivables)

About competition, I do expect competition to come in but if BR is taking 18 months to add 500TPD furnace, I expect at least 2 years for any new comer to set up and fine tune the process to come to the level of BR.

Super interview… the questions were just point blank. I visited almost 3 module manufacturers in the last 2 months. The only bottleneck is glass, as of now the price is INR 1200-1300 per glass till Dec, there may be an price increase from Jan to March but has not yet been confirmed by BR, may or may not. Actually most of the Tier 2 type of module manf are crying for glass, some have even shutdown their plants as they are not able to supply to the orders. for eg one of manf needs 45000 glass per month and they are supplied 1500 per month by BR. its a scary situation out there for Module manf. on top of it CVD from Malaysia. Hope too much positive does not turn into negative for BR.

the invw which has just been uploaded clears the doubt on receivables, which you also have nicely explained. They do cash and carry and may be to their major customer like Warree etc there may be some credit but otherwise there is absolutely no credit in this business. they are in super demand. hopefully he does not give too many invws like this

I don’t think it is possible as per Ind-AS.

However your point is correct, revenue from operations does not includes GST.

I feel you need to assume conservatively only 30% price increase for the current quarter (as sales booked in Oct may be at old rates and sales booked in Dec would be with 60% price increase . Also price increase may differ from customer to customer based on long term relationships). On costs, if they are running “flat out”, this will involve additional costs like overtime, higher power & fuel etc . So I would assume around 90 cr of operational cost. This will give around 60 Cr of EBIDTA. (40% margin). So I expect PAT to be around 34 Cr this quarter.

Very recently the company has launched new products like Selene: an Anti-glare solar glass suitable for PV installations near airports and Shakti: a very high efficiency solar glass in matt-matt finish. Amongst the upcoming products with enhanced features is the solar glass with Anti-soiling coating.

The company has a strong focus on expanding its domestic & exports footprints. The exports business has grown at a CAGR of 33% in the last 3 financial years. The European market is a major customer base for the company where it has now successfully started supplies of its newly developed products, i.e. 2.0 mm and 2.5 mm fully tempered glass. With additional production now available, it has plans to substantially increase exports by tapping more customers in Europe as also increasing presence in the Americas.

Detail news is behind the paywall… but I guess the details and conclusions would have been taken from the interview posted above by @ranjeet.

I am amazed at media coverage once stock starts moving upwards. Just 3 months back, a simple google search on company name would have returned very old news on this company and now you can see many news in different publications. I am sure company management also would be contributing to it but news media also likes to run after the success stories. Not that I am complaining…

Agreed too much positivity sometimes gets jinxed!. I missed the bus early and now think there is too much attention on the script. Plus 10x sales and 40x PE seems to be at the high end of valuation for the time being. Maybe will wait to get into the name. Suggestions are welcome to help me make a decision here pls

I know what you mean Chirag. I first invested in Gujarat Borosil more than 2 years back and averaged up recently at 130 odd and again at 172.

This is how I look at it:

-

PE is not a good metric in a segment which is only just beginning to bloom.

-

Borosil has a capable management and have proven to deliver quality. I expect them to double capacities every 18-24 months for the next few years atleast.

-

I personally think they have the capability to achieve and exceed one-fourth of Xinyi’s(World leader in Solar Glass) current mcap (1lakh cr) in the next 5 years, if things play out as it can.

-

Looking at Adani Green, it seems anything is possible (in the stock market). I did not invest there because of debt and general dislike for the Adani style of business. I didn’t see any reason to miss out here, hence averaged up. My allocation though is not a big % of my portfolio currently.

Having said that, I expect the monopoly to not sustain. The news on the ground is that Borosil is unable to meet the demand for solar glass currently and they are fully booked all the time, and it appears the management is wary of expanding too fast (but the stock is running up fast)

I am in same boat as you. I missed Adani Green even though someone recommended it to me at price of 40. Reason why I didn’t invest in Adani Green was because of bad financials. But I realized sometime stocks moves due to emotions and not fundamentals. It seems to be the case with Borosil too. Company is good with monoply. I haven’t seen Solar sector moving the way it should have been moved. But recently everybody started talking about Clean/Renewable/Green energy in the world and hence everything that is related with Solar going up. Tata Power might be next in pipeline since they are also moving from conventional to solar energy.

Now coming to valuation and fundamental, I agree stock seems at high end and company is not generating much profit. But I personally think this as a momentum stock until company start showing growth and generate profit on consistent basis. Company is showing some apatite by doubling the capacity which is a good sign. I am expecting Govt will put more focus on solar sector. I was listening to a concall of Rites Ltd and one of their subsidiary/partner is putting solar panel on the railway platform. So solar is gaining traction.

The next big thing that all renewable energy sector is focusing on is hydrogen.

Off late I come across many institutions are showing interest in renewable energy.

Management acknowledgement of employee performance is a good gesture, says something about their grounded ways to motivate workforce and culture

Good to see MD shreevar taking time to personally appreciate a young middle mgmt employee on 10+yrs in svc on LinkedIn

Good gesture indeed.

@Dev_S, this should be posted in Borosil Ltd/Borosil Glass VP thread. Shreevar is not involved directly in Borosil Renewables.

Interesting, knowing that these both are recently demerged entities, expected overlap in backend , though Shreevar resigned as KMP - although media interviews are given by Pradeep, Shreevar announced success of QIP on LinkedIn and Pradeep responded to each of messages

Also Shreevar shows up in promoter holding and is on board of directors as well.

Anyways same family ( and hopefully culture and values)and point was to highlight employees connect, will link to the borosil thread as well.thanks for highlighting it @Marathondreams

Edit on website - Site is up, covers basic info as corporate site.

Hope to see some good content and marketing materials - either different site or in here.