apparently, it’s trading around borosil’s valuation multiples, be it p/e, p/b, ev/ebitda or p/s…

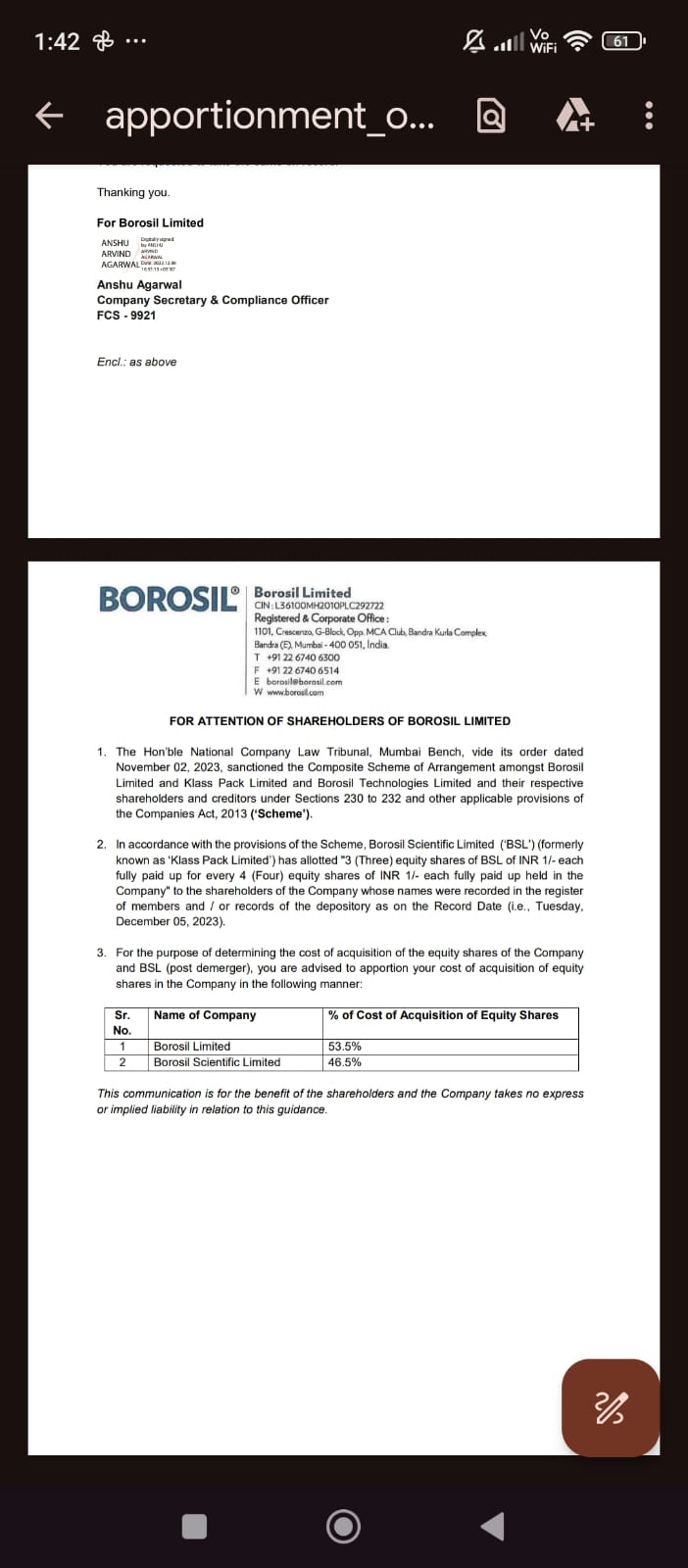

Hi a slightly novice question but how do we account for the acquisition of these shares? Will the share price be zero buy value?

yes it will be priced as zero acquisition value

Thats the basis for price adjustment as per me, in the past I also got shares of Borosil Renewables and they have been at 0 acquisition cost, because as an investor we receive shares without any cost price…but you can consult your CA for right advice…

@samm2211 @UrvilShah acquisition cost for bonus shares is zero. For demergers, the company in the scheme document gives a ratio / percentage as to how you should split your original cost of acquisition between the two shares

2 Likes

its not showing the average cost for me in zerodha, what average cost should I put, I got shares from demerger, I did not buy them. anyone can please shed a light on this ?

On 5th December 2023 (which was demerger date) share price of Borosil Ltd reduced from 445 to 375.

So you have paid around 70rs for Borosil Scientific.

Even if your cost of Borosil Scientific is showing as 0 but you have actually paid around 70rs which is deducted from your Borosil Ltd on 5th December.

