Borosil Ltd

Q3 concall and results highlights -

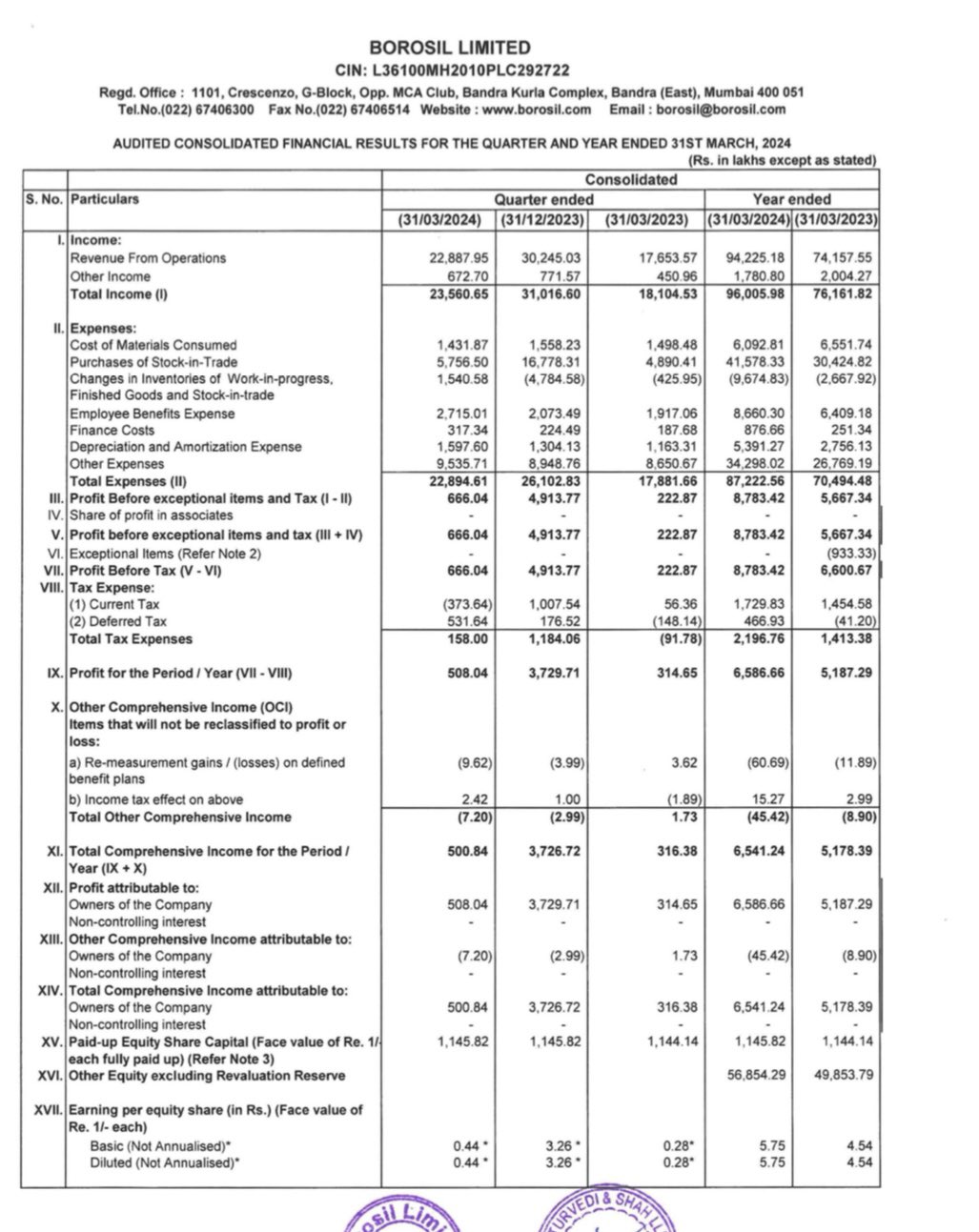

Q3 financial outcomes -

Sales - 302 vs 207 cr

EBITDA - 65 vs 26 cr

PAT - 37 vs 16 cr

9M financial outcomes -

Sales - 714 vs 565 cr

EBITDA - 125 vs 80 cr

PAT - 61 vs 48 cr

Segment wise sales for 9M ending Dec 23 -

Glassware ( under Borosil brand ) - 155 vs 138 cr, up 12 pc

Non Glassware ( under Borosil brand ) - 290 vs 235 cr, up 23 pc

Opalware ( under Larah brand )- 269 vs 192 cr, up 39 pc

This performance is superlative considering most other consumer durable, kitchen appliance, glassware companies reported a flattish Qtr / 9M performance

Post doubling of Opalware capacity and its utilisation, significant operating leverage helped in margin expansion. Also the RM and fuel costs were benign in 9M FY 24

Company has just commissioned a furnace near Jaipur making press - ware Borosilicate. This ll help the company reduce its import bill and also help lower RM costs. This will also help the company ramp up its exports

Company is guiding for a medium term ( 3-5 yrs ) sales growth CAGR of 15 pc plus ( includes good and bad years )

Depreciation expected @ 80 cr / yr post the commissioning of Jaipur furnace ( that is going to make borosilicate )

At present, Borosil Ltd has a debt of 180 cr on its books

Most of the growth reported by the company is volume led as the company has not taken any price hikes this yr. Some element of growth is also attributable to higher sale of premium products

Opalware capacity utilisation @ 85 pc at present

No major capex lined up for next 12-18 months as the company intends to stabilise the borosilicate furnace and improve its utilisation

The company’s consumer durable range is placed at the premium end. Company is not playing in the mass mkt segment. Also, company doesn’t manufacture any of these durables. They just procure, control quality and distribute

Current size of Opalware industry is around 1200 cr. It was around 300 cr in 2016. Company expects the Industry size to grow to around 3000 cr in the long term

Currently, the company is basically selling to top 100 cities in India. Aim to expand to next 100 cities / rural areas in future

Disc: initiated a tracking position, not SEBI registered, biased