1 Like

Vikas Khemani’s Carnelian Asset Management bought 2.5% stake from promoters in bulk deal on 28th June at Rs 318 per share

2 Likes

I am long term investor in Borosil and have been watching progress of this company under stewardship of Shreevar Kheruka. He had taken over a sleepy scientific glassware making company from his dad (we have all used Borosil burettes and pipettes in chemistry labs in school/ college) and slowly turned it into a thriving consumerware brand. From the beginning, Shreevar was very clear about what and how he wants to achieve the end goal. I remember attending many calls where despite lower margins, Shreevar would say that he is playing a long game of brand building and hence would not reduce marketing spend for the sake of margins for few quarters. All those efforts have started showing results now.

Slowly and steadily he added more products in glass as well as non glassware, built distribution network, added right manufacturing capacities, demerged scientificware division while increasing brand visibility and thereby increasing market share. Recent results of Borosil is testimony of this when you compare it with its competitors like La Opala, Cello etc. Seems like a classic case study for management school…

I have used many of the Borosil products and also got chance to check out their after sales service and happy to say I am satisfied with their product and service quality.

In last 5 years, company has created a good foundation for sustainable growth in highly competitive consumerware market. They have done the hard yards and now future looks very promising.

15 Likes

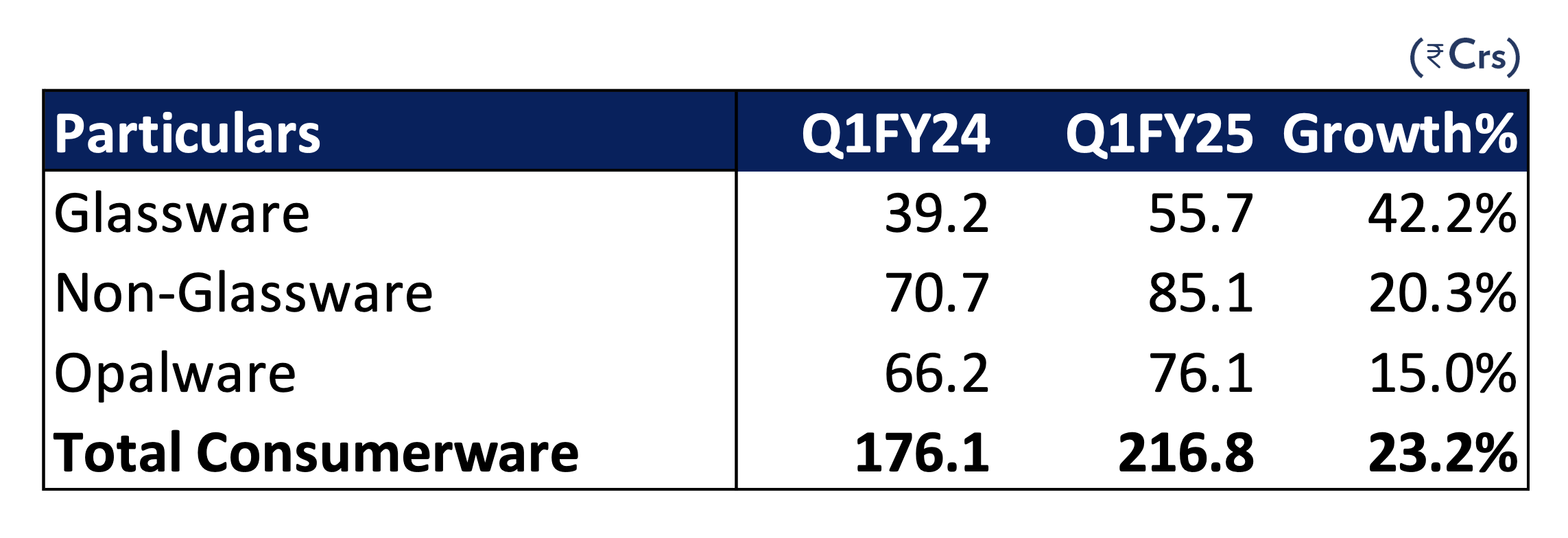

Here’s a summary of the key points from latest Investor Presentation:

Financial Performance for Q1 FY25 (Quarter ended June 30, 2024):

- Net Sales: ₹216.8 crores, up 23.2% year-over-year (YoY)

- EBITDA: ₹36.7 crores, up 74.9% YoY

- EBITDA margin: 16.0%, improved from 13.6% in Q1 FY24

- Profit Before Tax (PBT): ₹12.9 crores, up 80.4% YoY

- Profit After Tax (PAT): ₹9.3 crores, up 87.6% YoY

- Net Debt: Reduced to ₹57.8 crores from ₹94.5 crores in the previous year

Segment-wise Performance:

- Glassware: ₹55.7 crores, up 42.2% YoY

- Non-Glassware: ₹85.1 crores, up 20.3% YoY

- Opalware: ₹76.1 crores, up 15.0% YoY

Other Key Insights from the commentary/slides:

-

Strong overall growth: The company has shown robust growth across all segments, with total consumer ware sales increasing by 23.2%.

-

Improved profitability: Significant improvement in EBITDA and PAT, indicating better operational efficiency and cost management.

-

Debt reduction: The company has reduced its net debt, strengthening its financial position.

-

Diversified product portfolio: Borosil has successfully expanded from being primarily a glassware company to offering a wide range of consumer products including non-glassware and opalware.

-

Market position: Borosil is positioned as one of the leading brands in glass microwavables and claims to be the largest opalware player in India.

-

Future growth strategies: The company aims to achieve a revenue CAGR of 15-20%, improve EBITDA margins, and optimize capital employed through various initiatives including increasing penetration of glass storage and opalware, introducing innovative products, and accelerating e-commerce growth.

-

ESG focus: Borosil has outlined strategic ESG priorities, including aims to achieve carbon-neutral operations, create a positive water balance, and focus on waste management opportunities.

Disclaimer: Holding part of tail end of LT PF. No recos., No transaction in last 30 days.

2 Likes

noted on Borosil Limited

1 Like

BOROSIL LTD -

Q1 FY 26 results and Concall highlights -

Revenues - 226 vs 216 cr, up 4.5 pc

EBITDA - 47 vs 36 cr, up 28 pc ( margins @ 17.8 vs 16 pc )

PAT - 17.4 vs 9.3, up 87 pc

Category wise sales -

Glassware - 56 vs 55 cr, up 1 pc

Non Glassware - 94 vs 85 cr, up 10 pc

Opalware - 76 vs 76 cr, flat YoY

Borosil’s brand - Larah is now India’s no 1 Opalware brand. Company has 84 TPD opal ware capacity - largest in India. Larah brand was acquired by Borosil in 2016. Its sales have grown @ 26 pc CAGR from 2016 to 2025 ( from 48 cr to 384 cr )

Company also has a 25 TPD borosilicate plant ( commissioned in Mar 24 ). This backward integration is margin accretive { Borosilicate glass offers superior thermal shock resistance, chemical durability, and strength compared to normal (soda-lime) glass }

Company’s Non - Glassware sales have grown from 23 cr to 453 cr over last 8 yrs @ 45 pc CAGR

As on 20 Jun, company has a net debt of 5 cr on books

Setting up a new manufacturing facility in Rajasthan for Steel Vacuum Flasks and Containers. Capex outlay for the same shall be around 40 cr. It will have a capacity to produce 24 lakh units / yr. Should commence operations wef Q4 this yr

Brown goods market in India comprising of Kitchenware, Microwaves, Small appliances is expected to keep expanding @ 10 pc CAGR for next 5-7 yrs - led by rising per capita income

Increased rejection of plastic cookware ( led by health concerns ) by millennials is accelerating a move towards Glassware, Steelware and Opalware - a space where the company operates

Company has operationalised 2 solar power plants in Rajasthan of 16 MW capacity - now catering to 30 pc of company’s power costs. Will be spending another 75 cr to set up another Solar plant @ Bikaner with a capacity of 20 MW

Demand scenario in Q1 was muted. Capacity utilisations in Opalware, Glassware in Q1 were @ 80 pc and 60 pc respectively. If the demand improves, company would like to go upto 100 pc and 80 pc capacity utilisations in these 2 segments

Confident of achieving aprox 15 pc revenue growth CAGR over next 2-3 yrs

Aim to hit 20 pc EBITDA margins over next 2 yrs. Margin improvement in Q1 was led by savings on power costs ( due captive solar plants ) and rationalisation of advertising and marketing spends

Company did lose some sales in Q1 due shortage of supply for their Hydra range of products. Supply challenges are ongoing but have reduced vs Q1. Company sells > 100 SKUs under their Hydra brand

Should be able to save 13-14 cr on power costs ( due solar energy ) vs FY 24 ( not FY 25 ). Once the new Bikaner solar power project going online, total savings will ramp upto 30 cr / yr ( vs FY 24 )

Post this, company’s power supply from solar sources shall rise to 65 pc with a further roadmap to reach 100 pc

Company’s mkt share in Opalware in India is about 30 pc

The new vacuum steel flask / containers facility shall be able to generate revenues of 120 cr / yr. After this, company is expected to go for another round of capacity expansion for steel flasks / containers

At present, there are 24k retail outlets that the company sells / supplies its products to - on a regular basis ( ie - at least once every Qtr ). Realistically, company aims to take this coverage upto > 40k outlets in next 3-4 yrs

E comm / Quick Comm - demand has been holding up very well. Weakness is there is general trade and gifting channels ( due rollout of new Pharma regulations ). Seeing green shots in the general trade in Q2

Company is planning to be-bottleneck their opalware facilities. That should increase their capacities by 15-20 pc - sometime in next FY. Plus they r not at 100 pc capacity utilisations at present. This should help them take care of Opalware demand for next 2 yrs

Disc : initiated a tracking position, not SEBI registered, not a buy/sell recommendation, posted for educational purposes

6 Likes